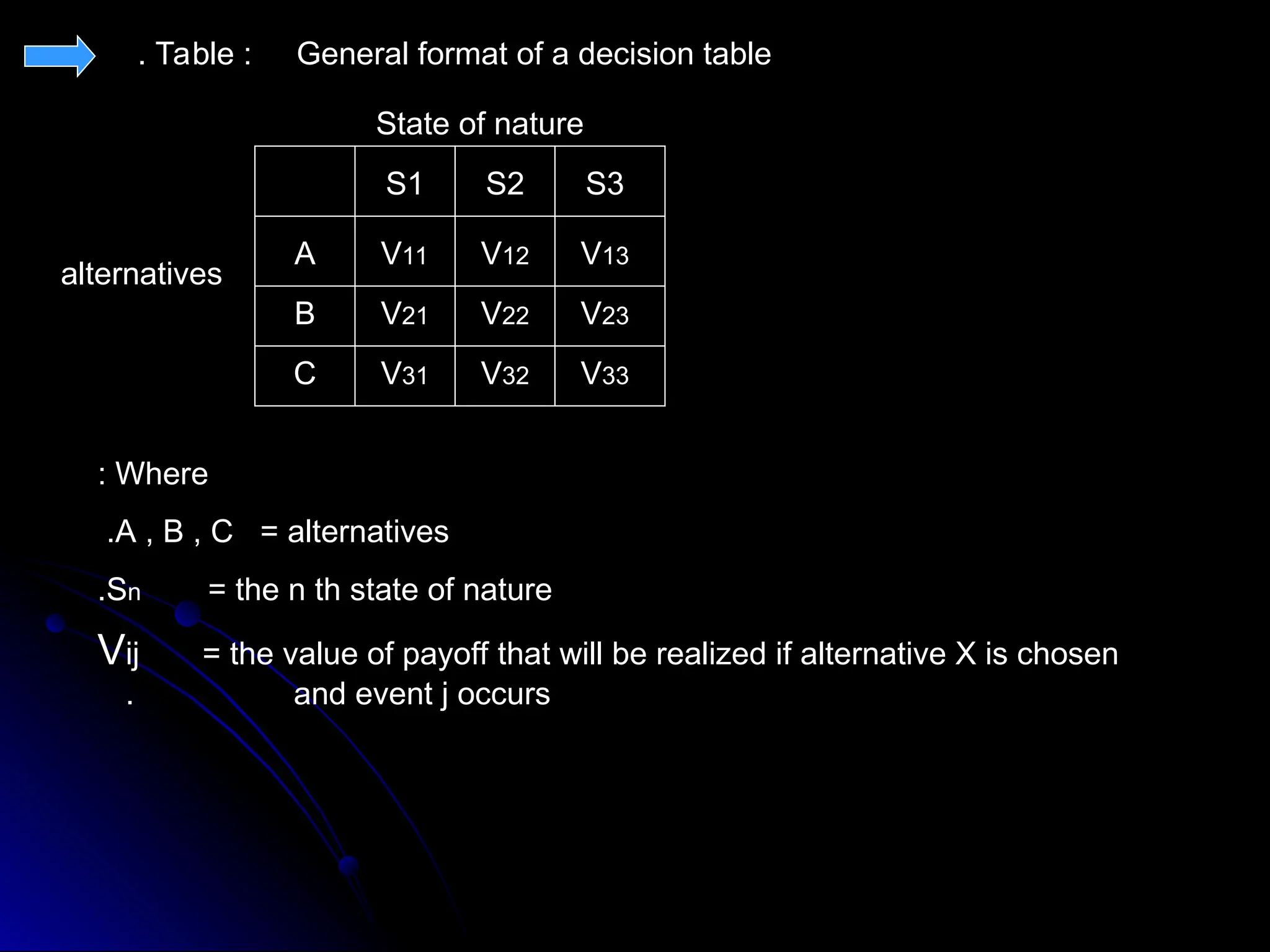

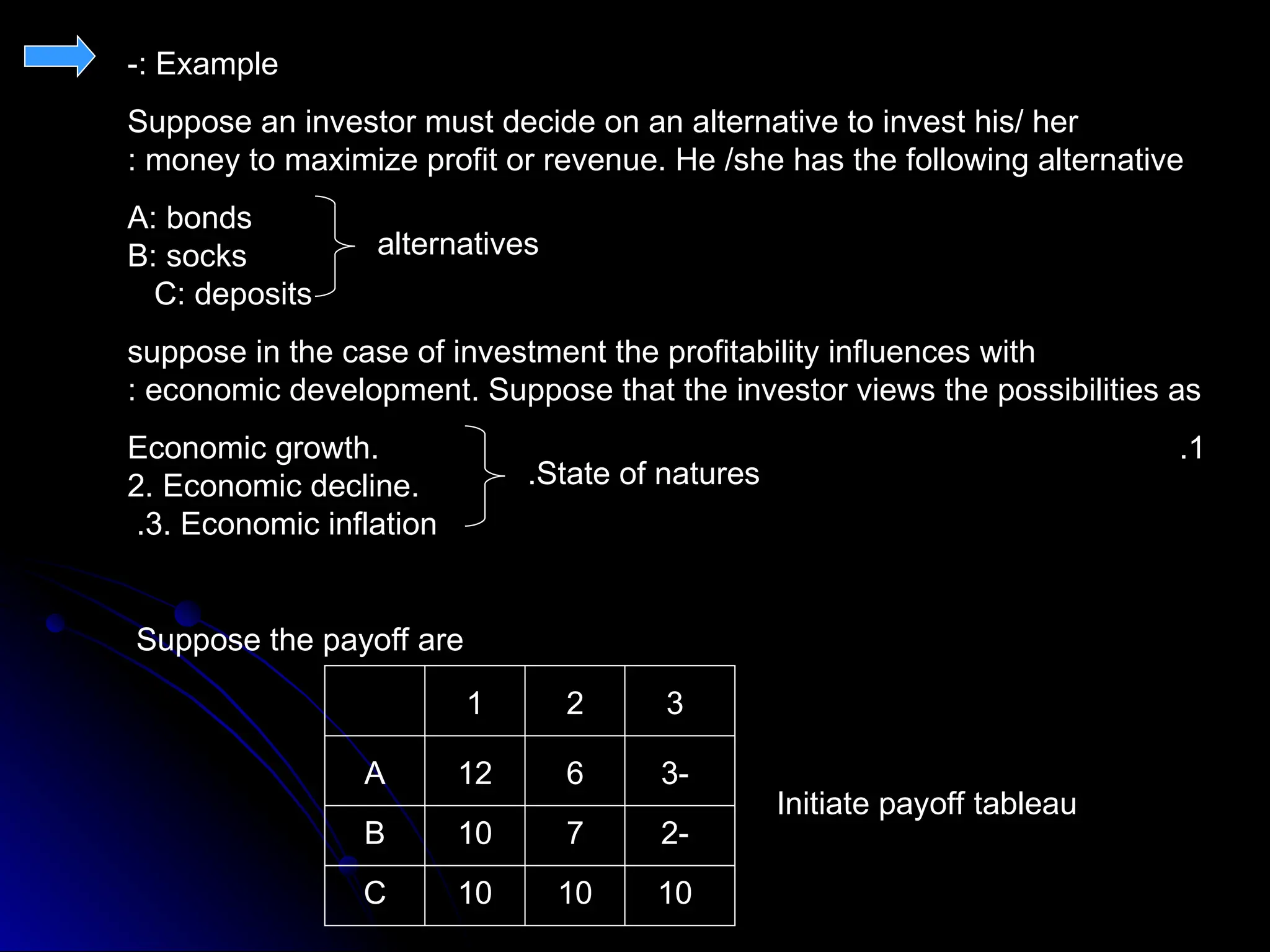

