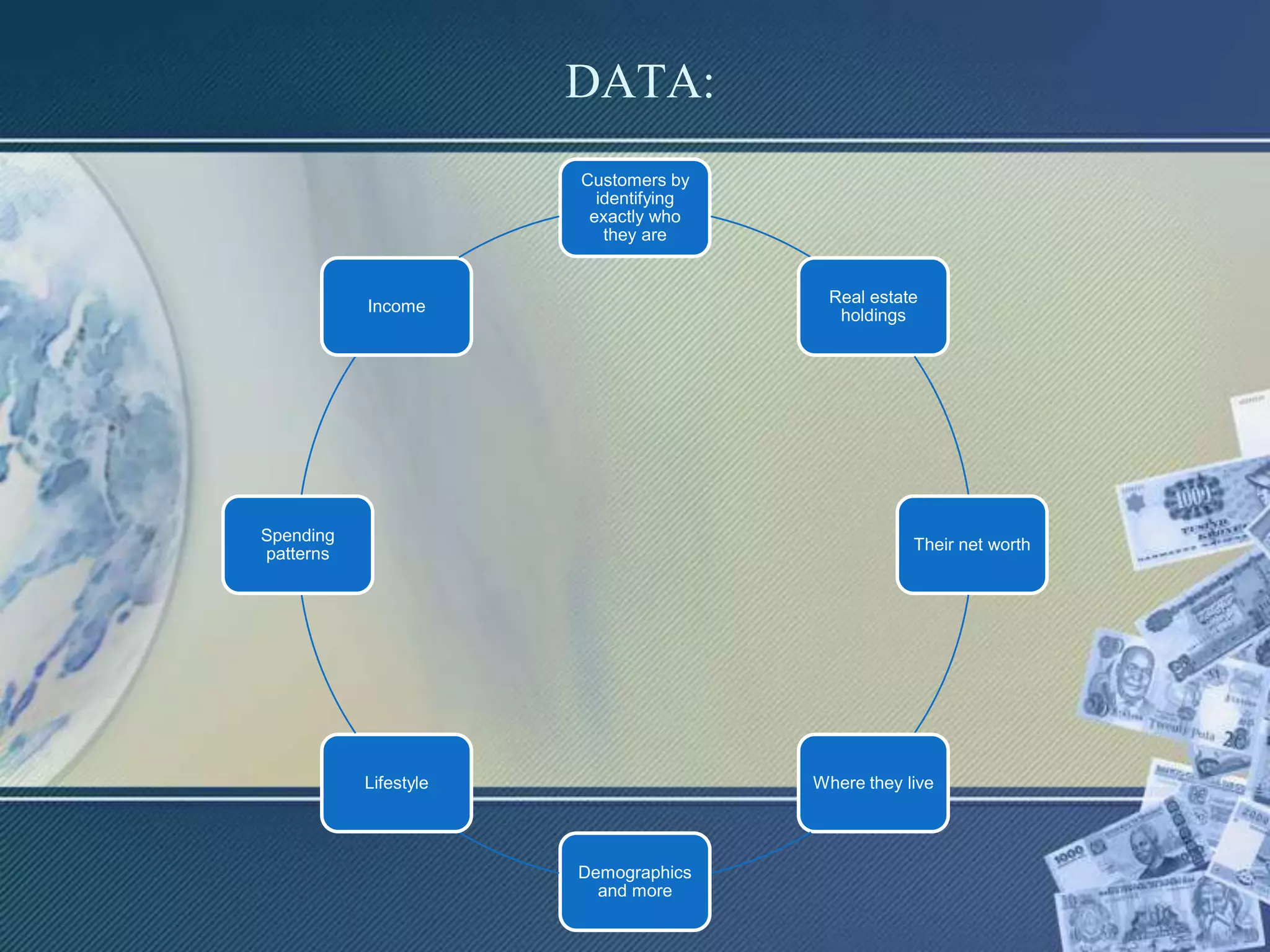

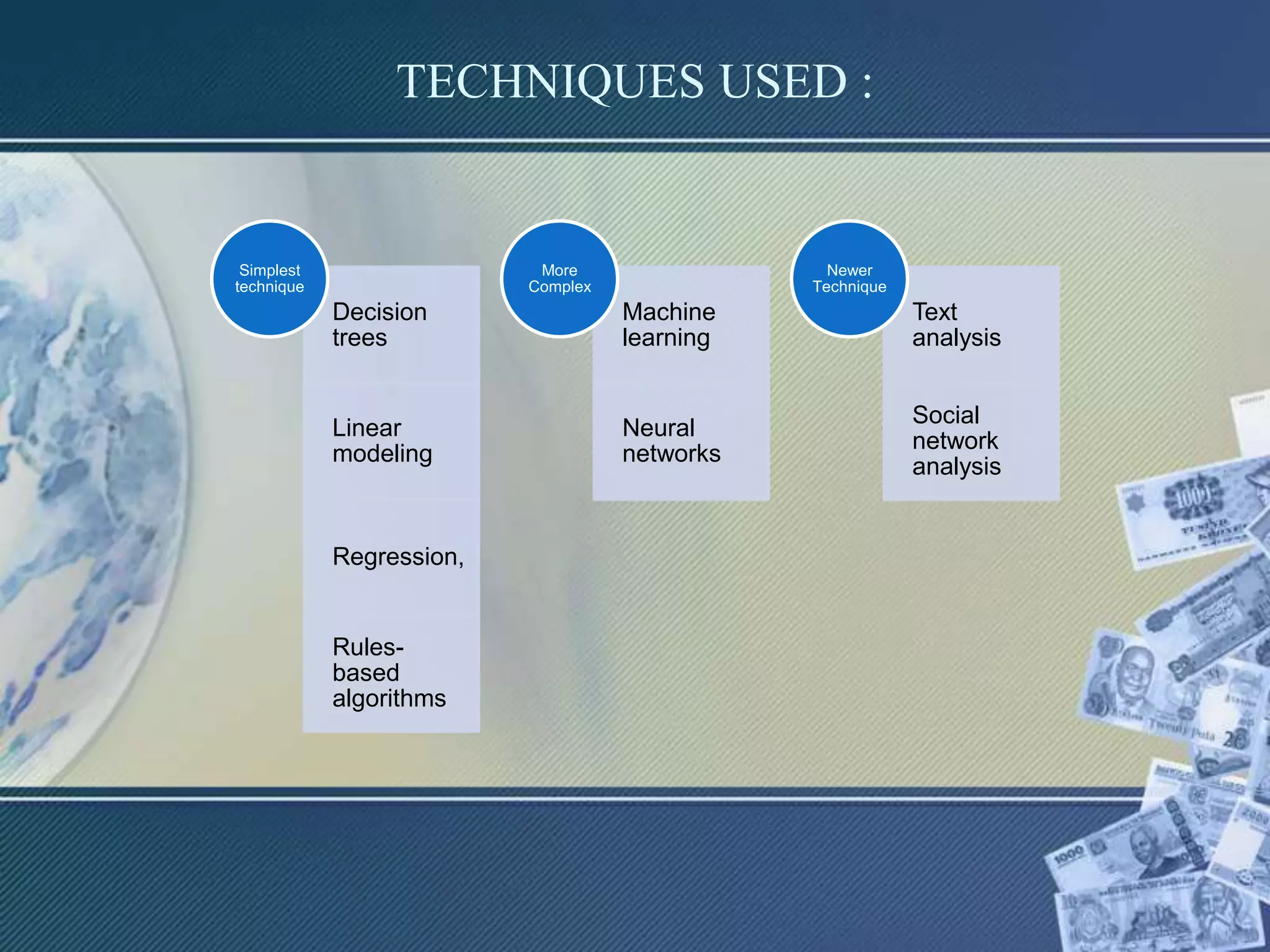

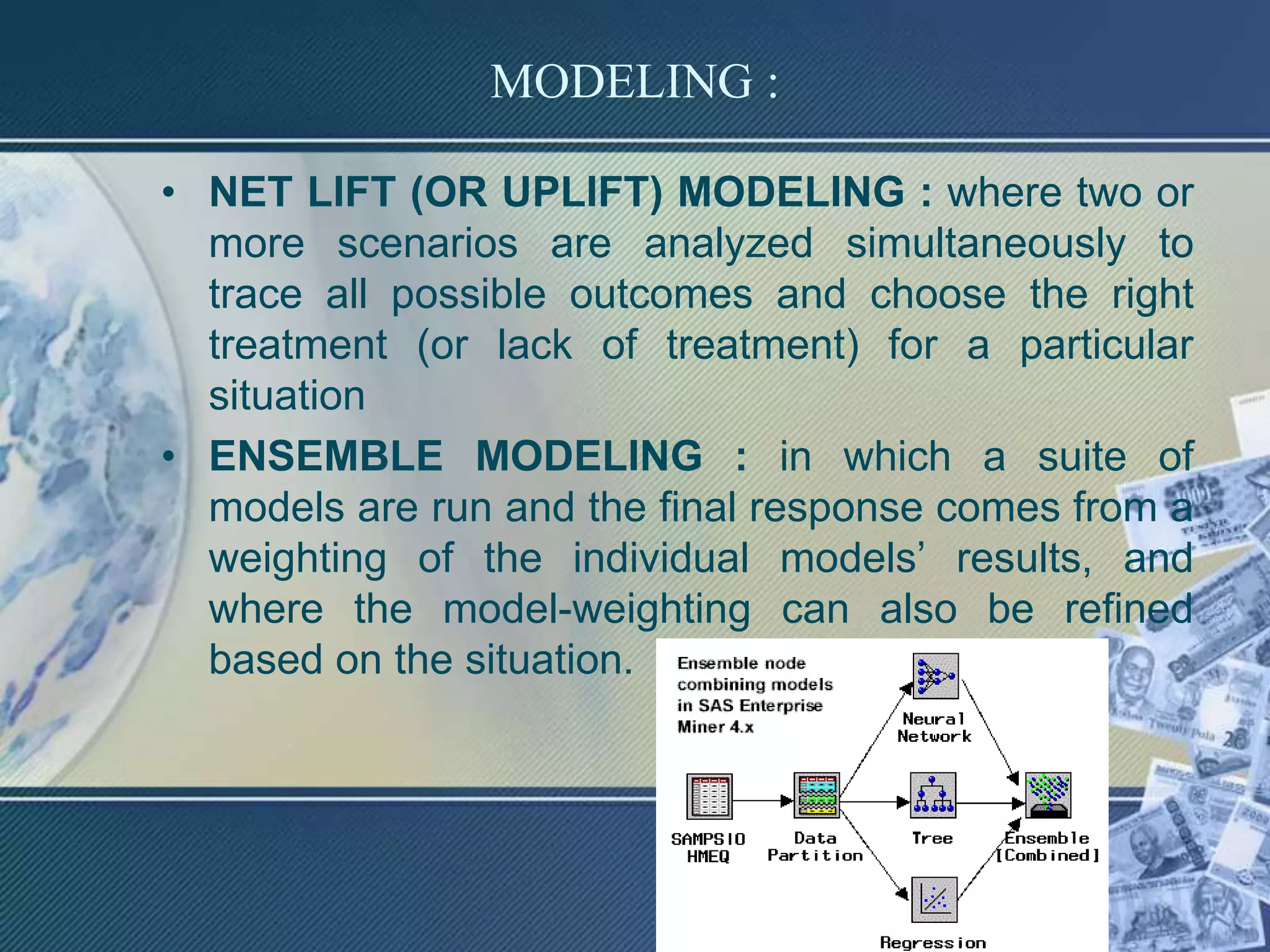

1) High performance business computing enables organizations to analyze vast amounts of internal and external data using cost-effective systems and analytical methodologies. 2) Techniques like decision trees, machine learning, and text analysis are used to analyze customer, demographic, and financial data to identify patterns and predict outcomes. 3) Modeling approaches like ensemble modeling and uplift modeling analyze multiple scenarios and models to identify the most effective predictions and treatments.