Downloaded 312 times

![What are the characteristics of a

record?

• Records are evidence of actions and transactions

• Records should support accountability, which is

tightly connected to evidence but which allows

accountability to be traced;

• Records are related to processes, i.e.

“information that is generated by and linked to

work processes” [Thomassen, 2001, p 374];

• Records must be preserved, some for very short

time and some permanently.](https://image.slidesharecdn.com/recordsbtchrm-150515215149-lva1-app6891/75/INTRODUCTION-TO-RECORDS-18-2048.jpg)

Here are the key points on how records can be categorized according to their use or value: - Administrative value: Records containing information on procedures, operations, decisions needed to support current business functions. - Fiscal value: Records providing evidence of financial transactions and accounting needed for auditing like invoices, receipts, payment records. - Legal value: Records containing information needed to protect the legal and financial interests of an organization in case of litigation or investigation. - Evidential value: Records providing proof of decisions made, actions taken etc. important for accountability and good governance. - Historical/informational value: Records important for historical research that give an overview of the development of an organization or society over time.

Overview of records management, its benefits, and importance for organizations including efficiency and cost reduction.

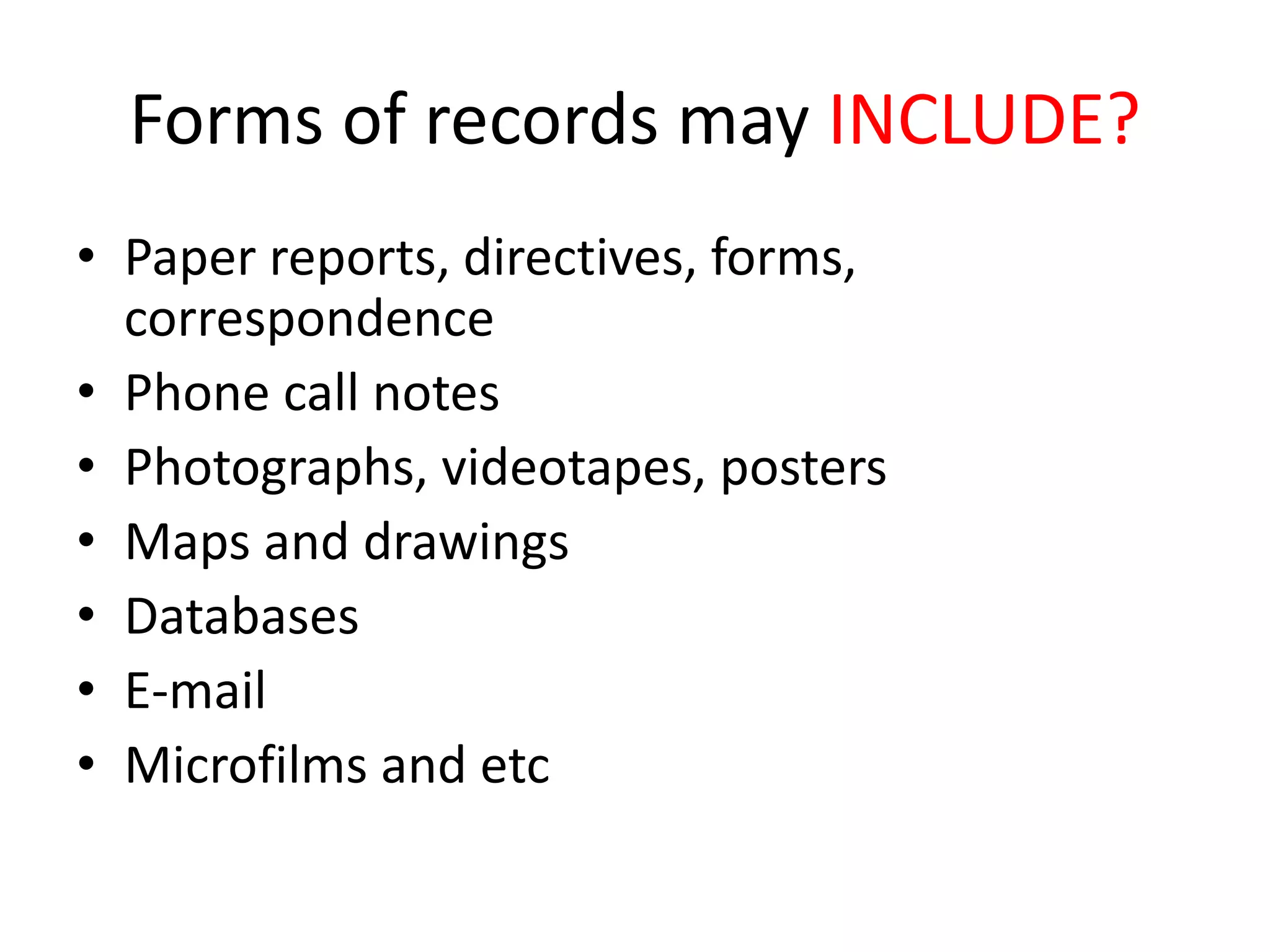

Explanation of what constitutes a record, including legal definitions and the forms records can take within an organization.