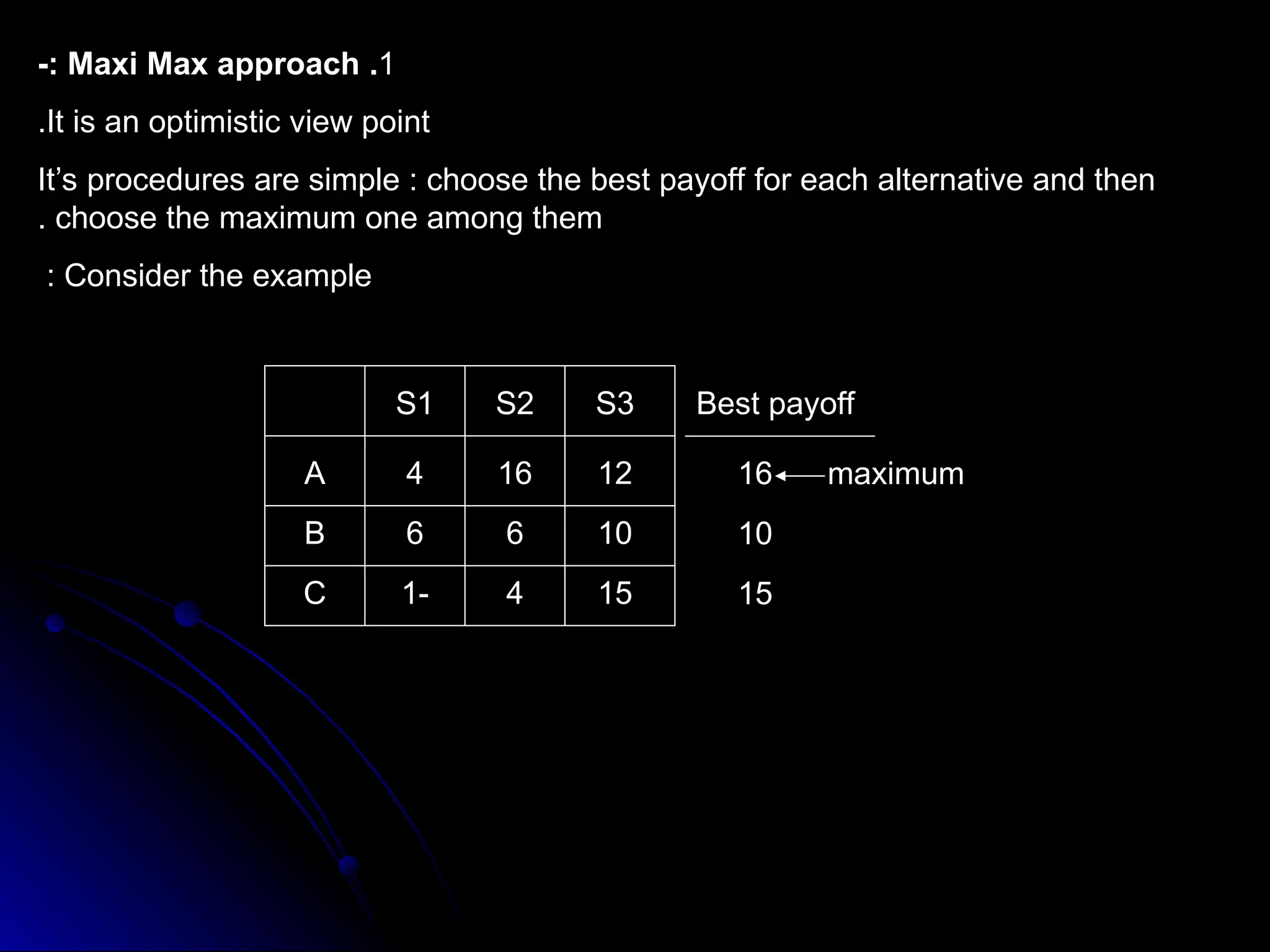

