1. Equity Research

Metals & Mining, Exploration | Canadian Small Cap

June 22, 2016

Alex Cutulenco

Analyst

alex@gravitasfinancial.com

1-416-992-6731

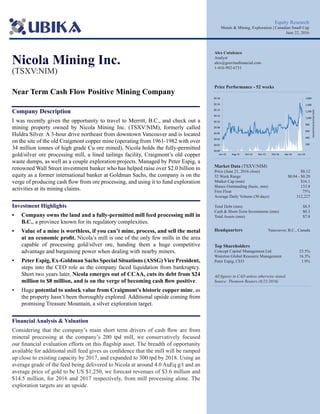

Price Performance - 52 weeks

Market Data (TSXV:NIM)

Price (June 21, 2016 close) $0.12

52 Week Range $0.04 - $0.20

Market Cap (mm) $16.1

Shares Outstanding (basic, mm) 133.8

Free Float 75%

Average Daily Volume (30 days) 312,227

Total Debt (mm) $8.5

Cash & Short-Term Investments (mm) $0.3

Total Assets (mm) $7.8

Headquarters Vancouver, B.C., Canada

Top Shareholders

Concept Capital Management Ltd. 23.5%

Waterton Global Resource Management 16.3%

Peter Espig, CEO 1.9%

All figures in CAD unless otherwise stated.

Source: Thomson Reuters (6/21/2016)

Nicola Mining Inc.

(TSXV:NIM)

Near Term Cash Flow Positive Mining Company

Company Description

I was recently given the opportunity to travel to Merritt, B.C., and check out a

mining property owned by Nicola Mining Inc. (TSXV:NIM), formerly called

Huldra Silver. A 3-hour drive northeast from downtown Vancouver and is located

on the site of the old Craigmont copper mine (operating from 1961-1982 with over

34 million tonnes of high grade Cu ore mined), Nicola holds the fully-permitted

gold/silver ore processing mill, a lined tailings facility, Craigmont’s old copper

waste dumps, as well as a couple exploration projects. Managed by Peter Espig, a

renowned Wall Street investment banker who has helped raise over $2.0 billion in

equity as a former international banker at Goldman Sachs, the company is on the

verge of producing cash flow from ore processing, and using it to fund exploration

activities at its mining claims.

Investment Highlights

• Company owns the land and a fully-permitted mill feed processing mill in

B.C., a province known for its regulatory complexities.

• Value of a mine is worthless, if you can’t mine, process, and sell the metal

at an economic profit. Nicola’s mill is one of the only few mills in the area

capable of processing gold/silver ore, handing them a huge competitive

advantage and bargaining power when dealing with nearby miners.

• Peter Espig, Ex-Goldman Sachs Special Situations (ASSG) Vice President,

steps into the CEO role as the company faced liquidation from bankruptcy.

Short two years later, Nicola emerges out of CCAA, cuts its debt from $24

million to $8 million, and is on the verge of becoming cash flow positive.

• Huge potential to unlock value from Craigmont’s historic copper mine, as

the property hasn’t been thoroughly explored. Additional upside coming from

promising Treasure Mountain, a silver exploration target.

Financial Analysis & Valuation

Considering that the company’s main short term drivers of cash flow are from

mineral processing at the company’s 200 tpd mill, we conservatively focused

our financial evaluation efforts on this flagship asset. The breadth of opportunity

available for additional mill feed gives us confidence that the mill will be ramped

up close to existing capacity by 2017, and expanded to 300 tpd by 2018. Using an

average grade of the feed being delivered to Nicola at around 4.0 AuEq g/t and an

average price of gold to be US $1,250, we forecast revenues of $3.6 million and

$14.5 million, for 2016 and 2017 respectively, from mill processing alone. The

exploration targets are an upside.

-

200

400

600

800

1,000

1,200

1,400

1,600

$0.00

$0.02

$0.04

$0.06

$0.08

$0.10

$0.12

$0.14

$0.16

$0.18

Jun-15 Aug-15 Oct-15 Dec-15 Feb-16 Apr-16 Jun-16

DailyVolume(thousands)

2. Ubika Research

Page 2 - June 22, 2016

Table of Contents

Investment Thesis .................................................................................................................................................. 3

Change in Management Brings a Ruthless Winners-Mindset as well as Decades of Leadership and Operational Experience ........... 3

Nicola Owns a Fully-Permitted Processing Mill in British Columbia ................................................................................................. 3

Exploration will be Funded by Cash Flow, not Dilutive Equity Raises ............................................................................................... 4

Upside: Thule Copper and Treasure Mountain ..................................................................................................................................... 4

The Company ......................................................................................................................................................... 5

Huge Competitive Advantage: Fully-Permitted Gold Processing Mill in B.C. ..................................................................................... 5

Getting Deals Done .......................................................................................................................................................................... 7

Exploration: Thule Copper Project ........................................................................................................................................................ 7

Waste Dumps .................................................................................................................................................................................... 9