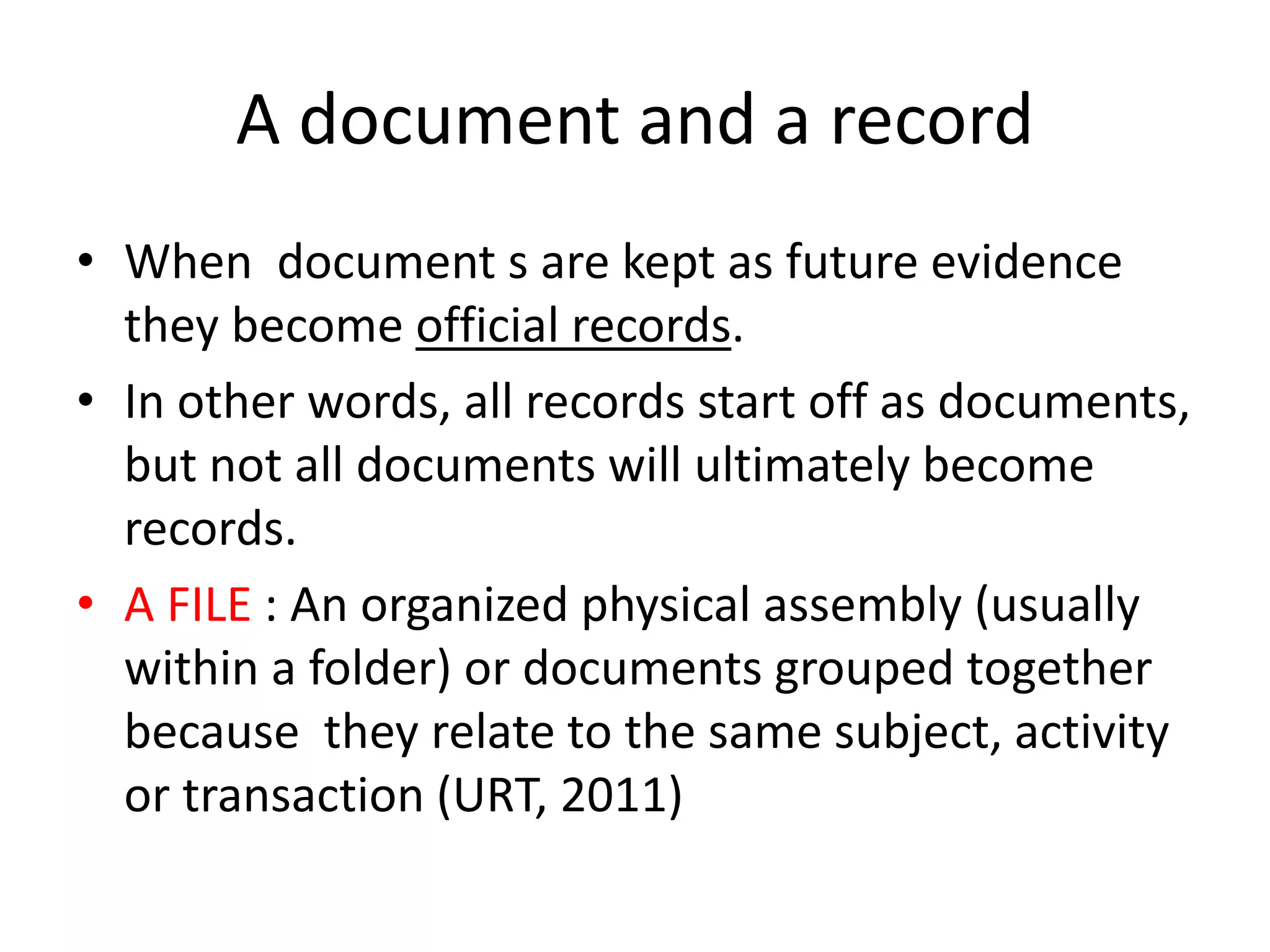

Distinguishing between documents and records, and defining a file as an organized collection of related documents.