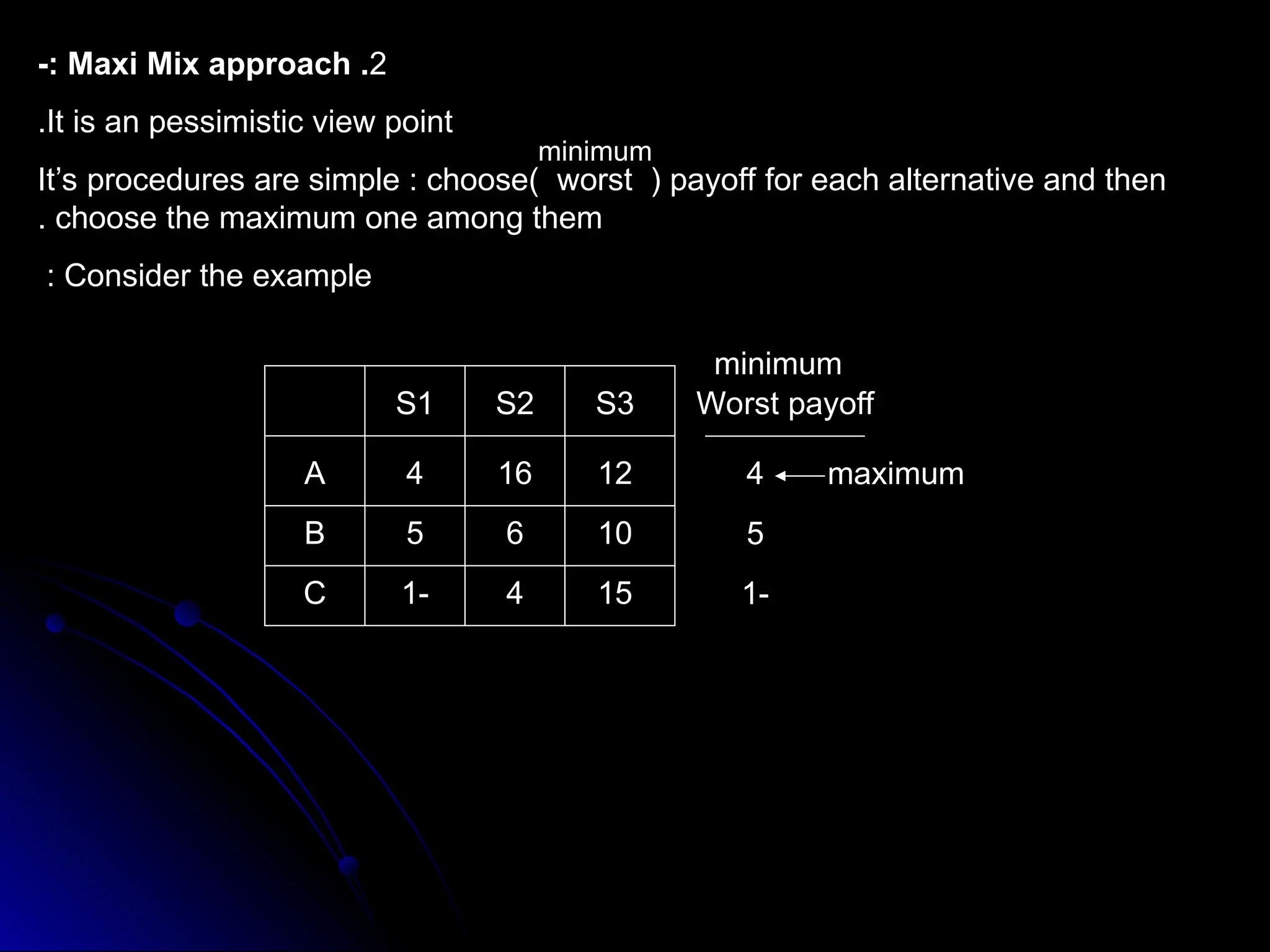

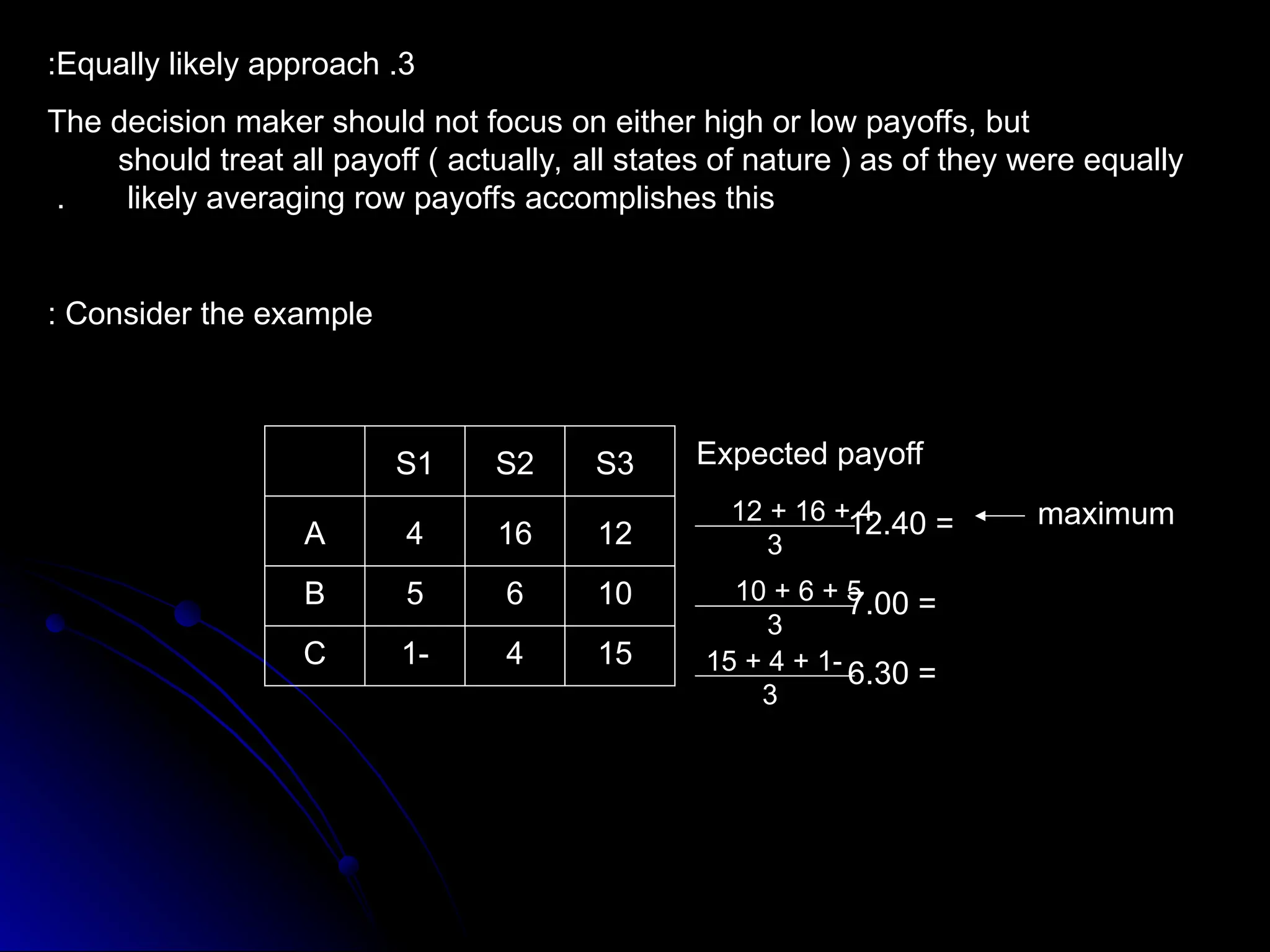

