1. 1

Department of Labor (DOL) Fiduciary Rule – The DOL’s

perspective

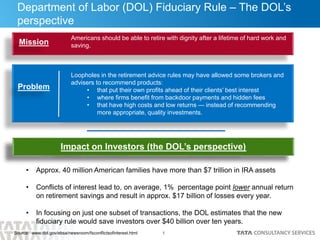

Impact on Investors (the DOL’s perspective)

Americans should be able to retire with dignity after a lifetime of hard work and

saving.

• Approx. 40 million American families have more than $7 trillion in IRA assets

• Conflicts of interest lead to, on average, 1% percentage point lower annual return

on retirement savings and result in approx. $17 billion of losses every year.

• In focusing on just one subset of transactions, the DOL estimates that the new

fiduciary rule would save investors over $40 billion over ten years.

Loopholes in the retirement advice rules may have allowed some brokers and

advisers to recommend products:

• that put their own profits ahead of their clients' best interest

• where firms benefit from backdoor payments and hidden fees

• that have high costs and low returns — instead of recommending

more appropriate, quality investments.

Problem

Mission

Source: www.dol.gov/ebsa/newsroom/fsconflictsofinterest.html

2. 2

Department of Labor (DOL) Fiduciary Rule – An Overview

The proposed rule applies to advice provided to:

– IRA account holders, including rollovers into an IRA

– individual participants and beneficiaries of employer-sponsored plans

– plan sponsors of ERISA plans, unless the carve-out applies.

The Proposed rule:

– Requires a financial professional (advisor) giving investment advice to comply with the “fiduciary” standard, i.e. put

the clients financial interests before his or her own and where the account is a qualified [retirement] account

– Prohibits advisors from accepting any payments / compensation that create a conflict of interest unless they qualify

for an exemption intended to assure the customer is adequately protected

– Allows customers to take action for breach of contract and gives the DOL the right to bring enforcement actions

against fiduciary advisors, if they believe the fiduciary has not put the interests of the client first

– Defines retirement investment advice to exclude education and include the recommendation of specific investments.

Best Interest

Contract

Point of Sale

Disclosure Web Disclosure

The BIC Exemption: 4 Client - facing components

Annual Disclosure

The DOL offers an exemption to prohibited transactions (which in turn, allows them) but requires certain

disclosures be put in place for the protection of the consumer.

– This exemption permits advisors to receive commission-based/ variable compensation from third parties.

3. 3

How people save for retirement

Non-Qualified

Government

• 403(b)

Schools

• 401(a)

State/local

• 457

State/local

Defined

Contribution

• Rollover

• Traditional

• Roth

• Inherited

• SEP-IRA*

• SIMPLE IRA**

• Brokerage

• Advisory

• Direct Mutual

Fund

• Cash Solicitor

IRA’s

ERISA Non-ERISA

Qualified (Tax-advantaged accounts)

ERISA - Employee Retirement Income Security Act - 1974

• DOL enforces ERISA

• Sets minimum standards for pension plans

• Provides protection for participants and beneficiaries

• Those who manage must meet ‘fiduciary’ standard of conduct

IRS Plans/

Accounts

• Pensions

Defined Benefit

Defined

Contribution

Other

(non-retirement)

• Brokerage

• Funds

• Equities

• ETF’s

• Savings

• Money Market

• CD’s

• 401(k) Private

• 401(a) Non-

Govt.

• 403(b)

sponsored by

tax-exempt

orgs

PTE 84-24 for FA’s

BIC for VA’s & all other

** SIMPLE IRA - Savings Incentive Match Plan for Employees* SEP IRA - Simplified Employees Pension

4. 4

Department of Labor (DOL) Fiduciary Rule – Main

Components

Best Interest

Contract

• Firm & advisor must

provide advice in the

best interests of client

• Discloses any conflict of

interests

• Warrants that the firm

has policies to mitigate

conflicts of interests

Disclosure at time of

sale that shows:

Fees, expenses

Total Cost of

Investment if held

for 1, 5, 10 years at

a reasonable rate of

return

Point of Sale

• Products in the same

class should offer

same commission

levels and structures to

mitigate conflict of

interest

• Must consolidate comp

data to easily integrate

with other components

Compensation

• Annual disclosure must

provide:

• Actual fees &

expenses

• Actual

commissions paid

Annual

Disclosure

• A public webpage

that shows

• charges to

investor

• compensation

paid to the firm

and advisor

Web Disclosure

5. 5

How will this impact consumer, you, and the industry?

Consumer

Insurance

Company

The

Industry

Advisors will be held to the “fiduciary” standard when providing advice for your IRA

Certain disclosures may be necessary (BIC, POS, Web Page, Annual Disclosure)

Clients will have the right to bring an action against the advisor if it is believed that a

fiduciary did not act in their best interest, failed to disclose, or violated any law. (Contract

can require arbitration but must give clients the right to bring a class action lawsuit if a group

of people are harmed)

Must implement policy, procedure and systems to support and comply

with the BIC Exemption for Advisors to receive variable compensation.

Must warrant it has identified & mitigated material conflicts of interest and

compensation structures that would encourage advisors to make

recommendations that are not in clients' best interests

Training, Education and Communication

Potential increase in litigation from consumers

Potential increase in enforcement actions by DOL against

advisors

Move to asset-based fee arrangements , fixed (indexed)

annuities

Some broker dealers exiting the business

![2

Department of Labor (DOL) Fiduciary Rule – An Overview

The proposed rule applies to advice provided to:

– IRA account holders, including rollovers into an IRA

– individual participants and beneficiaries of employer-sponsored plans

– plan sponsors of ERISA plans, unless the carve-out applies.

The Proposed rule:

– Requires a financial professional (advisor) giving investment advice to comply with the “fiduciary” standard, i.e. put

the clients financial interests before his or her own and where the account is a qualified [retirement] account

– Prohibits advisors from accepting any payments / compensation that create a conflict of interest unless they qualify

for an exemption intended to assure the customer is adequately protected

– Allows customers to take action for breach of contract and gives the DOL the right to bring enforcement actions

against fiduciary advisors, if they believe the fiduciary has not put the interests of the client first

– Defines retirement investment advice to exclude education and include the recommendation of specific investments.

Best Interest

Contract

Point of Sale

Disclosure Web Disclosure

The BIC Exemption: 4 Client - facing components

Annual Disclosure

The DOL offers an exemption to prohibited transactions (which in turn, allows them) but requires certain

disclosures be put in place for the protection of the consumer.

– This exemption permits advisors to receive commission-based/ variable compensation from third parties.](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)