Exploration: Treasure Mountain .......................................................................................................................................................... 10

Financial Analysis, Forecasts & Valuation ........................................................................................................ 11

First and Foremost, Nicola is NOT Going Bankrupt ........................................................................................................................... 11

Valuation .............................................................................................................................................................................................. 14

Discounted Cash Flow Analysis .................................................................................................................................................... 14

Risks ...................................................................................................................................................................... 18

A Lot of Factors Influence the Company’s Operations ........................................................................................................................ 18

Exploration Failure .............................................................................................................................................................................. 18

Overall Market Sentiment .................................................................................................................................................................... 18

Conclusion ............................................................................................................................................................ 18

Appendix A: Recent News .................................................................................................................................. 19

Appendix B: Management & Board of Directors ............................................................................................. 20

Nicola Mining Inc.

3. Investment Thesis

Peter Espig, CEO: Change in Management Brings a Ruthless Winners-Mindset as

well as Decades of Leadership and Operational Experience

Peter Espig was appointed President and CEO of Nicola (at the time, Huldra Silver) on

November 7, 2013. From there on, he took his company into CCAA, restructured debt from

$24.5 million to $8.5 million, successfully exited CCAA, and is on track to generating positive

cash flow. His background in corporate turnarounds, having structured over $2.0 billion in

private equity and pre-IPO investment transactions the former Vice President at Goldman

Sachs, was a key addition to the Nicola team.

A former football athlete, father of three, and an accomplished former investment banker, this

three-language speaking mogul (German, Japanese and English) brings a whole different level

of mindset to the company’s management team. Additionally, he also has operational mining

experience, having previously spent 8 years as a diamond driller with Connors Drilling.

Having personally spent a couple days with Peter at the mining facility in Merritt, I saw that

he is highly regarded by his team, and has an accomplishment-type attitude. There are not a

lot of Canadian public company CEOs like Peter, which should give investors a good level of

comfort for his vision and execution at Nicola.

Nicola Owns a Fully-Permitted Processing Mill in British Columbia

This is a huge competitive advantage. Considering that the Province of British Columbia has a

lengthy and stringent permitting process when it comes to economic development, Nicola has

a huge leg up on the competition with their fully-permitted mill. The process of getting First

Nations’ approval for mine development and mill processing may generally take years, and

cost millions of dollars. Nicola’s grandfathered permit allows the company to process mill feed

from throughout the Province.

This competitive advantage ensures that Nicola will most likely remain one of only a few gold/

silver processing mills in B.C., which provides it clean bargaining leverage in negotiating

with miners. From the miner’s standpoint, an ore in the ground is worthless, unless it can

be extracted, processed, and sold for an economic profit. Partnering with Nicola as the ore

processor is often the only solution.

To date, Nicola’s mill is permitted to process 200 tonnes per day of mill feed, and five mineral

processing contracts have already been signed. The mill was constructed for expansion, and

currently has crushing capacity of 500-600 tpd. We believe that the mill will be operating at

full capacity by Q2/2017.

Page 3 - June 22, 2016

Ubika Research Nicola Mining Inc.

4. Exploration Funded by Cash Flow, not Dilutive Equity Raises

There are over 1,400 publicly listed mining companies in Canada, out of which 1,200 are

not seeing a single penny in revenues. What’s even worse is that only 100 of these mining

companies are seeing positive operating cash flows. Cash generation is very difficult in the

mining sector, which ultimately forces a lot of companies to raise dilutive financing to fund

exploration and other operating activities. The company will position itself to choose between

conducting future exploration by using flow through financing or cash flow from operations.

This is especially true with exploration companies. These stocks have no way of generating

cash flow, and are forced to seek out funding from the market. In fact, it is estimated that for

every 1,000 properties drilled, only 1 will see an economically viable discovery. However, the

story is very different with Nicola. Nicola’s strategy is to self-fund its exploration activities via

cash flow generation from its ore processing mill.

Upside: Thule Copper and Treasure Mountain

Although we believe that the mill will be the primary source of value creation for shareholders

in the short term, longer term gains will result from continued exploration work at the

company’s two targets.

The Thule Copper Project is located in the prolific copper-rich Guichon Batholith, home to

the famous Craigmont Copper and Highland Valley Copper mines. The 100% owned copper

porphyry project consists of 21 mineral claims covering approximately 10,084 hectares of

land. The project includes the past producing Craigmont copper-iron mine, which operated

from 1961 to 1982, and produced 34,000,000 metric tonnes of ore, averaging 1.28% copper.

The Thule Project consists of several historic zones with known copper mineralization. The

2016 exploration program will target the Embayment Block, the WP, Titan Queen, Eric and

Marb zones. All of these zones occur proximal to the Nicola Group-Guichon Batholith contact

and to prominent fault trends.