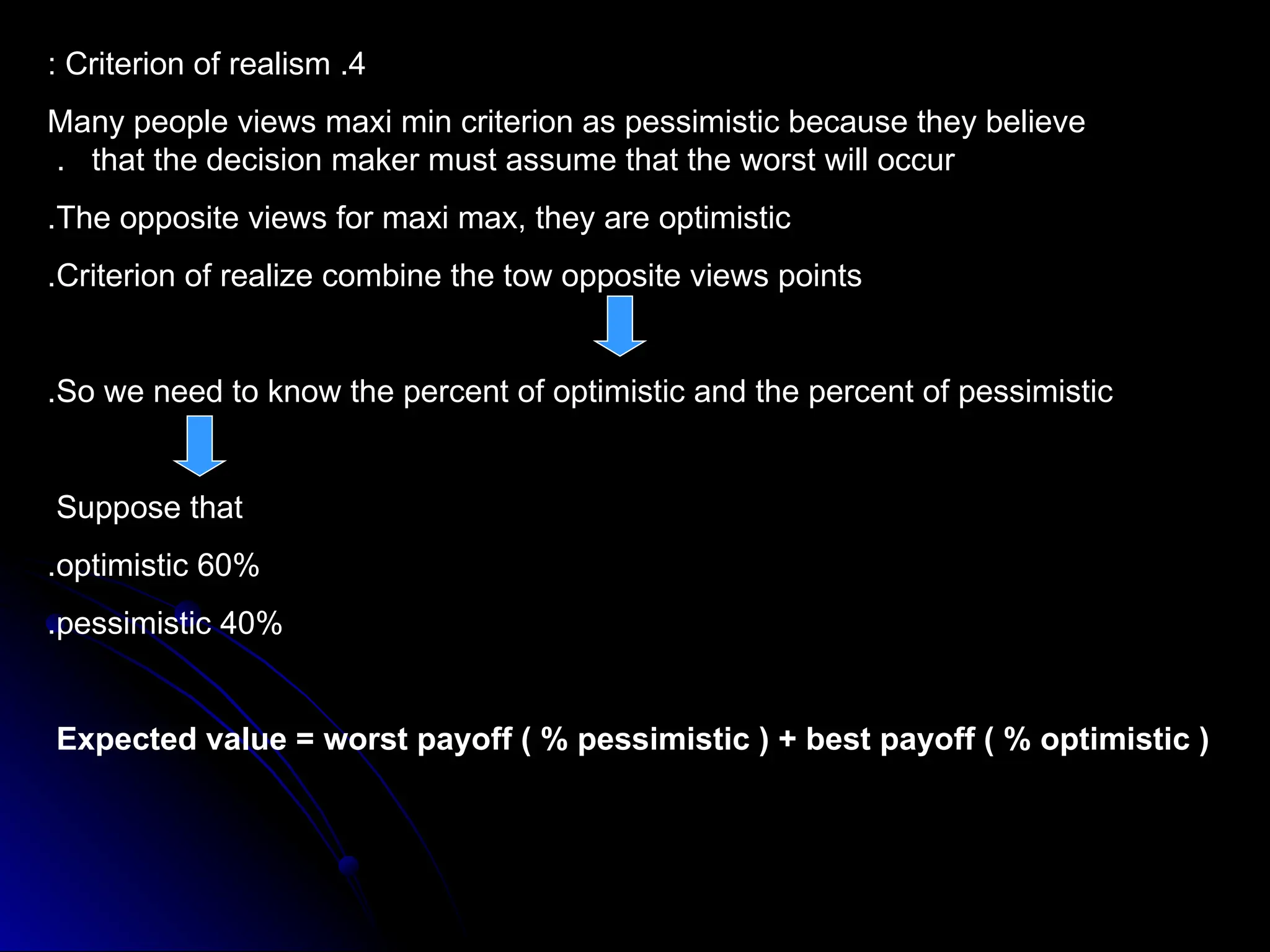

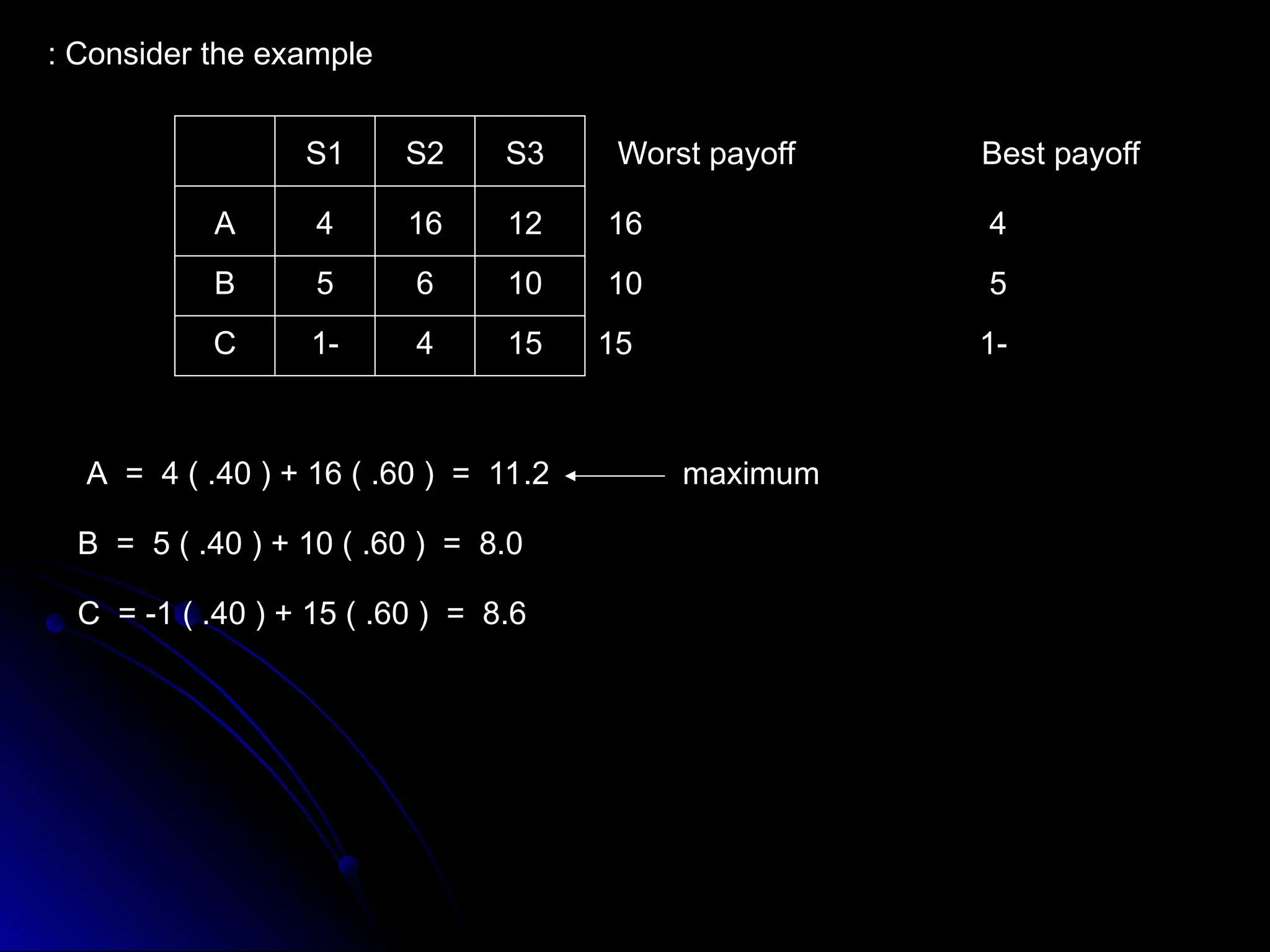