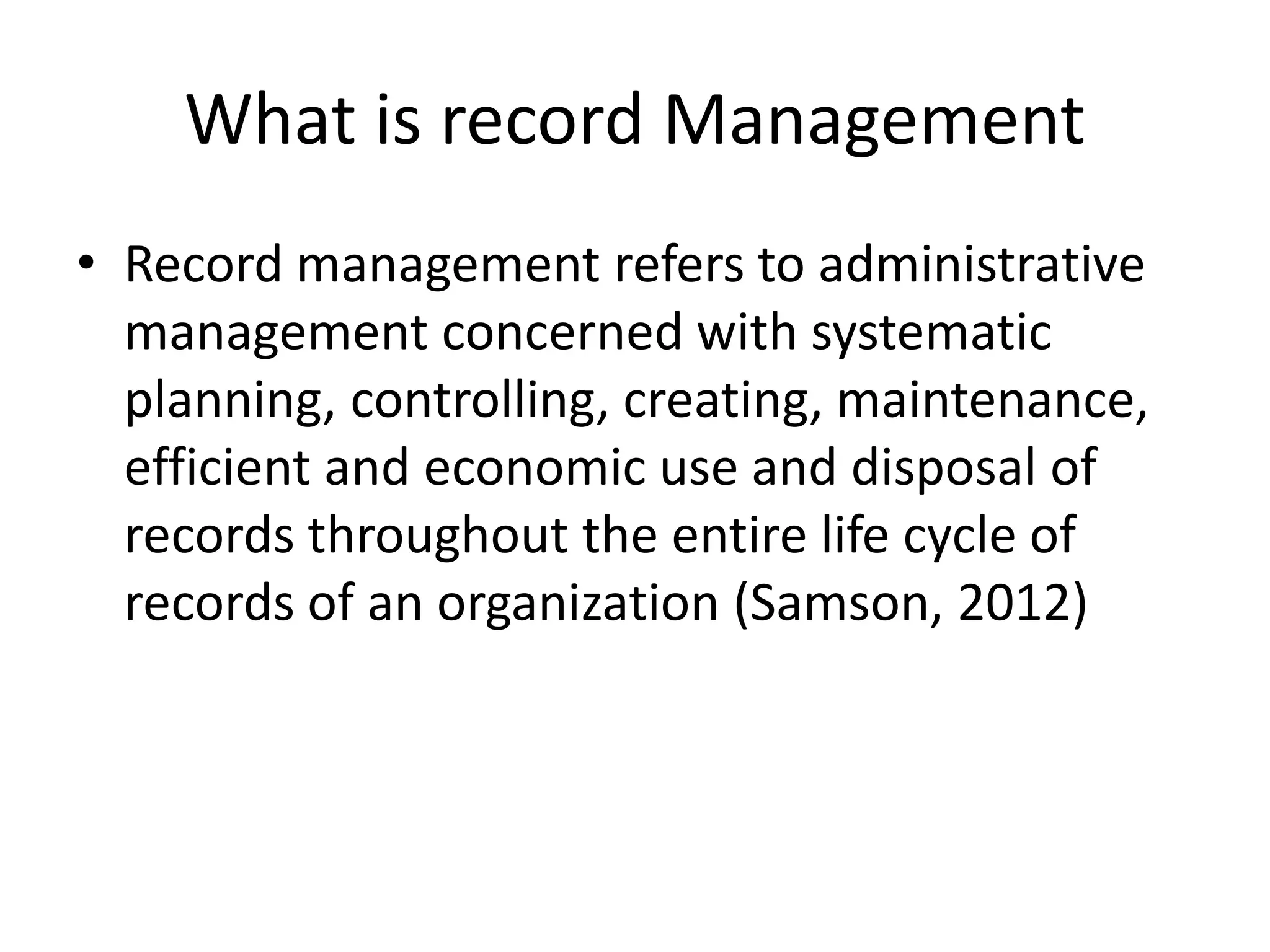

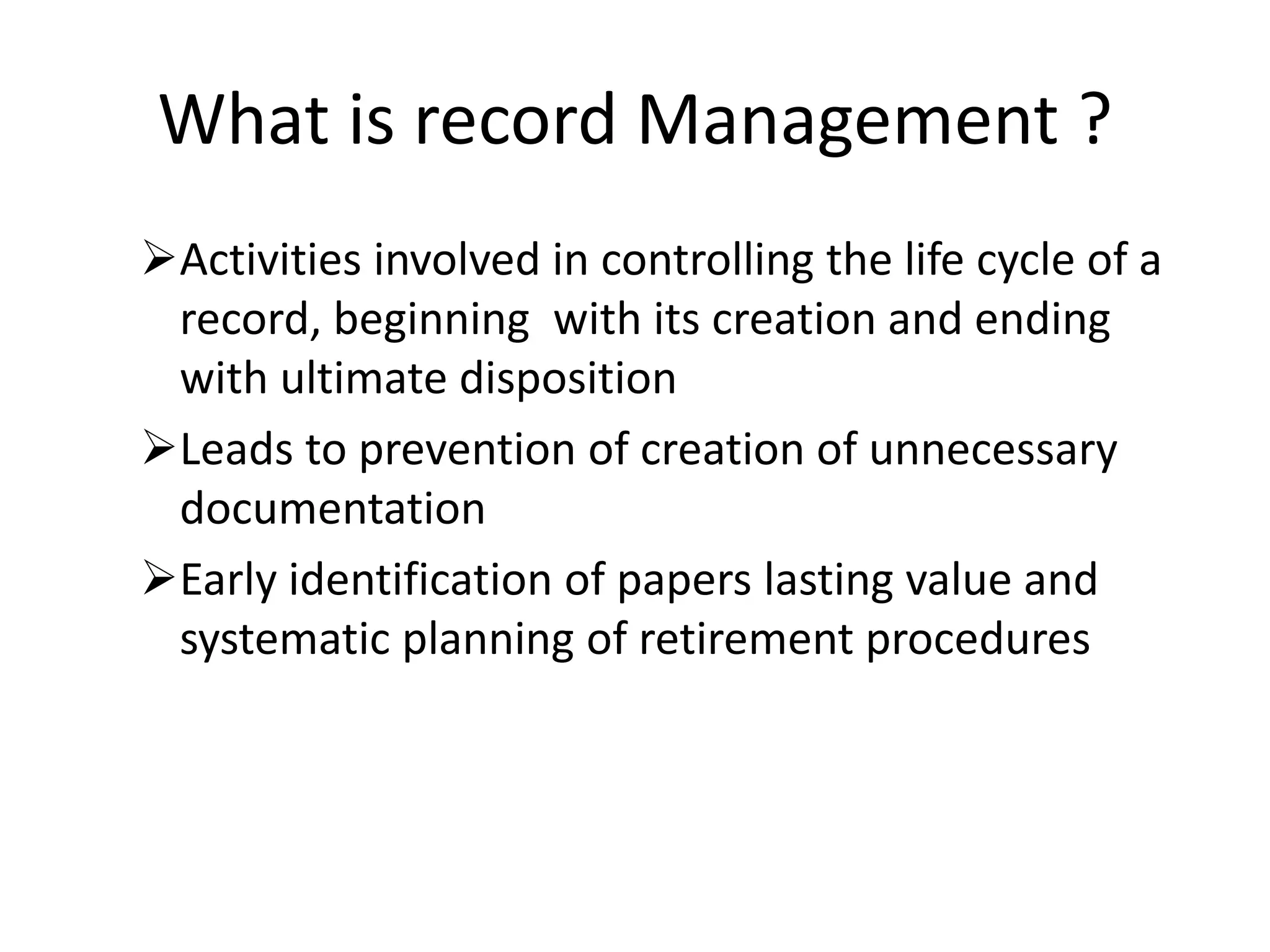

Defining record management, its lifecycle, types of records, and materials that do not qualify as records.