On the other hand, the 100% owned Treasure Mountain Mine is a 7,000-acre silver deposit

comprising of 21 legacy claims. Near term focus will be to continue the exploration of 3

highly-prospective targets. The company has the option to extract 430,000 oz. of NI 43-101

compliant high grade silver ore from Level 1 Stope 2 of its mine, which has already incurred

approximately 60% of the cost associated with extraction of material.

Page 4 - June 22, 2016

Ubika Research Nicola Mining Inc.

5. The Company

Nicola Mining Inc. (TSXV:NIM) is not your typical mining company. In contrast to the

cash infused, high expenditure, moonshot exploration companies listed on the Canadian

exchanges, Nicola prides itself on funding its exploration activities via self-sustaining cash

flow. Yes, real cash flow which it generates from its flagship asset – the Merritt Mill.

Apart from the mineral processing mill, the company also owns a fully-lined tailings facility,

Craigmont waste dumps, and a couple exploration properties – Thule Copper and Treasure

Mountain.

Huge Competitive Advantage: Fully-Permitted Gold Processing Mill in B.C.

The company currently owns a 200 tonnes per day (tpd) processing mill/facility, located 10

kilometers northwest of Merritt, B.C. The mill is permitted to conduct custom milling of ore,

with recovery of gold and silver metal. The mill was constructed in the fall of 2012 and, for

a cost of $21.6 million, went into commercial production in March 2013. The land on which

the mill is constructed is owned freehold and was purchased for $8.0 million. In addition,

the company installed a fully-lined tailings facility for approximately $2.0 million, which

minimizes the environmental footprint of operations.

Page 5 - June 22, 2016

Ubika Research

Figure 1: Nicola’s Mill

Source: Ubika Research, property visit (06/06/2016)

Nicola Mining Inc.

6. Page 6 - June 22, 2016

Figure 2: Stockpiled ore ready for processing

Source: Ubika Research, property visit (06/06/2016)

Ubika Research

Ore in the ground doesn’t mean anything, unless you are able to mine it, process it,

and sell the mineral at an economic profit. Or at least that’s the idea behind successfully

operating a mine. Unfortunately, mining in British Columbia is a tough business, considering

the length and capacity of permitting required that companies have to go through in order to

operate a mine - let alone a mill the mined resource.

Unlike other provinces, British Columbia does not have modern-day treaties with its First

Nations. A supreme court ruling in June 2014 recognized the requirement of First Nation

consultation and approval for resource-based projects. This has essentially made it easier for

First Nations to establish title over lands that were regularly used for hunting, fishing and

other activities. Economic development on land where title is established would require the

consent of the First Nation. In turn, this creates a timely regulated process of getting projects

permitted.

This is where the story gets interesting – Nicola is one of the only few operators of a fully-

permitted gold/silver processing mill in B.C. This is huge considering that a miner looking

to make money from mining activity, have to process their ore prior to selling the metal in the

open market. Think of it in term of an airport logistics model – Nicola’s mill is an airport for

all the airplanes (miners in B.C.) to land. Without an airport, there are no planes.

And sure, miners can apply themselves to gain a milling permit, however the process will

typically last 5 years, and will cost tens of millions of dollars in fees to the First Nations

(owners of the land). Because of these constraints, a mineral extraction process turns

economically un-feasible, and un-fundable. Turning to a third party processor makes

economic sense – which is where Nicola comes into play.

Over the past year, Nicola has been working closely with miners within the area, in order to

develop contractual partnerships for the processing of ore. To date, four partnerships have

been signed, various others are in close negotiations, and the mill is expected to operate at

full capacity by Q1/2017. For a breakdown of current and potential contracts, see Financial

Analysis.

Nicola Mining Inc.

7. Ubika Research

Page 7 - June 22, 2016

Getting Deals Done

As mentioned in our Investment Thesis, Nicola is run by Peter Espig, a very accomplished

individual strongly capable of turning around what used to be Huldra Silver, and making

Nicola a truly unique company. His focus in the short term will be to develop contractual

partnerships with miners within the area, and ramp up his mill to full capacity.

As deals go, Peter should be more than capable of getting enough throughput for its 200 tpd

milling operations. Longer term, we should expect the company to apply for an increased

milling rate to the mills designed capacity of around 500-600 tpd. This is where the

growth will occur from, and considering the wide range of projects in the area, we should see

supply that matches the mills capacity.

Exploration: Thule Copper Project

The Thule Copper Project is 100% owned by Nicola, located 14 km north-west of Merritt

B.C., and consists of 21 mineral claims covering approximately 10,084 hectares of land.

Nicola Mining Inc.

Figure 3: Old Craigmont Mine (operational from 1961-1982)

Source: Ubika Research, property visit (06/06/2016)

8. There are two dominant styles of mineralization at the property: copper iron skarn and copper

porphyry. The most important discovery to date on the property has been the past producing

Craigmont copper-iron mine, located in the central part of the claims. Craigmont operated from

1961 to 1982, and produced 34,000,000 metric tonnes of ore, averaging 1.28% copper.

Craigmont shut the mine down in 1982 due to falling copper prices (with copper trading at

approximately $0.60 per pound), and the property was later acquired by Huldra Silver in 2011.

