Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

Standard Assessing The Organization Risk Maturity

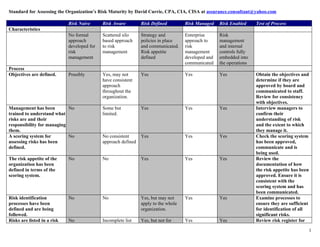

- 1. Standard for Assessing the Organization’s Risk Maturity by David Currie, CPA, CIA, CISA at assurance.consultant@yahoo.com Risk Naive Risk Aware Risk Defined Risk Managed Risk Enabled Test of Process Characteristics No formal Scattered silo Strategy and Enterprise Risk approach based approach policies in place approach to management developed for to risk and communicated. risk and internal risk management Risk appetite management controls fully management defined developed and embedded into communicated the operations Process Objectives are defined. Possibly Yes, may not Yes Yes Yes Obtain the objectives and have consistent determine if they are approach approved by board and throughout the communicated to staff. organization. Review for consistency with objectives. Management has been No Some but Yes Yes Yes Interview managers to trained to understand what limited. confirm their risks are and their understanding of risk responsibility for managing and the extent to which them. they manage it. A scoring system for No No consistent Yes Yes Yes Check the scoring system assessing risks has been approach defined has been approved, defined. communicate and is being used. The risk appetite of the No No Yes Yes Yes Review the organization has been documentation of how defined in terms of the the risk appetite has been scoring system. approved. Ensure it is consistent with the scoring system and has been communicated. Risk identification No No Yes, but may not Yes Yes Examine processes to processes have been apply to the whole ensure they are sufficient defined and are being organization. for identification of all followed. significant risks. Risks are listed in a risk No Incomplete list Yes, but not for Yes Yes Review risk register for 1

- 2. Standard for Assessing the Organization’s Risk Maturity by David Currie, CPA, CIA, CISA at assurance.consultant@yahoo.com register and assigned to may exist whole organization completeness and management. assignment to managers. Response to manage risks No Some responses Yes, but may not Yes Yes Examine the risk register have been selected and identified apply to the whole to ensure appropriate implemented organization responses have been identified. Management has process No Some monitoring Yes, but may not Yes Yes Select sample of for monitoring key controls apply to the whole processes and responses processes, responses and organization and ensure management action plans would know if they were not working or if actions were not implemented. Management report risks No No Yes, but no formal Yes Yes Obtain documentation of to the board where risk process is in place board being advised on responses have not risks above the risk managed the risks to a appetite. level acceptable (risk appetite). All significant new No No Most projects are Yes Yes Examine project projects are assessed for risk assessed proposals for an analysis risk. of risks that may threaten them. Responsibility for No No Limited Most job Yes Review job descriptions. assessment and descriptions management of risk is included in job descriptions. Managers provide No No No Some Yes Review assurance assurance on the managers provided and for key effectiveness of their risk risks check for controls management and are managing them. Examine assessed on their risk a sample of performance management performance appraisals for evidence risk management is being properly assessed. Internal Audit’s approach Promote risk Promote Facilitate risk Audit risk Audit risk 2

- 3. Standard for Assessing the Organization’s Risk Maturity by David Currie, CPA, CIA, CISA at assurance.consultant@yahoo.com management enterprise-wide management and management management and rely on risk use management’s processes and processes and alternative management assessment of risk use use audit approach and where appropriate management’s management’s planning rely on assessment of assessment of method alternative risk where risk where audit planning appropriate appropriate method Example of Key Concepts: • The Chief Executive Officer is ultimately responsible for the organization’s risk management capabilities. • The board provides oversight and should ensure it is appraised of the most significant risks, along with actions management is taking and how it is ensuring effective enterprise risk management. • Everyone in the organization has some responsibility for enterprise risk management. • Management identifies events that will affect the organization. For example, the acquisition of one Bank by another Bank. • The organization’s risk appetite (e.g., broad-based amount of risk an organization is willing to accept in pursuit of its mission) is defined (e.g., high, moderate, low) by management and approved by the board. It serves as a guidepost in strategy setting and selection of related objectives at the entity level and represents the amount of risk an entity is willing to accept in pursuit of value. Management considers it when aligning the organization, its people, and its processes. For example, management has decided that the Bank’s Adjusted Tangible Book Value on the closing date should equal or exceed $330 MM (e.g., Bank’s risk appetite has been defined). • Risk tolerance is the acceptable level of variation relative to the achievement of a specific objective. Operating managers can use risk tolerance to determine what performance measures are required to ensure actual results will be within the risk tolerance…Operating within risk tolerances provides management greater assurance that the entity remains within its risk appetite. For example, management may decide that the number of staff needed to provide for ordinary and usual business practices in order to help achieve the Bank’s objective is as follows: Staff Target Tolerance –Acceptable Range 1. Overall Bank Staffing 516 departure of 40 non-key staff 2. Credit Administration 8 departure of 1 non-key staff 3. Commercial Bank 14 departure of 2 non-key staff 4. Financial Centers 233 departure of 15 non-key staff • After risks have been identified, management determines how it will respond. Risk responses involves management assessing the effect on risk likelihood and impact as well as costs and benefits, selecting a response that brings the residual risk (with controls) with the desired risk tolerance. • Internal audit has performed its own assessment of risks facing the organization. It is tempting to take this assessment and start considering it as the organization’s risk register. If this happens, the risk maturity level of the organization will not develop as intended by management as it is likely to indicate that internal audit is responsible for risk management. 3