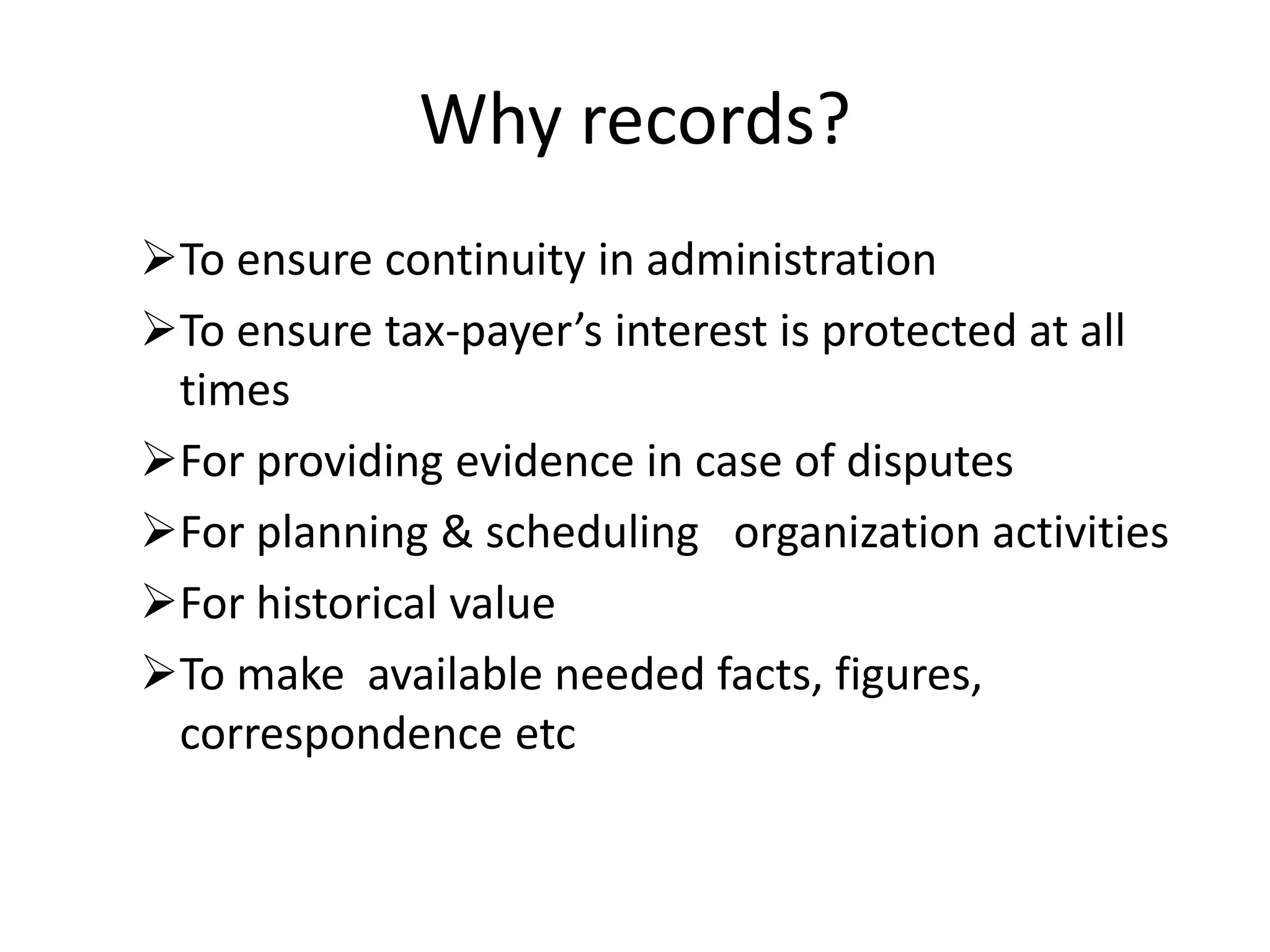

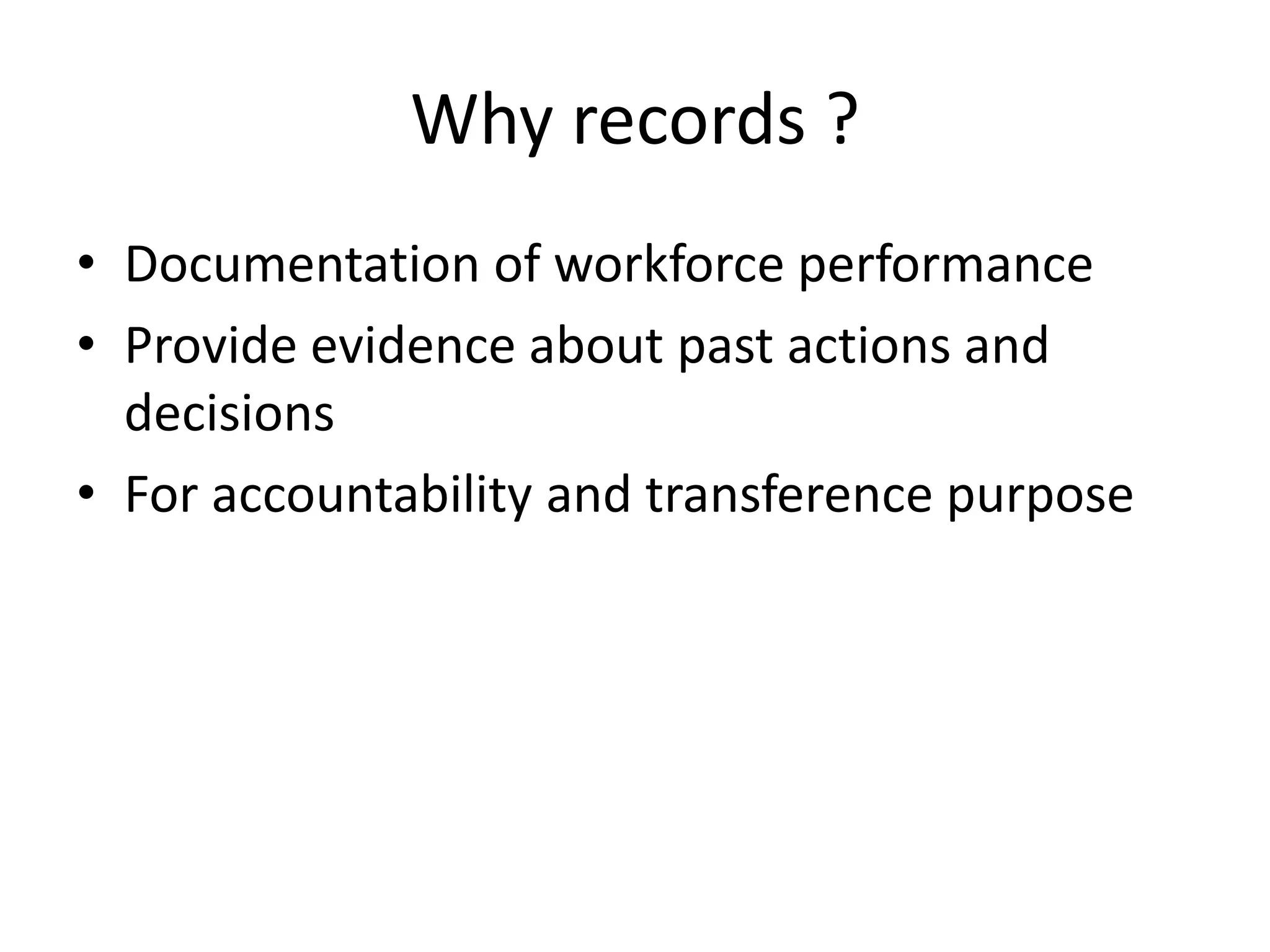

Reasons for maintaining records including legal, administrative, and historical purposes, as well as performance documentation.