The Craigmont Mine is made up of four zones of copper and iron mineralization known as

the No1, 2, 3 and 4 bodies. Although No1 and No2 bodies at the Property are believed to be

mined out, historical reports suggest No3 and No4 bodies remain open for exploration. Non-

compliant 43-101 estimates by Craigmont Mines calculated a possible reserve of 1.29 million

tons grading 1.53% copper at No3 body, assuming a 0.7% cut-off grade. On the other hand,

the No4 body is vaguely represented by a mineralized intercept on section 4700E where core

from diamond drill hole S100 assayed 149 metres of 0.41% copper.

Page 8 - June 22, 2016

Ubika Research

Figure 4: Thule Copper Property and Target Zones

Source: Company Website

At this moment, no further drilling activity has taken place at Thule Copper, and it is noted in a

technical report that future exploration will be considered higher risk and expensive due to the

depth of potential new targets and associated copper mineralization.

The Thule Copper Project consists of several historic zones with known copper mineralization.

The 2016 exploration program will target the Embayment Block, the WP, Titan Queen, Eric

and Marb zones. All of these zones occur proximal to the Nicola Group-Guichon Batholith

contact and to prominent fault trends.

Nicola Mining Inc.

9. Page 9 - June 22, 2016

Ubika Research

Figure 5: Craigmont Waste Dumps

Source: Ubika Research, property visit (06/06/2016)

Waste Dumps

Walking by the Craigmont mine, large piles of waste rock have been left out next to the open

pit from the mining operations done in the 1960’s-80’s. Cut-off grades of 0.7% - 1.2% were

applied while Craigmont operated, so naturally, most of the unwanted ore was left without

processing. The estimated volume of the waste rock is approximately 100 million tonnes.

Nicola Mining Inc.

As you can see from the pictures blow, the mineralized rock is clearly observed from the waste

rock collected. We believe that there is potential value in this ore if it is further processed.

Figure 6: Mineralized Ore

Source: Ubika Research, property visit (06/06/2016)

10. Page 10 - June 22, 2016

Ubika Research Nicola Mining Inc.

Exploration: Treasure Mountain

Nicola Mining also owns 100% of the Treasure Mountain property, an approximately 7,000-

acre silver deposit consisting of 51 mineral tenures, comprising 21 legacy claims. The project

is about 29 kilometers northeast of Hope, BC. or a 3-hour drive from Vancouver, B.C.

Exploration at Treasure Mountain since June of 2011 has consisted of 69 diamond drill holes

over a total length of approximately 7,000 meters.

Nicola Mining Inc. continues to maintain the option of reopening Level 1 in order to extract

silver mill feed from Stope 2; however, given the global status of depressed silver prices,

the near term focus will be to continue focusing on the exploration of 3 highly-prospective

targets:

• MB Zone located approximately 1.5km from the underground mine workings on the

undrilled Northern backside of the mountain. Though not yet drilled, the MB Zone

has provided positive soil sample results such as 0.79 g/t Au, 7270 g/t Ag, 0.81%

Cu, 1.56% Pb, 1.23% Zn, 0.76% As, 0.60% Sb from a 0.06m chip sample of reddish

oxide clay.

• JV Vein/Eastern Zone located approximately 1.0 km from the underground mine

workings. the area had modest success reported from the area, with numerous rotary

reverse circulation chip sample intervals assaying as much as 34.48 opt (1072.44 g/t)

Ag, 15.2% Pb and 0.04% Zn over 20 feet (6.1 m).

• Jensen Portal located approximately 100 meters west of the Level 3 Portal and

previously mined in the 1920’s. The Company has not conducted any exploration at

the Jensen Portal.

11. Financial Analysis, Forecasts & Valuation

We believe that the company’s past two-year share price decline and stagnation are largely

attributed to the investors’ sentiment placed over Nicola’s financial situation. Having entered

creditor protection (CCAA) on July 26th

, 2013, the company’s share price responded with a

50% nosedive, followed by further declines to today’s current market price of just 14 cents.

Within this timeframe, Nicola has changed its name (formerly Huldra Silver), rolled back its

share count on a 1 for 5 basis, and has successfully exited CCAA on December 5th

, 2015.

To ease investors’ fears, we would like to discuss Nicola’s current financial obligations, as well

as its ability to service them via revenue generation coming from existing projects. Simply put:

can Nicola generate enough revenue to pay off creditors, and have some cash flow left

over for equity shareholders?

First and Foremost, Nicola Continues to Stabilize its Balance Sheet

Looking at the company’s balance sheet, we clearly see that the company is not in a healthy

position, as evident by a shareholder’s deficit of $5.5 million, and a negative working capital of

$4.0 million.

Page 11 - June 22, 2016

Ubika Research

Figure 7: Nicola Mining Inc.’s Balance Sheet (as at March 31, 2016)

Source: Sedar Filings

Nicola Mining Inc.

