Downloaded 99 times

![A17 - 25

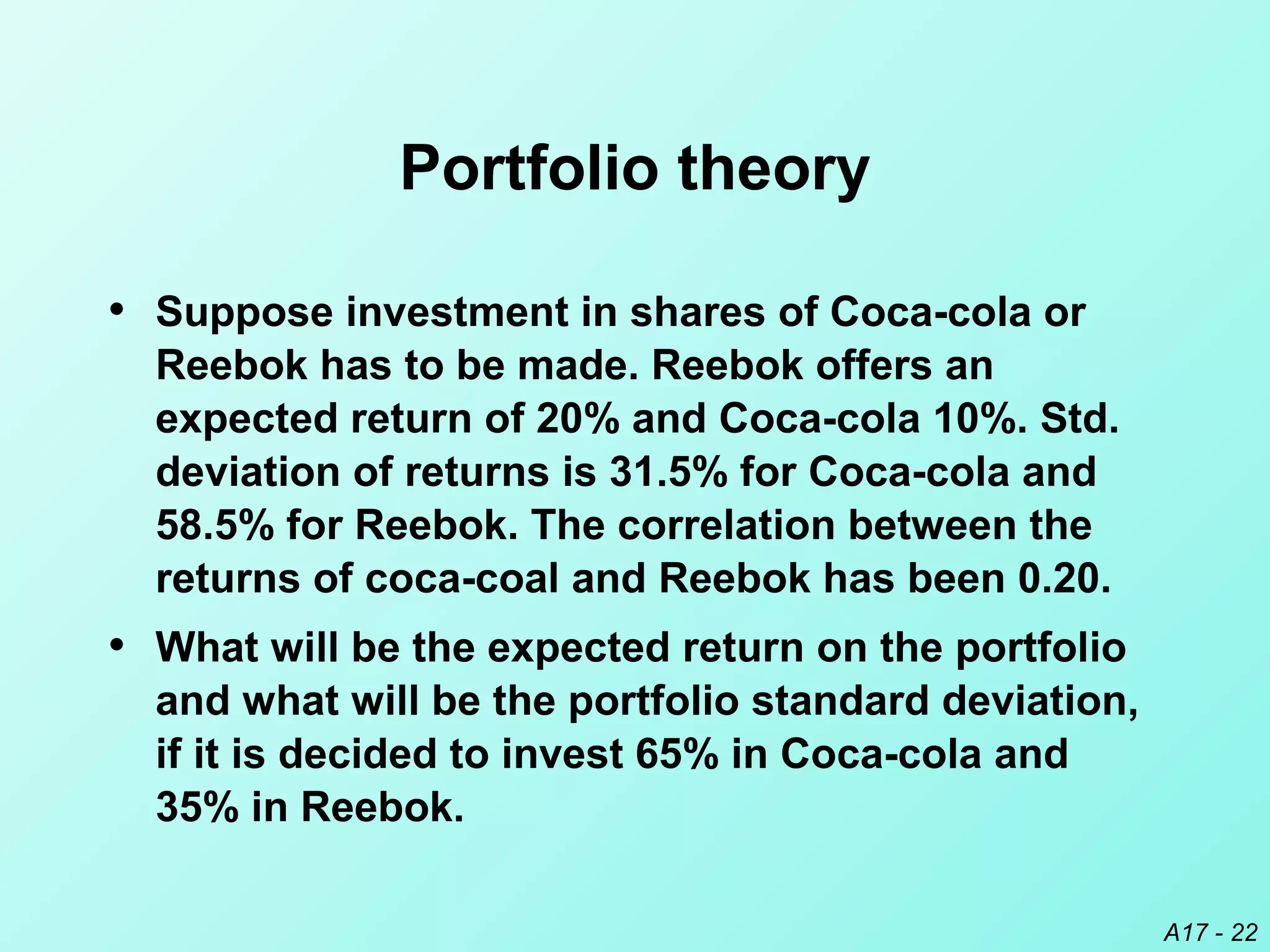

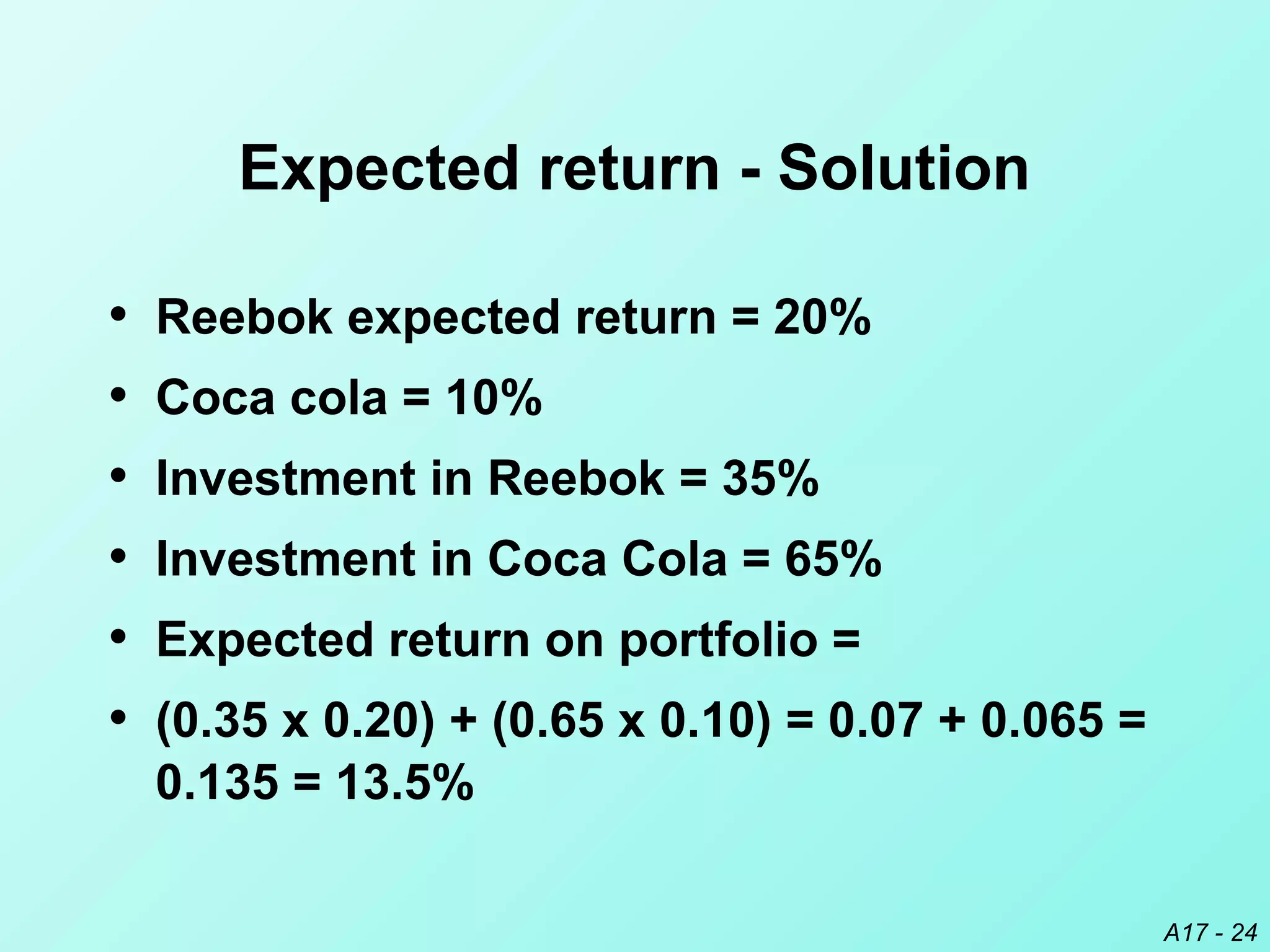

Solution

• Variance = [(0.652

) x (31.52

)] +

• [(0.352

) x (58.52

)] +

• 2(0.65 x 0.35 x 0.2 x 31.5 x 58.5)

• = 1006.1

• Std.deviation = 31.7](https://image.slidesharecdn.com/multinationalcostandcapitalstructure-131010060713-phpapp01/75/Multinational-cost-and-capital-structure-25-2048.jpg)

![A17 - 33

Impact of Multinational Capital Structure

Decisions on an MNC’s Value

( ) ( )[ ]

( )∑

∑

+

×

=

n

t

t

m

j

tjtj

k1=

1

,,

1

ERECFE

=Value

E (CFj,t ) = expected cash flows in

currency j to be received by the U.S. parent at the

end of period t

E (ERj,t ) = expected exchange rate at

which currency j can be converted to dollars at

Parent’s Capital Structure

Decisions](https://image.slidesharecdn.com/multinationalcostandcapitalstructure-131010060713-phpapp01/75/Multinational-cost-and-capital-structure-33-2048.jpg)

The document discusses how multinational corporations determine their cost of capital and establish optimal capital structures. It explains that an MNC's cost of capital may differ from domestic firms due to their size, access to international markets, diversification across countries, and exposure to exchange rate and country risks. The cost of capital also varies by country based on interest rates, risk premiums, and tax laws. An MNC considers these corporate and country characteristics when deciding how much debt and equity to use in different subsidiaries to minimize its overall cost of capital.