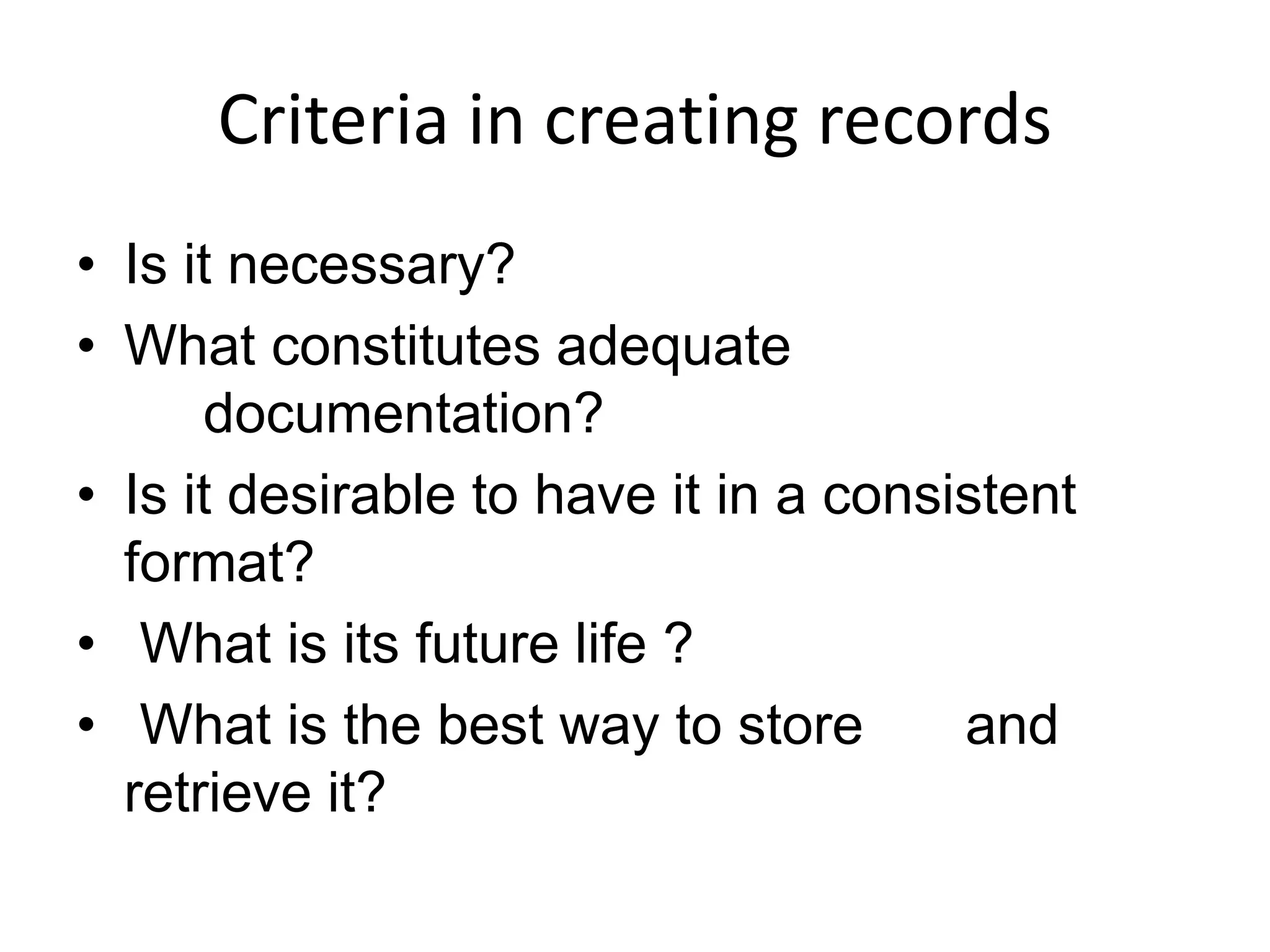

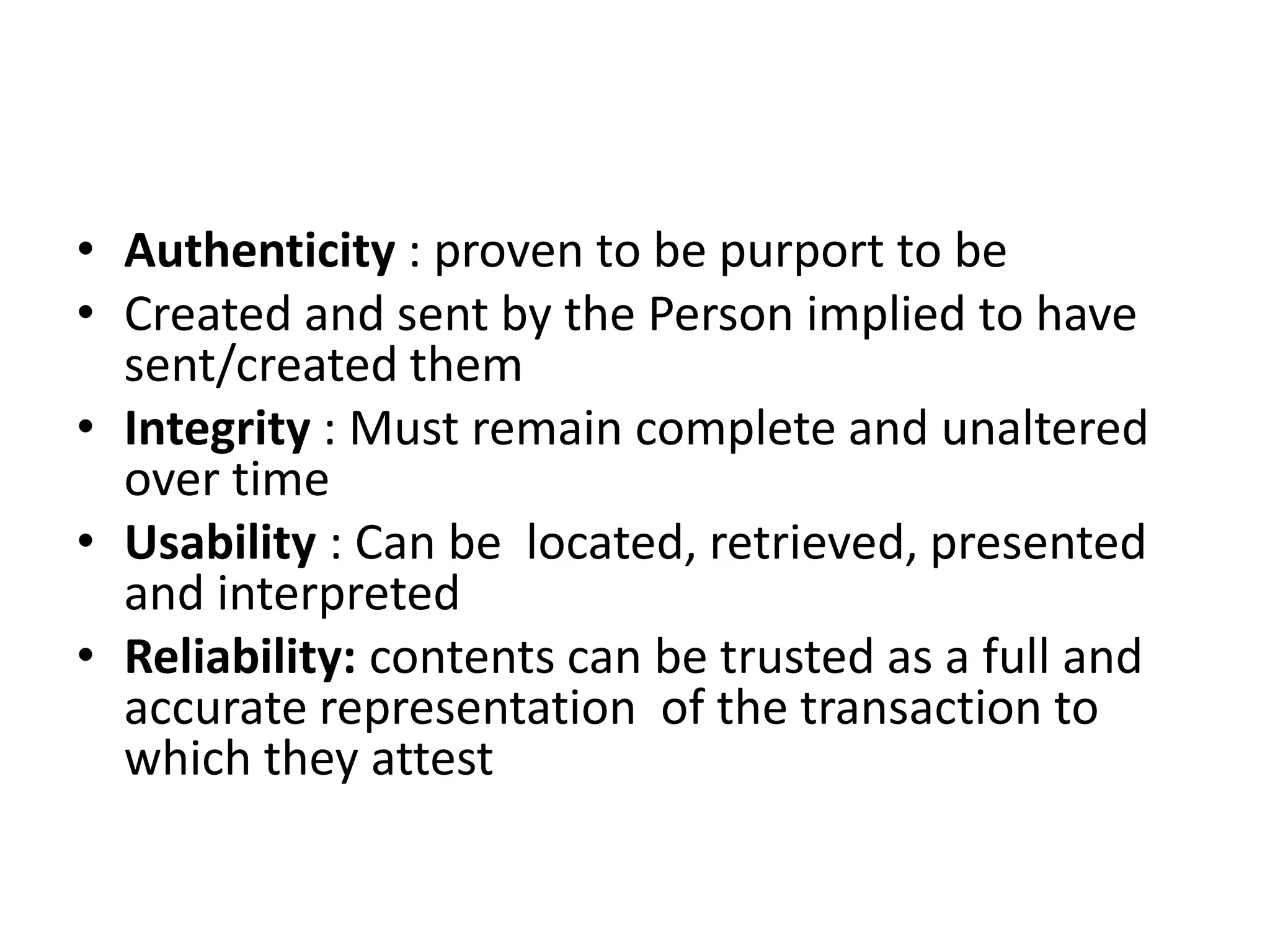

Key criteria for creating records, characteristics like authenticity, integrity, and how they support decision-making and accountability.