12. Page 12 - June 22, 2016

Ubika Research

That being said, our biggest points of concern are:

• Flow-through obligations of $3.7 million

• Waterton Debt Loan of $1.3 million

• Secured Convertible Debenture of $6.2 million

• and the fair value of the $6.1 million PP&E asset account, which is discounted due to

accounting standards

Flow Through Share Obligation: $3.7 million

Flow Through Shares (FTS) are special shares issued by a mining company to investors, which

grant the investor additional tax saving incentives. Basically, a company issues FTS, and is

required to use the proceeds from the issuance to incur exploration costs.

These exploration costs then entitle the investor to use as personal expenses when calculating

personal income taxes. As you can see, an investment of $1,000 by an investor into FTS, can

be used as a tax deduction on their income. If the investor’s effective tax rate is say 25%, this

$1,000 investment saved the investor from paying $250 in taxes.

In Nicola’s case however, the company issued 12,000,000 FTS on March 30, 2013 and have

not used the gross proceeds for qualifying exploration expenditure. According to the CRA,

qualifying expenditures must then be incurred within 24 months following the month in which

the agreement was entered into. Theoretically, we should see the FTS obligation wiped off the

balance sheet as the company begins exploration work. The amount will be depreciated starting

2017.

Waterton Debt: $1.3 million

After a long and convoluted relationship built over the years with Waterton, the creditor re-

mains entitled to the remaining $1.3 million debt balance, bearing interest at an annual 3% rate

paid annually, and maturing on November 24, 2018.

Nicola Mining Inc.

With interest payments of roughly $40k/year, and maturity in another 2 ½ years, we are not

really worried about this debt balance. It should be noted that Waterton is also a major share-

holder of the company.

13. Page 13 - June 22, 2016

Ubika Research

Secured Convertible Debenture: $6.2 million

Nicola closed a couple tranches of convertible debt financing of $7.0 million and $0.3 million,

in November 2014 and May 2015 respectively. The debt incurs interest at 10% per annum, and

is paid 50% in cash and 50% in newly issued common shares at price equal to the market price

at time of issuance (on payment day). Both of the tranches have a maturity of three years, and a

principal conversion price of $0.275/share.

We are most concerned with the first tranche of this debt financing, as evident by the event

which occurred on the first payment day (Nov. 21, 2015). Nicola has effectively paid out the

interest owed (which was supposed to be $700k million) through the issuance of 12,924,705

common shares at $0.065 per share (resulting in an implied interest payment of $840k). Instead

of paying out the interest in cash/shares on a 50-50 basis as originally negotiated, the company

paid 100% via share issuance and agreed to settle the interest as if rate was 12% rather than

10% for first year.

Although the company managed to get out of paying $350k in cash, we are unhappy of the

additional share issuance. Although we hope that this event will not persist for future interest

repayments, we do note the risk involved. Nicola should be able to mitigate the risk of

defaulting on interest payments via its cash generation from the newly started mill.

Additionally, considering that the principal repayment is within a 1 ½ years, we feel that the

company’s share price would have increased by that point (as per our Valuation), allowing

Nicola to refinance the debt at a lower interest rate. We would also like to note that this is

friendly debt of which 90% is held by its largest shareholders and management.

Nicola Mining Inc.

14. Page 14 - June 22, 2016

Ubika Research

Valuation

Valuing Nicola Mining can be done is several ways. Specifically, a discounted cash flow

model, comparable companies model, and an asset liquidation model all seem appropriate.

However, since Nicola is such a unique mining company, not a whole lot of comparables

would be justifiable. Additionally, a liquidation model assumes a fair price for assets (which is

essentially guessing what the next buyer would pay for Nicola’s assets) – also a tough task. To

keep things conservative, we will only look at Nicola’s producing mill, and forecast those

cash flows.

Mineral Processing - Cash Flow Analysis

The company is able to generate cash flow in three respective ways: mill feed processing,

gravel sales, and industrial soils processing.

Considering that the company’s main short term drivers of cash flow will result from mineral

processing at the company’s 200 tonnes per day (tpd) Merrit Mill, our objective will primarily

be to account for the current contractual obligations Nicola has entered into with mineral

producers, as well as to identify potential other nearby sources of mill feed, and use those for

forecasting purposes.

Figure 8: Nicola Mining is Currently Engaged with 4 Clients (green point represents Nicola’s mill):

Source: Ubika Research, Mapcustomizer.com

Nicola Mining Inc.

Client #1 – Gavin Mines Inc.

Gavin Mines operates the Dome Mountain gold-silver mine, located approximately 38 km

east of the Town of Smithers in northwest B.C. The agreement schedules for the delivery of

approximately 6,000 tonnes of stockpiled material.

The loading and transportation costs will be covered by Gavin Mines, with milling costs taken

care of by Nicola. Afterwards, the profit on the sale of the refined metal will be split 50/50

between the two parties. Loading and transportation costs have been estimated at $60.50/tonne,

with milling costs estimated at $75.00/tonne. The grade of the processed mill feed will be

approximately 9.0 g/t.