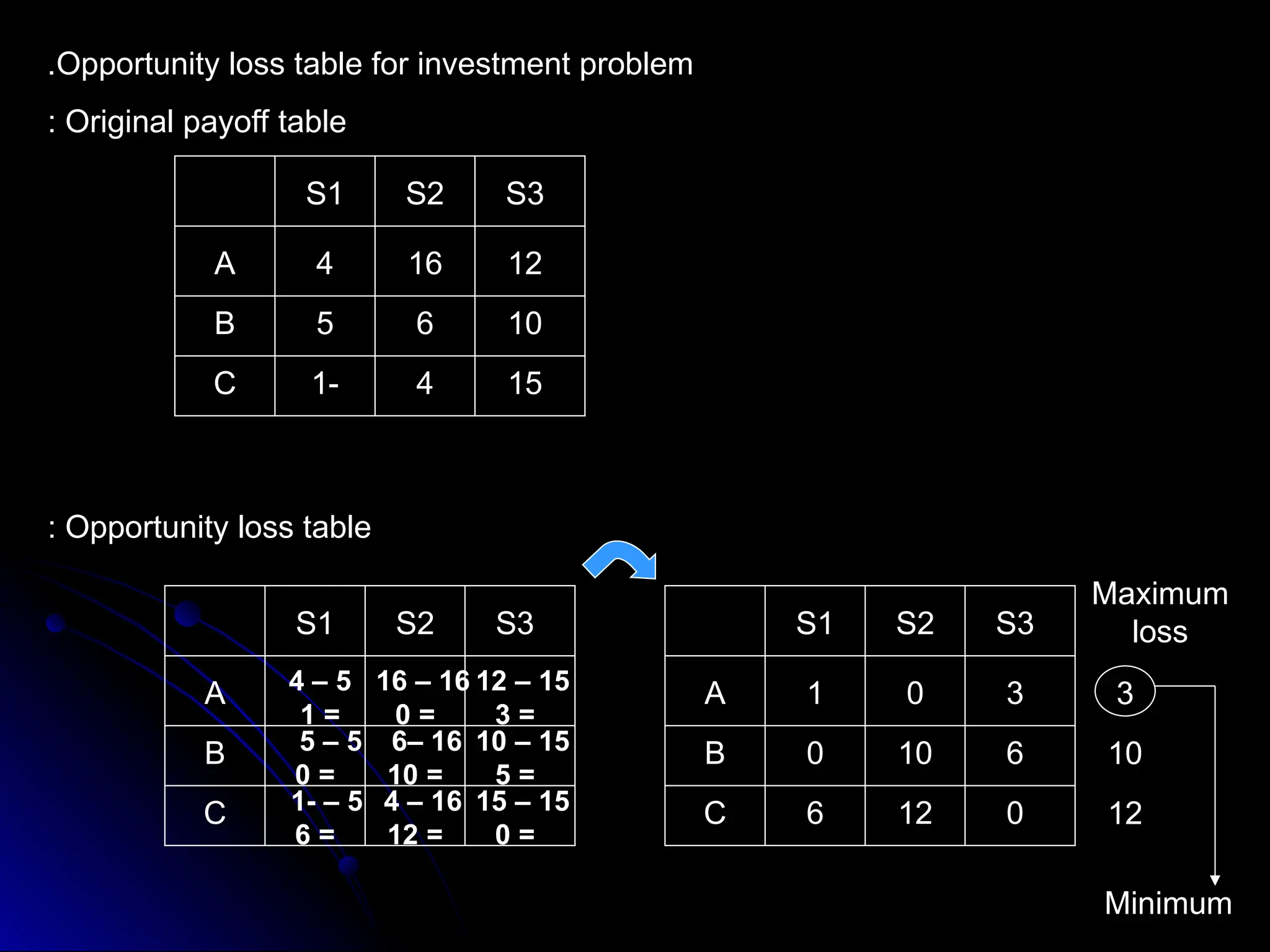