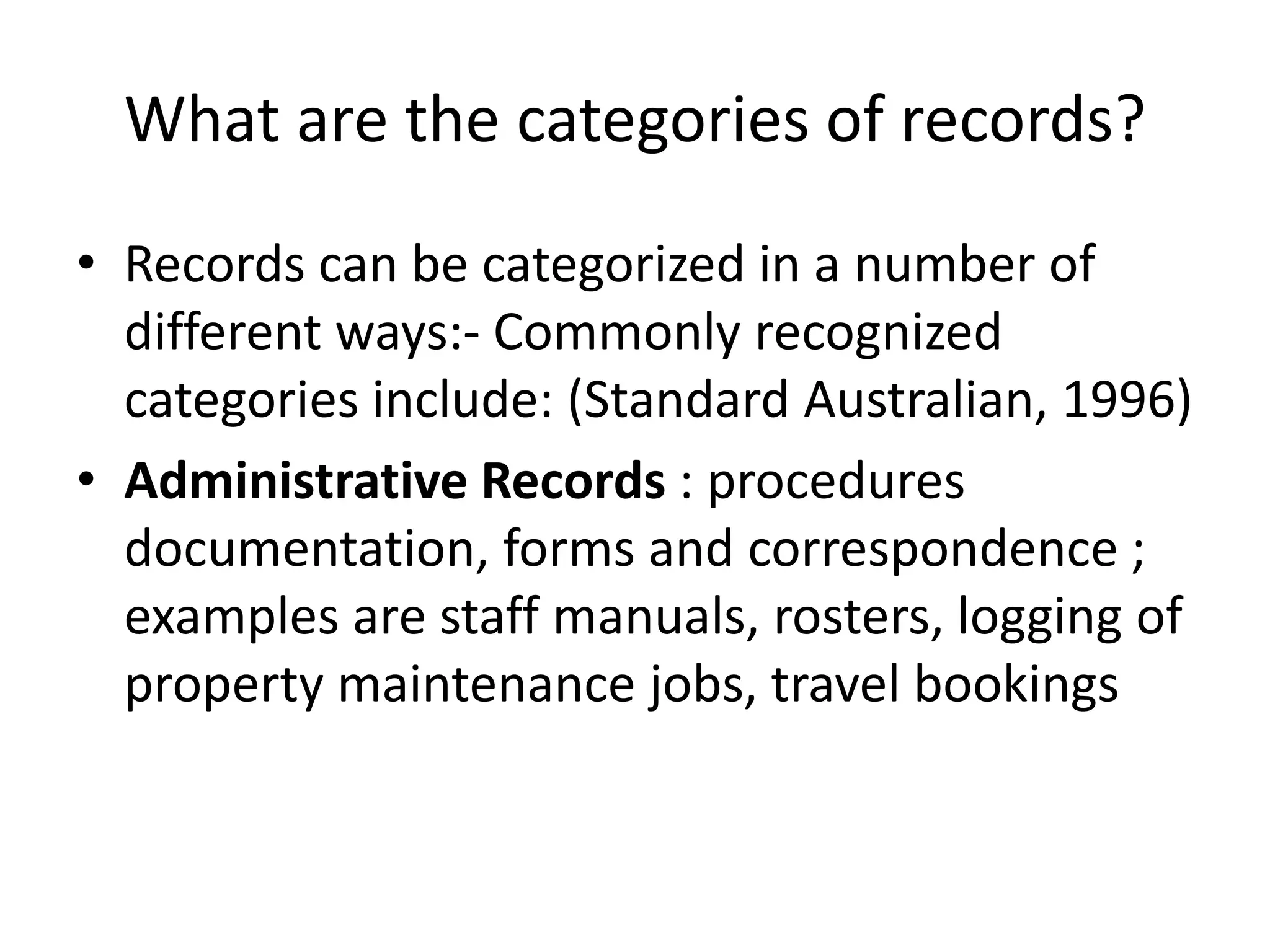

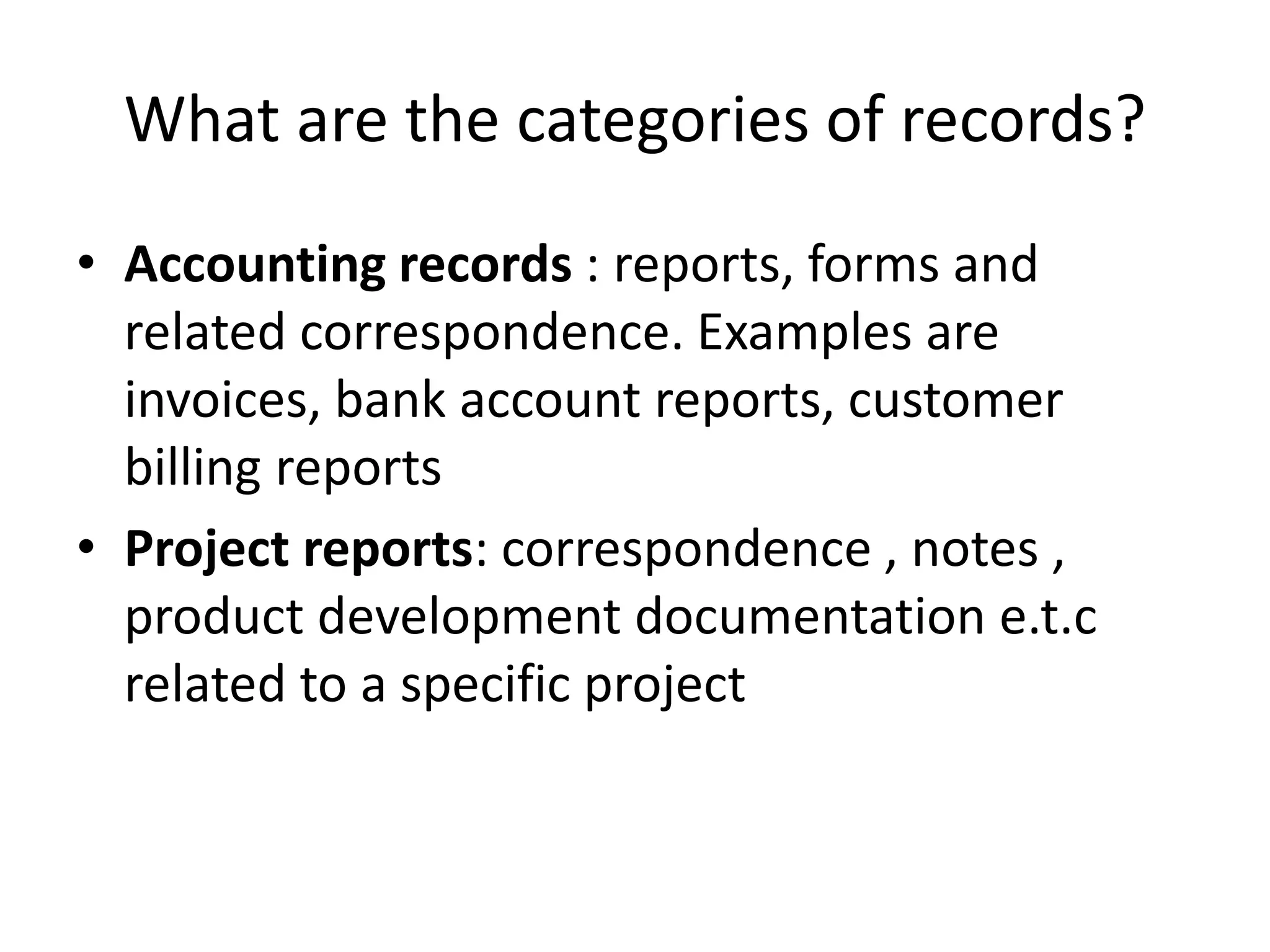

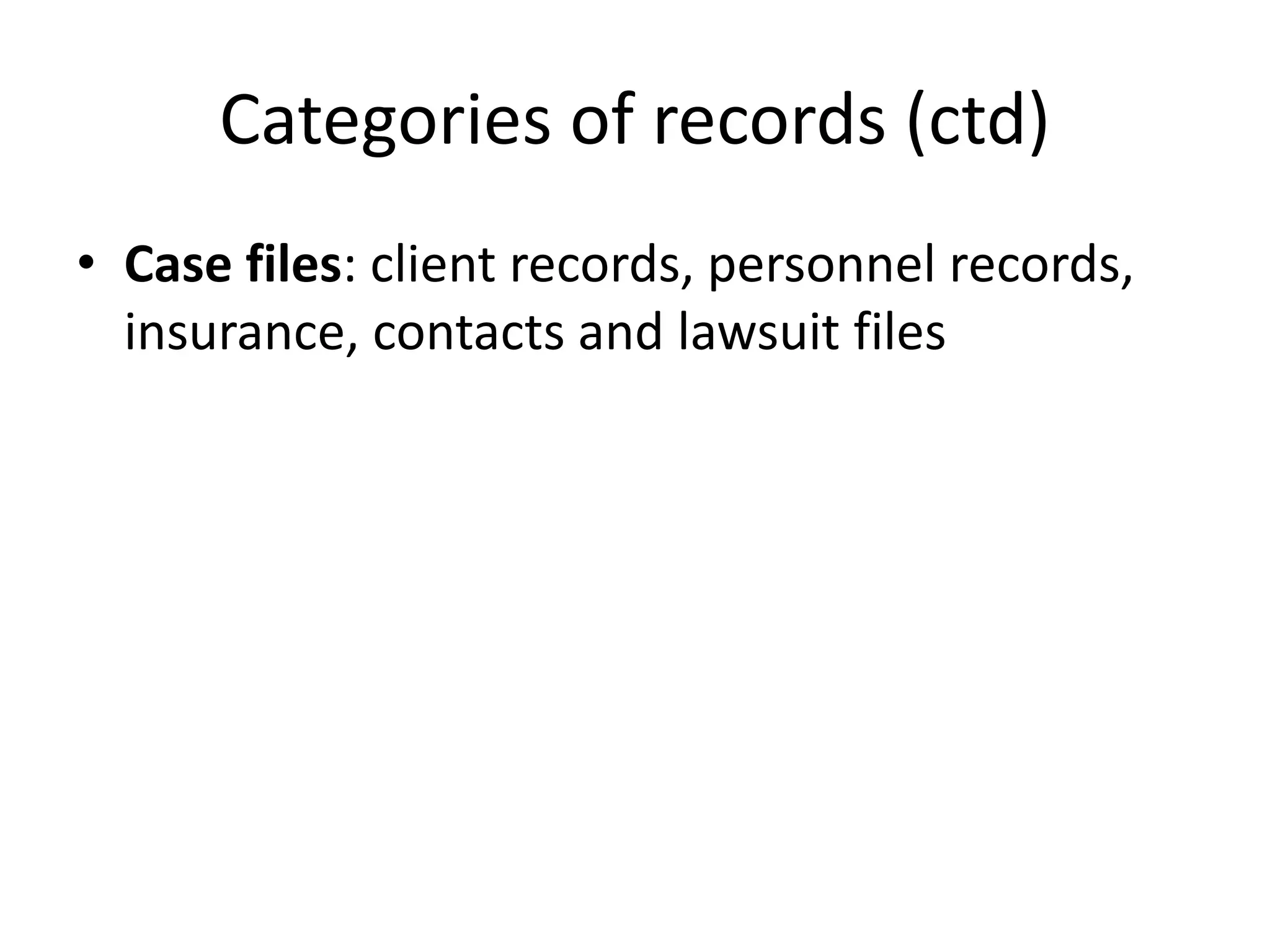

Different categories of records such as administrative, accounting, and project-specific, emphasizing their importance in various contexts.

![E. Bryan - An Introduction To Records Management [Barbados Community College]](https://cdn.slidesharecdn.com/ss_thumbnails/e-bryan-anintroductiontorecordsmanagementbarbadoscommunitycollege-090312123710-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)