Agneya\'s Newsletter on Renewable Energy Sector and REC market in India

•

0 likes•333 views

Horizons V2 Issue 6

Recommended

Recommended

More Related Content

What's hot

What's hot (12)

Viewers also liked

Similar to Agneya\'s Newsletter on Renewable Energy Sector and REC market in India

Similar to Agneya\'s Newsletter on Renewable Energy Sector and REC market in India (20)

More from Agneya Carbon Ventures Private Limited

More from Agneya Carbon Ventures Private Limited (20)

Agneya\'s Newsletter on Renewable Energy Sector and REC market in India

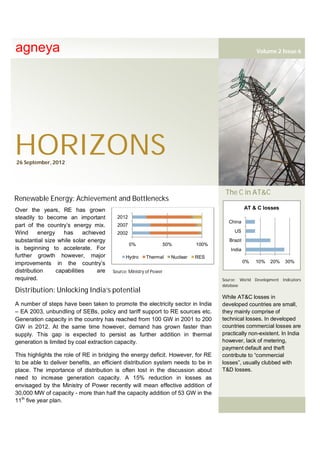

- 1. agneya Volume 2 Issue 6 HORIZONS 26 September, 2012 The C in AT&C Renewable Energy: Achievement and Bottlenecks Over the years, RE has grown AT & C losses steadily to become an important 2012 China part of the country’s energy mix. 2007 Wind energy has achieved 2002 US substantial size while solar energy Brazil 0% 50% 100% is beginning to accelerate. For India further growth however, major Hydro Thermal Nuclear RES improvements in the country’s 0% 10% 20% 30% distribution capabilities are Source: Ministry of Power required. Source: World Development Indicators database Distribution: Unlocking India’s potential While AT&C losses in A number of steps have been taken to promote the electricity sector in India developed countries are small, – EA 2003, unbundling of SEBs, policy and tariff support to RE sources etc. they mainly comprise of Generation capacity in the country has reached from 100 GW in 2001 to 200 technical losses. In developed GW in 2012. At the same time however, demand has grown faster than countries commercial losses are supply. This gap is expected to persist as further addition in thermal practically non-existent. In India generation is limited by coal extraction capacity. however, lack of metering, payment default and theft This highlights the role of RE in bridging the energy deficit. However, for RE contribute to “commercial to be able to deliver benefits, an efficient distribution system needs to be in losses”, usually clubbed with place. The importance of distribution is often lost in the discussion about T&D losses. need to increase generation capacity. A 15% reduction in losses as envisaged by the Ministry of Power recently will mean effective addition of 30,000 MW of capacity - more than half the capacity addition of 53 GW in the 11th five year plan.

- 2. 2 Solar Tariffs in India Tariff in (Rs./ Unit) Guj PT FY12 CERC PT FY12 Maha PT FY12 Distribution: Backbone of commercial models The REC Mechanism introduced last year provided RE generators a significant Kar State policy alternative to selling to cash strapped State Utilities. The non-solar REC market however has been muted of late. While generators have enthusiastically opted JNNSM for this mechanism, the corresponding demand is yet to reach expected levels. Phase I Batch This is due to slow implementation of RPO mechanism of which distribution II companies are key constituents. Odisha State policy One of the important reasons for poor Wind tariffs (Rs./ Unit) financial condition of Utilities is delayed 6.5 11.5 tariff hikes. Actual cost of power taking TN REC 4.04 4.94 Lower value Higher value into account increased fuel prices is not passed to consumers to avoid tariff TN PT 3.39 shocks. AP REC 3.5 4.4 Source: SERC Tariff orders, News articles Discoms in developed countries have AP PT 3.5 higher share of infirm renewable energy Recently concluded bidding Guj REC 4.11 5.01 in their energy mix. In India, discoms are process for solar power in various States as well as under unable to manage the grid with Guj PT 3.56 JNNSM resulted in surprisingly increasing share of renewable energy Kar REC 4.23 5.13 low tariffs. injected into the grid. Financial Financing sustainability is a prerequisite for Kar PT 3.7 However, investors have opted discoms to implement technological for projects under these policies developments. Commercials due to lower risk of default from Source: SERC orders, Lower REC price taken distribution companies. This is at Rs. 1.5/ unit and higher REC price taken at because investors have taken Bailout, not Reform Rs. 2.4/ unit (Average of 1.5 & 3.3) into account risk of payment Technology default under other commercial Regulators aim to transition to a process of competitive bidding for deciding the mechanisms. renewable energy tariff in the States. To achieve this, a competitive distribution sector able to provide open access is important. The Government has found a The REC mechanism however, temporary solution to the problems of distribution companies by reducing the is providing a major boost to debt servicing burden on the discoms. In the long run however, such financial solar energy especially through engineering will have limited impact on the sector. A calibrated plan of increase the captive route. in tariffs is required to ensure viability as well as higher efficiency.