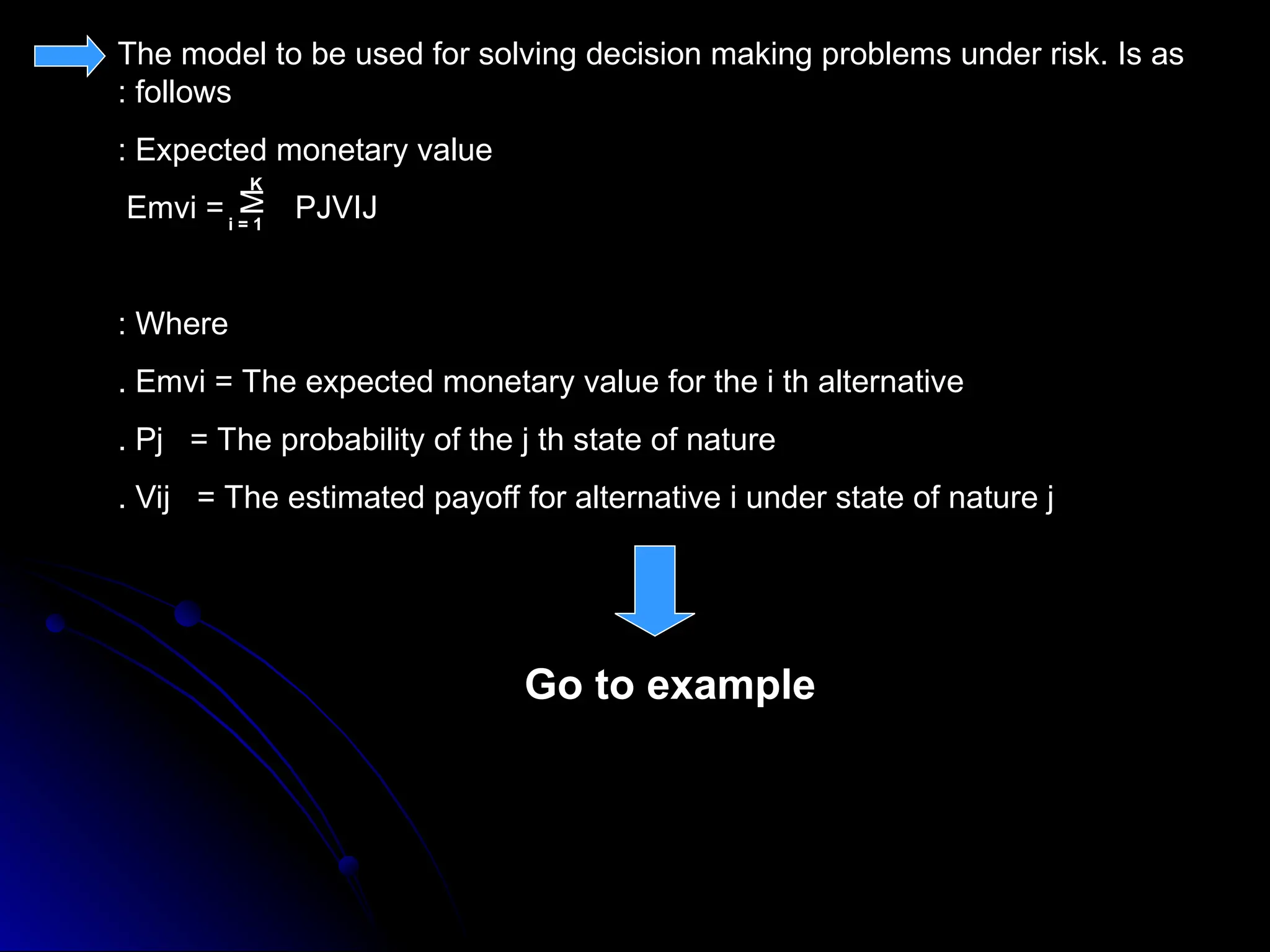

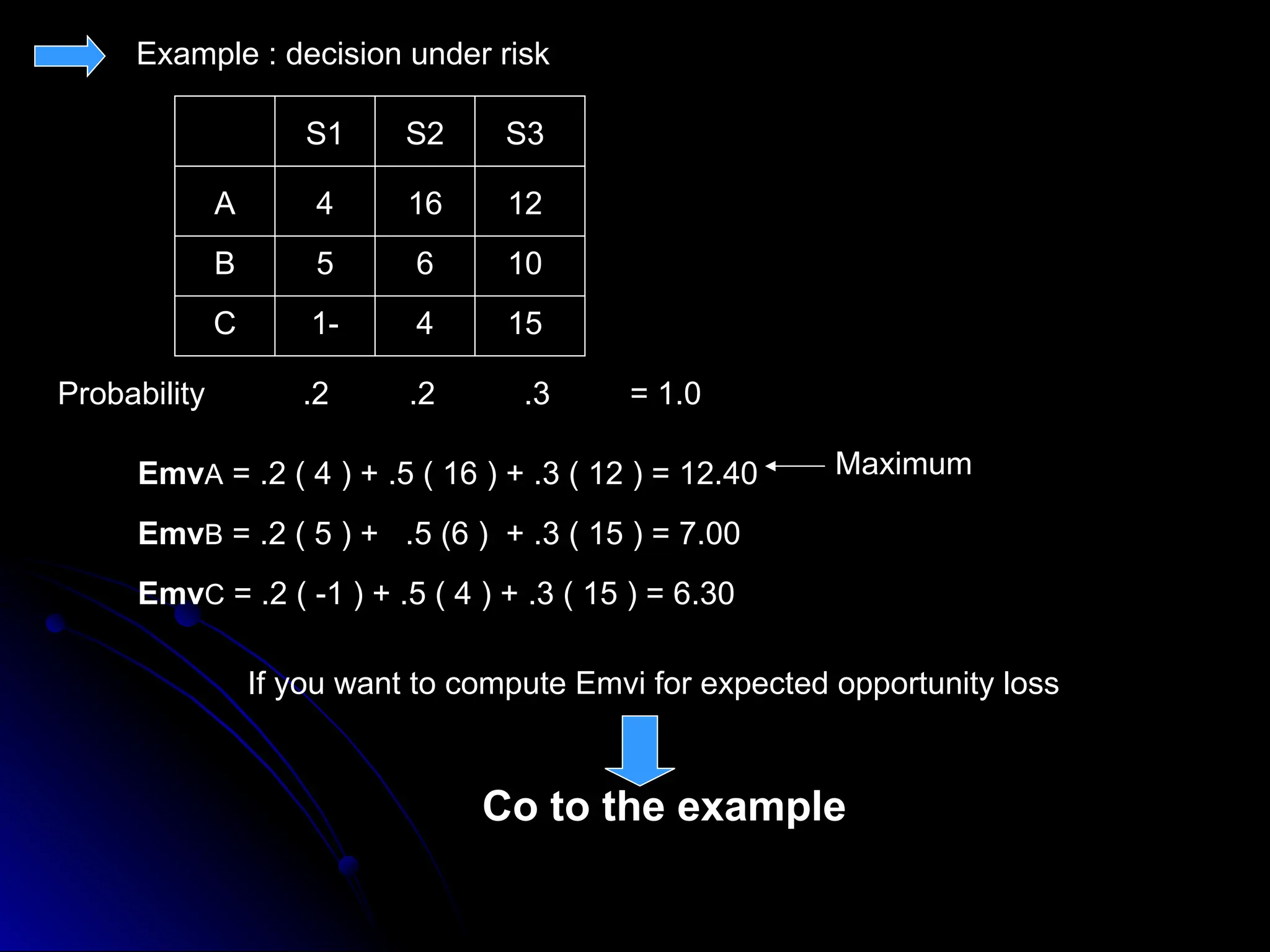

