Download to read offline

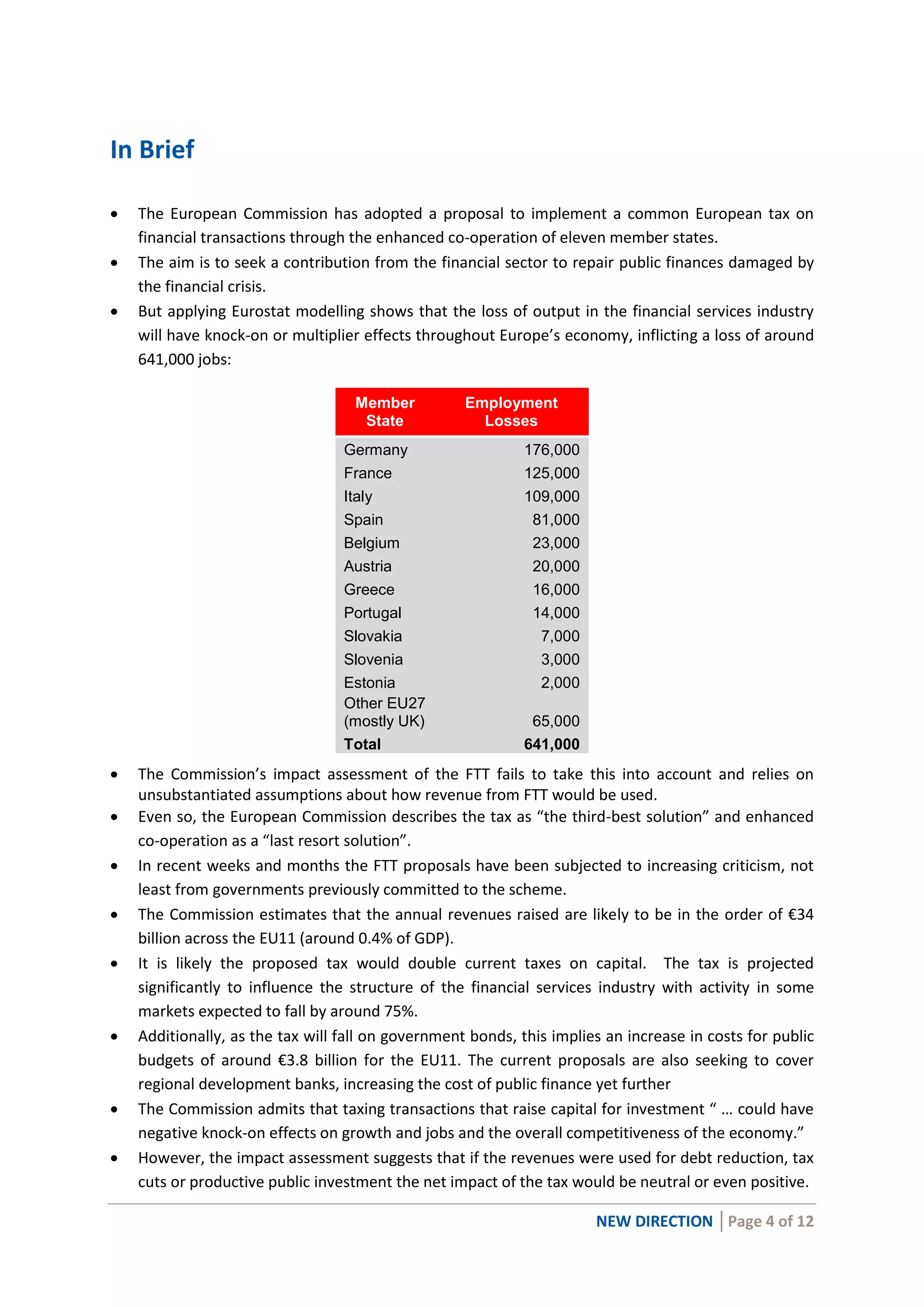

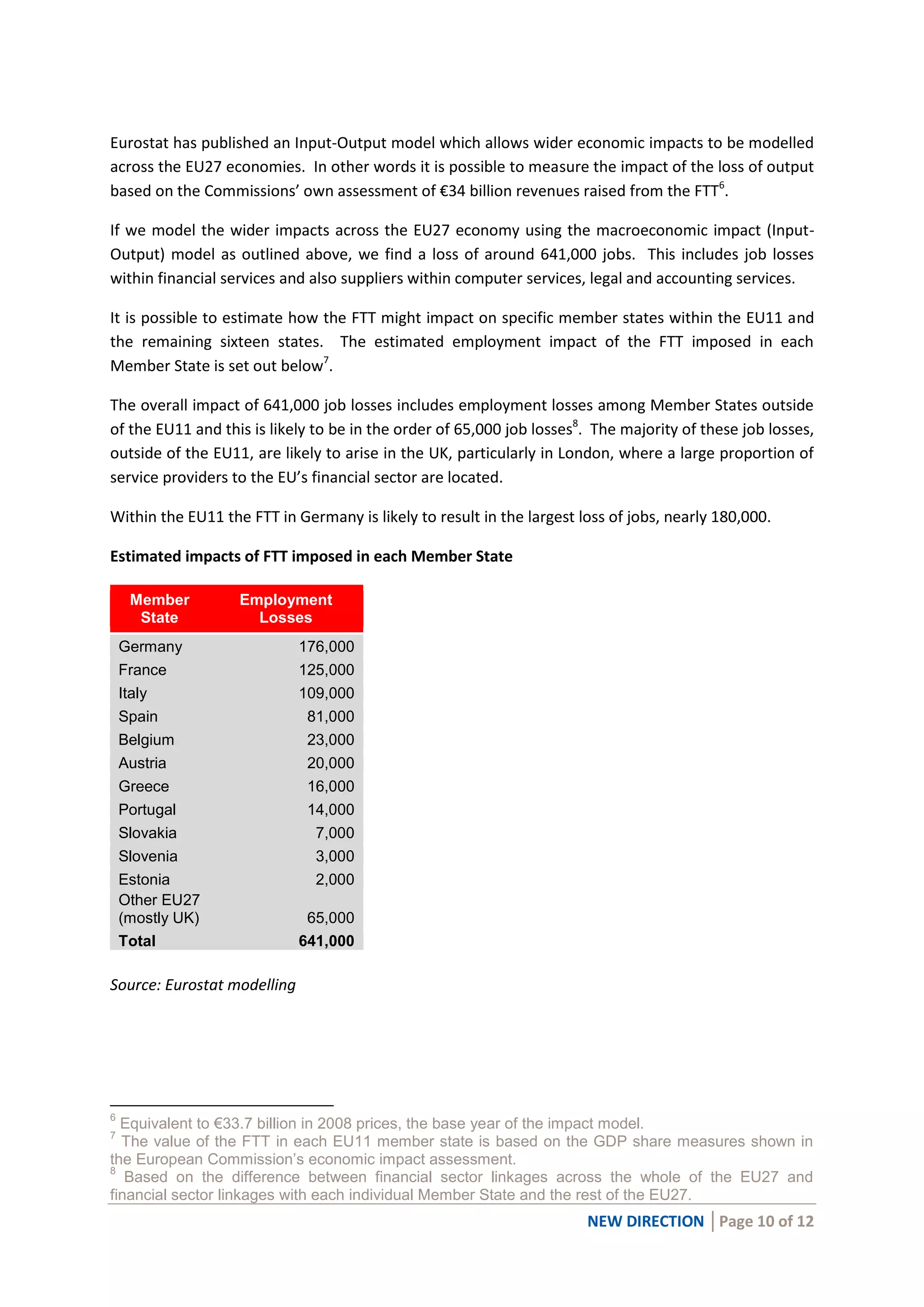

The document summarizes a report analyzing the economic impact of implementing a European Financial Transactions Tax (FTT). It finds that applying the tax would result in significant job losses across Europe. Specifically: - Modeling estimates the tax would cause over 641,000 job losses in the EU, including over 176,000 in Germany, 125,000 in France, and 109,000 in Italy. - The tax is projected to double current taxes on capital and reduce activity in some financial markets by around 75%. - Imposing the tax risks reducing economic growth, investment, and job creation. It could also undermine public finances by taxing government bond transactions. - The European Commission's impact assessment of the FTT fails