- 3. 3 REC Market in September 2012 REC Inventory REC Trade Clearing Price Buy Bids Sell Bids Volume Traded Sep 2012 Rs. per REC REC Inventory Sep 2012 IEX 239,364 664,641 239,364 1,500 Non-Solar PXIL 25,082 46,530 25,082 1,500 2,64,446 IEX 1,317 1,094 735 12,500 5,17,432 Solar PXIL 525 527 425 12,900 8,51,628 Non-Solar prices wait for demand to catch up 5,98,642 The REC market in September 2012 recorded the highest volume of REC issuance ever resulting in the highest closing balance in the REC trade, Demand however remained subdued. Price realization remained at floor level of Rs. 1,500 with all the buy bids cleared at both IEX and PXIL. Even if we consider that only 20% of the RPO compliance is done through RECs, annual demand of RECs for FY 2012-13 should Source: REC Registry be more than 1 Crore. This demand is not yet reflected in the REC market as only less than 12 lakh RECs have been traded till September. This shows that while regulators have provided support to RE through RPO, more effort on enforcement is Solar RECs cross 1000 required. milestone 300 274 3,500 While non-solar RECs market 264 has been muted, solar RECs 3,000 250 236 have been picking up steadily 206 200 200 2,500 for the last few trading 172 169 sessions. 158 2,000 150 106 112 1,500 Solar REC witnessed a surge in 96 100 trading this month. With 1,160 71 1,000 46 certificates traded, the volume 50 500 this month more than tripled volume of last trading session. - - Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep-12 The trade also saw a healthy 2011 2011 2011 2011 2012 2012 2012 2012 2012 2012 2012 2012 price realization at Rs. 12,500 per certificate at IEX. Value of IEX and PXIL Whole Volume Trade in Thousands Price at IEX (RHS) Price at PXIL (RHS) trade more than tripled and Source: IEX and PXIL exceeded Rs.1.4 Crores in this trading session.

- 4. Capacity Registered, MW 600 3500 4 State-wise Registered 500 3000 Capacity, April 2012 to 384 2500 400 date 335 2000 300 271 250 State MW 1500 Tamil Nadu 329 Maharashtra 253 200 172 158 149 1000 Gujarat 135 113 106 107 Karnataka 126 93 100 73 62 500 Rajasthan 27 Madhya Pradesh 22 Uttar Pradesh 20 0 0 Chhattisgarh 12 Odisha 5 Himachal Pradesh 4 Punjab 0 Uttarakhand 0 Cum. Registered till Date(RHS) Registered Kerala 0 Source: REC Registry J&K 0 Haryana 0 In total, 107 MW of capacity was registered in September. With this addition, the Total 933 capacity registered in this financial year has touched 933 MW. Total trade value of solar and non-solar RECs exceeded Rs. 40 Crore in this trading session. Source-wise Registered Capacity, April 2012 to date Source MW Wind 731 Biomass 97 Bio-fuel cogen 81 Solar PV 18 Small Hydro 6 Total 933 Source: REC Registry agneya Agneya is promoted by alumni of IIM Ahmedabad and IIM Bangalore. We provide services in the following areas – Renewable Energy – advising clients on the best possible portfolio of renewable energy (wind, solar, bio) across tariff regimes, technology options, electricity sales structuring and availing incentives like REC and GBI. Renewable Energy Regulations – advising clients on regulatory aspects of electricity market, options for realizing the maximum value from their energy assets and minimizing costs related to regulatory compliance including addressing RPO. Carbon & Energy – measuring carbon footprint, current/future energy profiling, and setting up energy management systems to assess risks and opportunities related to energy security and climate change. Sustainability – building robust long term foundations for business i.e. managing economic, environmental and social aspects of business. These include establishing sustainability management framework and reporting as per GRI guidelines. For further information on Renewable Energy Certificates or other services, please contact us at – E-mail – rahul@agneya.in | Phone – +91-20-41203800, +91-88 06 07 07 83 | Website – www.agneya.in