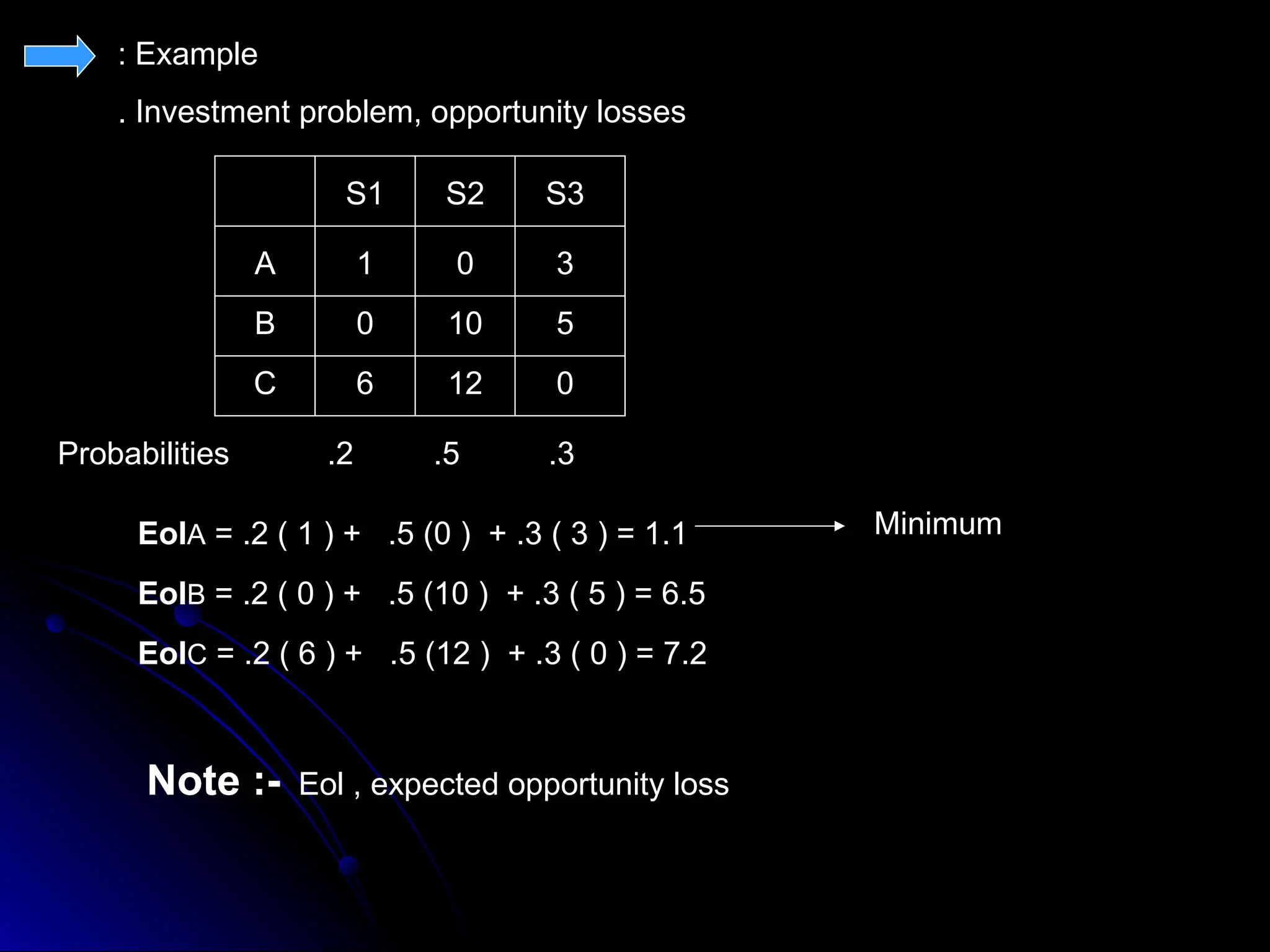