15. Page 15 - June 22, 2016

Ubika Research Nicola Mining Inc.

Processing of this stockpiled material will take approximately 54 days, and using a gold price

of US $1250/oz, will yield $664k.

Looking past this one-off stockpiled resource, the Dome Mountain deposit has a lot more ore

which may be mined and used as potential feed to Nicola. Specifically, an April 2010 NI 43-

101 report states an Indicated Resource of 138,000 tonnes and an Inferred Resource 154,000

tonnes (at a 5.0 g/t cut-off). This feed can stimulate 200 tpd milling for the next 4 years alone.

Client #2 – Siwash Minerals Inc.

The Miner’s property is located in the Siwash Creek Area, located approximately 8 km

northeast of Yale, B.C. and approximately 90 minutes from Nicola Mining’s processing facility

in Merritt, B.C.

Siwash has a stockpile of 6,000 tonnes of ore which will make its way to Nicola’s mill for

processing, with the same economic arrangements as the stated agreement with Gavin Mines.

Slightly adjusting the trucking costs to account for a shorter commute to Nicola’s processing

facility, we forecast a profit of $778k to both parties.

Surprisingly enough, there is not much information to be found on Siwash.

Client #3 and #4 – Clibetre Exploration Inc. & High Range Exploration

Under the Clibetre Agreement the Miner plans to ship mill feed that has already been extracted

and is currently being stored on its property, which is located approximately 25 km west of the

city of Courtenay, B.C. Under the Clibetre Agreement, the miner plans to ship stored mill feed

from its wholly-owned Mt. Washington Property to Nicola for processing. At this moment, no

visibility on tonnage or grades have been provided.

Under the High Range Agreement, High Range plans to extract mill feed from its wholly-

owned Dominion Creek Property, which is located 43 kilometers northeast of the Town of

Wells and about 110 kilometers east-southeast of Prince George, and then plans to ship this

mill feed to Nicola for processing.

High Range intends to apply for a Bulk Sample Permit from the Ministry of Energy and Mines

of British Columbia, which, if obtained, would allow High Range to extract up to 10,000

tonnes of mill feed. According to the milling agreement, mill feed will be stored and tested on

site to confirm grades greater than 15.6 g/t AuEq. Once a sufficient stockpile has been achieved

the stockpile will be transported to Nicola’s Merritt Mill.

Mineral Processing - Potential New Sources of Mill Feed

Apart from the current sources of mill feed, there are several other mining properties within a

fairly close radius to the Merritt Mill, which may be suitable partners to Nicola.

16. Page 16 - June 22, 2016

Ubika Research Nicola Mining Inc.

Figure 9: Potential New Sources of Mill Feed for Nicola:

Source: Ubika Research, Mapcustomizer.com

We believe that some of the more promising opportunities may come from the:

• Elk Gold project, owned by Gold Mountain Mining (TSX.V: GUM), having a M&I

resource estimate of 2.2 million tonnes grading 4.3 g/t Au

• Spanish Mountain Gold project, owned by Spanish Mountain Gold (TSX.V: SPA),

having a M&I resource estimate of 237.8 million tonnes grading 0.5 g/t Au

• Chu Chua project, owned by Newport Exploration (TSX.V: NWX), which has an

Inferred resource of 2.5 million tonnes averaging 9.4 g/t silver and 0.5 g/t gold

• Willa Gold Project, owned by Discovery Ventures (TSXV: DVN) which has a M&I

resource of 0.8 million tonnes at a grade of 5.1 g/t Au

Assumptions & Valuation

Considering the breadth of existing clients, as well as the opportunity for additional mill feed

in the future, this gives us confidence that the mill will be ramped up close to existing capacity

(200 tpd) by 2017. Additionally, we feel that the greater potential of the mill will be unlocked

by gaining permitting for mill processing expansion. We forecast that the mill will be expanded

to process close to 300 tpd by 2018. Lastly, we discounted the number of total days of mill

operating hours by 10% to account for various delays, closures and other uncertainties.

We forecast that the average grade of the feed being delivered to Nicola is around 4.0 AuEq

g/t, average price of gold to be US $1,250, exchange rate to be around 1.25 CAD/USD, and

operating costs to average $135/tonne ($75/tonne for milling, and $60/tonne for mining and

trucking).

Using these estimates, we forecast that Nicola will generate $3.6 million and $14.5 million

in revenues, for 2016 and 2017 respectively.

18. Risks

A Lot of Factors Influence the Company’s Operations

Arriving at a $0.23/share price target took a lot of variables, which for the most part were

kept conservative. However, slight variations to these variables may have a material impact.

Variables such as Nicola being granted an increased mill processing permit, changes to gold

price and variation in operating costs, all have a material impact on the valuation.

Another major assumption which may impact the company’s valuation is their ability to keep

the mill operating near capacity. Although there are potential sources of mill feed for the

company to use, valuation may change if either another miner develops their own mill, or if

Nicola fails at coming to terms with new clients.

