Download as PDF, PPTX

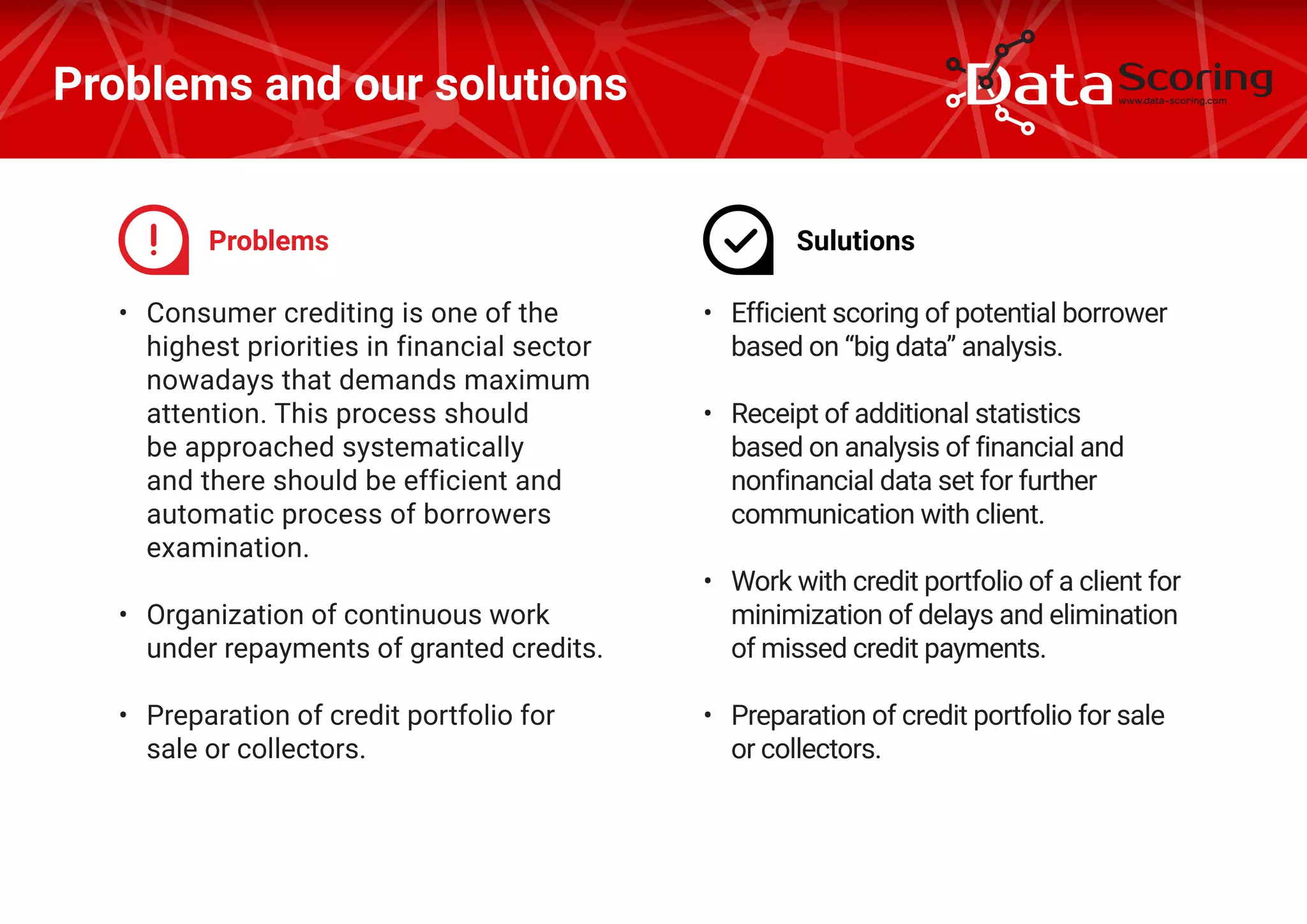

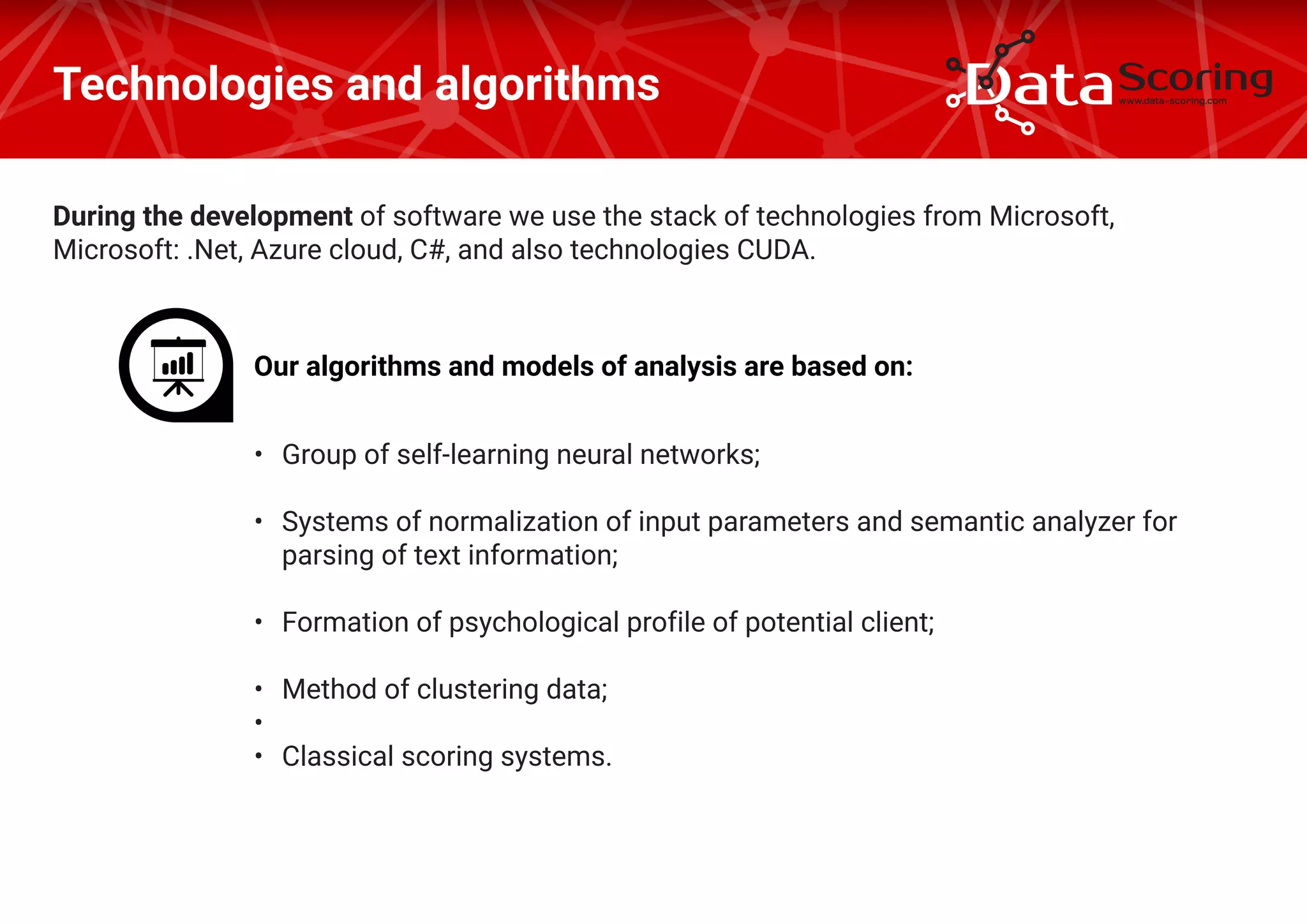

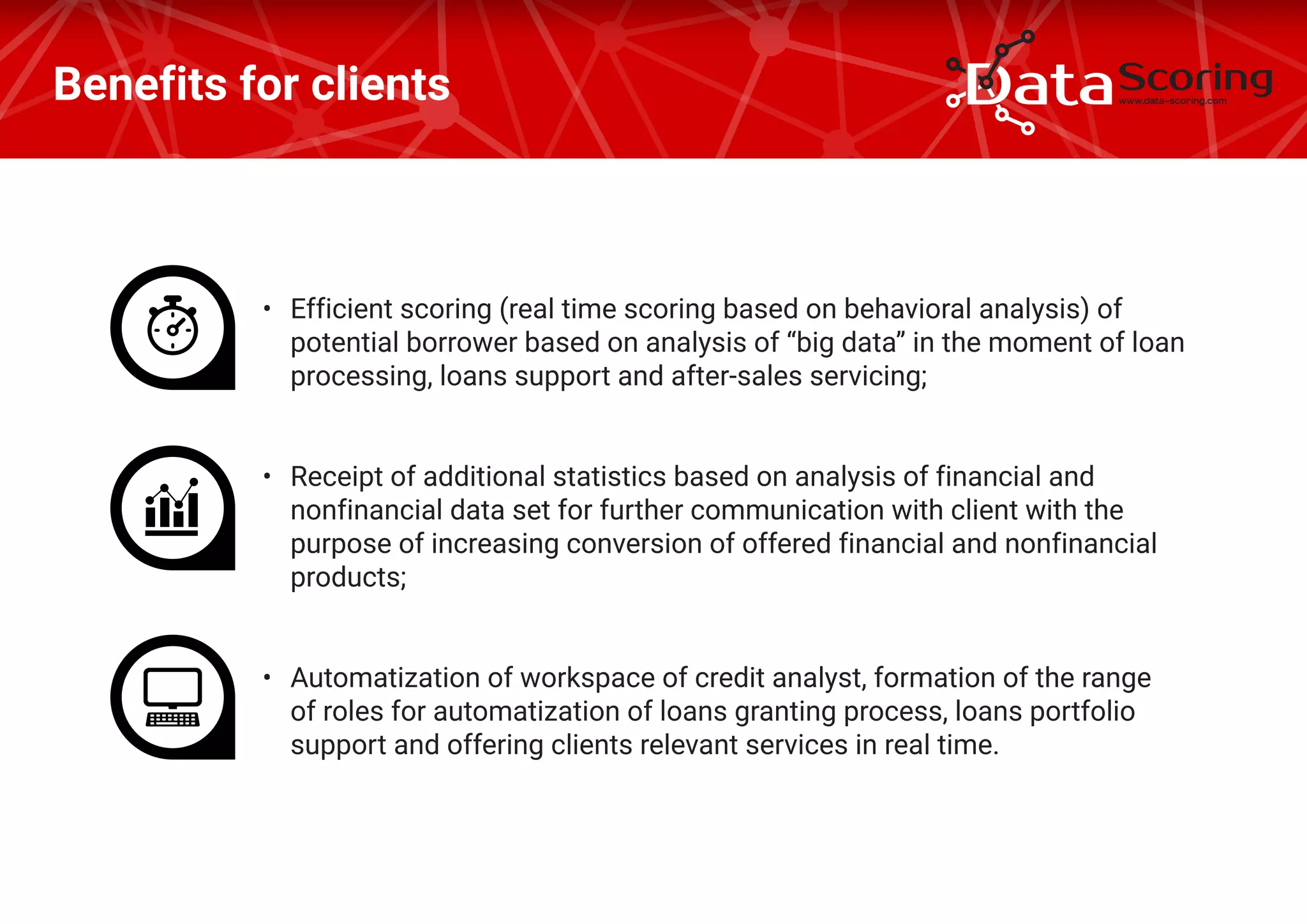

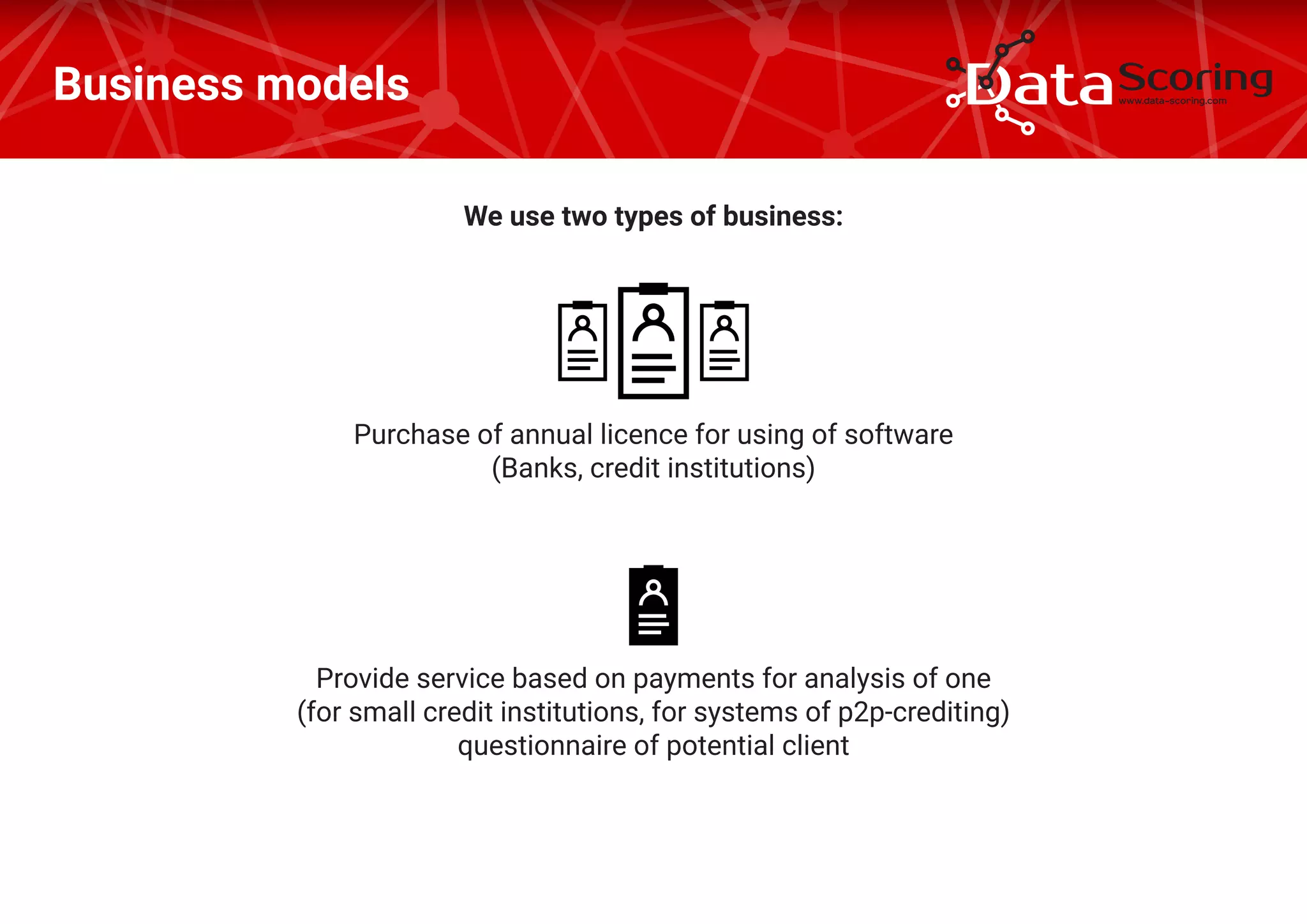

The document discusses the significance of big data in consumer credit scoring, emphasizing systematic borrower examination processes and minimizing payment delays. It outlines technology stacks and algorithms used for real-time scoring, client communication, and automating credit analyst workspaces, recommending a business model based on software licenses and pay-per-analysis services. The team includes professionals with extensive backgrounds in IT and software development, aimed at supporting financial institutions that provide credit services.