Exploration Failure

As with all exploration companies, the chances of failure far outweigh the chances of success.

With that, the capital expenditure used for exploration activities may in fact return worthless

results.

Overall Market Sentiment

During times of decreased metals prices, a lot of miners see a share price decrease. Regardless

of specific company operations, all equities typically get hurt. This is currently a minuscule

risk factor considering that metals prices are improving, however, the macroeconomic forces

may prove otherwise in the future.

Conclusion

Nicola Mining Inc. (TSXV:NIM) is not your typical mining company. Having faced

bankruptcy trouble in 2013, the previous CEO was replaced with a much more competent

leader. Peter Espig, a turnaround specialist, has successfully taken this company out of CCAA,

reduced the debt burden from $24.5 million to $8.5 million, and is on the verge of yielding

positive cash flows.

Unlike your typical exploration company infused by dilutive equity financing, Nicola plans

to go through their exploration activities through self-achieving cash flows. The company’s

value lies in its flagship asset – a 200 tpd processing mill – which will be used to process other

miners’ ore. The fully permitted mill is a huge advantage to the company, given the regulatory

environment B.C. faces with First Nations. For miners looking to profit from their ore in the

ground, the only feasible method would be to use Nicola’s mill for processing.

Having already signed four milling contracts, with much opportunity for future mill feed, we

forecast the company’s mill to run at close to capacity in 2017 and increase capacity to 300 tpd

by 2018. Our cash flow forecasts are highly conservative, and only accounts for activity at the

mill. The exploration projects (Thule Copper and Treasure Mountain), uses for the company’s

tailings pond, and its gravel pit are all simply upsides to the investor.

Page 18 - June 22, 2016

Ubika Research Nicola Mining Inc.

19. Appendix A: Recent News

Nicola Mining Commences Milling Operations

Nicola Mining commenced milling operations at its 200 tonne per day mill facility located 14

kilometers from Merritt, British Columbia. The Company has completed successful test runs

to confirm gold recovery rates and has commenced processing of material received from Gavin

Mines Inc.

Nicola Mining Provides Update on Thule Project Exploration Activities

During the first half of 2016, the Company is pleased to announce the following achievements:

Successfully re-logging and cataloging 7000 metres of historical drill core covering the

Embayment, Eric and Titan Queen mineral showings; 53 trench samples collected with a

range from 71 ppm Cu to 1.68% Cu.

Nicola Mining Announces Closing of Strategic Private Placement of $164,000

Closed a private placement of $164,000 with strategic investors that were unable to participate

in the recent Fourth Tranche Unit Financing. The Company sold an aggregate of 2,050,000

Units for gross proceeds of $164,000. Proceeds of the financing will be used for general

working capital.

Nicola Mining Provides Operational Update

The Company has completed all upgrades to its fully-permitted, modern, 200 tonne per day

mill facility. On April 15, 2016, the Company received the required permit amendment to

its mine permit M-68 that enables it to conduct custom milling of third party material. The

Amendment allows the Company to accept mill feed from third parties and execute on milling

and profit share agreements by processing material at the Mill. The Company purchased an I-3

industrial zoned property for $8,000,000 and subsequently constructed the $21.6 million Mill

and a fully-lined tailings facility for $1.8 million on such property. The Mill was constructed

with expansion capabilities and is supported by a 500 tonne per day crushing capacity and 1.7

kVA of hydro-power, of which the current Mill only requires 0.6 kVA and its 1,300,000 gallons

per day water permit.

Paul Johnston (Ph.D. Geological Sciences) Joins Board of Nicola Mining Inc.

Dr. Johnston’s extensive experience in recognizing and enhancing value-adding exploration

projects will be particularly useful as the Company looks deeper into its Thule Copper Project,

as well as potential acquisitions to augment its modern processing mill located 10 km outside

of Merritt, BC.

Page 19 - June 22, 2016

Ubika Research

May 31, 2016

June 8, 2016

June 16, 2016

May 31, 2016

May 19, 2016

Nicola Mining Inc.

20. Appendix B: Management & Board of Directors

Peter Espig, President, CEO and Director

Mr. Espig was appointed President and CEO on November 7, 2013 during CCAA

proceedings culminating in the restructuring of the Company on November 21, 2014. He

is experienced in the analysis of investment opportunities, raising capital, deal sourcing,

financial structuring and corporate turnaround. Mr. Espig has structured over US$2.0 billion

in private equity and pre-IPO investment transactions from the principal side.

Mr. Espig has been active in the turnaround of mining projects and has functioned in

management roles and as a director for numerous mining companies.

Mr. Frank Hogel, Chairman of the Board

Mr. Hogel is an Asset Manager actively involved in the financial evaluation of companies

and convertible debenture restructuring, and sits on the advisory board of Concept Capital

Management. His background includes more than 13 years of direct experience in the mining

industry, expertise as an international financier/investor and successful track record stock

consultant and stock broker in London, England. Mr. Hogel holds a degree in Economics and

International Business and management from the University of Nürtingenin Germany and

Finance Degree (DTV).

Mr. Doug F. Robinson, Q.C., Director

Mr. Robinson has been a member of the B.C. Bar since 1973. He has served as a Director

of the Law Institute of B.C., founding director of the B.C. Mediation Society, and founding

Chair of the Canadian Forum for Civil Justice. Mr. Robinson has litigated and lectured on

legal issues globally and in public practice is recognized by LEXPERT as one of the leaders

in construction and product liability litigation. Since retiring as a senior partner with Lawson

Lundell his focus of expertise has been on mediating corporate disputes and advising high net

worth families on a variety of issues.

Dr. Paul Johnston, P.Geo., Director

Dr. Johnston is a geologist with more than 25 years experience in the mining industry. Dr.

Johnston began his career in the late 1980s as a mine geologist at a large Canadian gold mine

and since 1996 has worked in a variety of international positions at Teck Resources, includ-

ing Regional Chief Geoscientist for South America. He holds a PhD from Queen’s Universi-

ty and is a member of the Association of Professional Engineers and Geoscientists of British

Columbia. He has accumulated extensive international experience in early to advanced stage

exploration for gold, copper, and zinc.

Mr. Warwick Bay, CFO & Corporate Secretary

Mr. Bay has been a member of the Institute of Chartered Accountants of B.C. since 1979.

Mr. Bay practiced for over 10 years with one of the big five public accounting firms and is

specialized in the audit of public mining companies. He also owned and operated a group of

companies in the hospitality industry for 15 years. Prior to joining Nicola Mining Inc., he

spent 17 years in the financial services industry where he focused on raising capital for junior

mining companies and exploration projects.

Page 20 - June 22, 2016

Ubika Research Nicola Mining Inc.

21. Disclosures

Copyright

This report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information,

opinions or conclusions contained in it be referred to without in each case the prior express written consent of Ubika Corporation.

Disclaimer

The Content contained on this page (including any facts, views, opinions, recommendations, description of, or references to, products or securities) made

available by SmallCapPower/Ubika Research is for information purposes only and is not tailored to the needs or circumstances of any particular person. Any

mention of a particular security is merely a general discussion of the merits and risks associated there with and is not to be used or construed as an offer to sell,

a solicitation of an offer to buy, or an endorsement, recommendation, or sponsorship of any entity or security by SmallCapPower/Ubika Research. The Reader

should apply his/her own judgment in making any use of any Content, including, without limitation, the use of any information contained therein as the basis

for any conclusions. The Reader bears responsibility for his/her own investment research and decisions. Before making any investment decision, it is strongly

recommended that you seek outside advice from a qualified investment advisor. SmallCapPower/Ubika Research does not provide or guarantee any financial,

legal, tax, or accounting advice or advice regarding the suitability, profitability, or potential value of any particular investment, security, or information source.

Ubika and/or its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities and/or commodities and/

or commodity futures contracts in certain underlying companies mentioned in this site and which may also be clients of Ubika’s affiliates. In such instances,

Ubika and/or its affiliates and/or their respective officers, directors or employees will use all reasonable efforts to avoid engaging in activities that would lead

to conflicts of interest and Ubika and/or its affiliates will use all reasonable efforts to comply with conflicts of interest disclosures and regulations to minimize

the conflict.

Safe Harbour Statement for US Residents/ Investors

The information set forth in this report may contain “forward-looking statements.” Statements in the report, which are not purely historical, are forward-looking

and include statements regarding beliefs, plans, expectations or intentions regarding the future.

Except for the historical information presented herein, matters discussed in this document contain forward-looking statements that are subject to certain risks and

uncertainties that could cause actual results to differ materially from any future results, performance or achievements expressed or implied by such statements.

There can be no assurance that the highlighted company’s efforts will succeed and the company will ultimately achieve sustained commercial success. These

forward-looking statements are made as of the date of this document, and neither Ubika Corporation nor the highlighted company assumes any obligation to

update the forward-looking statements, or to update the reasons why actual results could differ from those projected in the forward-looking statements.

The forward looking statements contained in the document have been prepared by management of the highlighted company who believe and have so advised

Ubika Corporation, without independent verification by Ubika Corporation that a reasonable basis exists for making such statements.

Analyst’s Comments

The analyst was given the opportunity to travel to the Company’s mining site on June 5th

, 2016. The flight was paid by the client, and all other accommodations

by Gravitas. No part of the Analyst’s compensation was, is, or will be, directly or indirectly, related to the recommendations of views expressed in this research

report.

Investor Quick Links

• Investing Newsletter on www.smallcappower.com

• Visit us at www.ubikaresearch.com for more details of our offering

• Reach us at info@ubikacorp.com for any questions or comments

333 Bay Street, Suite #650

Bay-Adelaide Centre

Toronto, ON, Canada, M5H 2R2