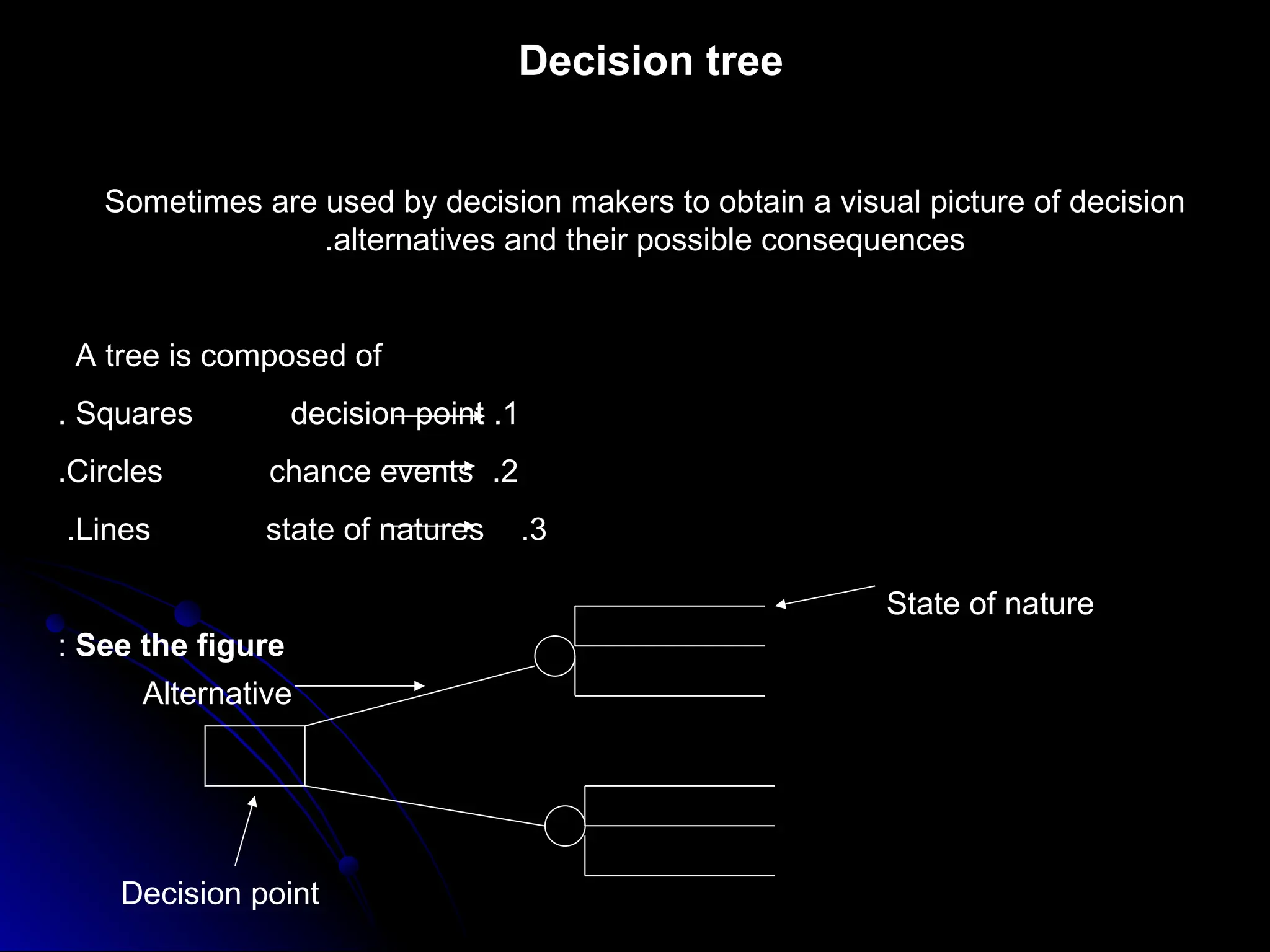

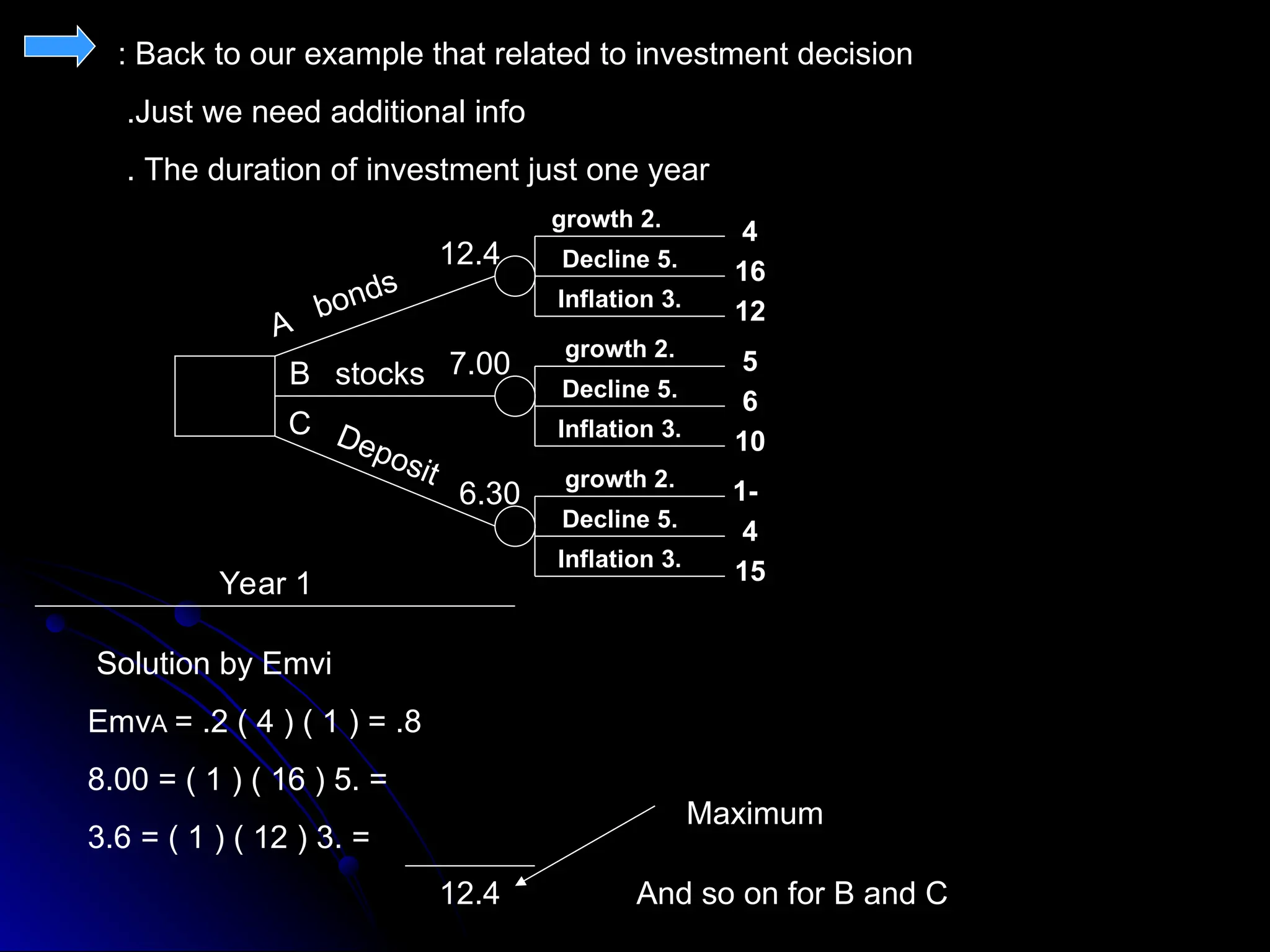

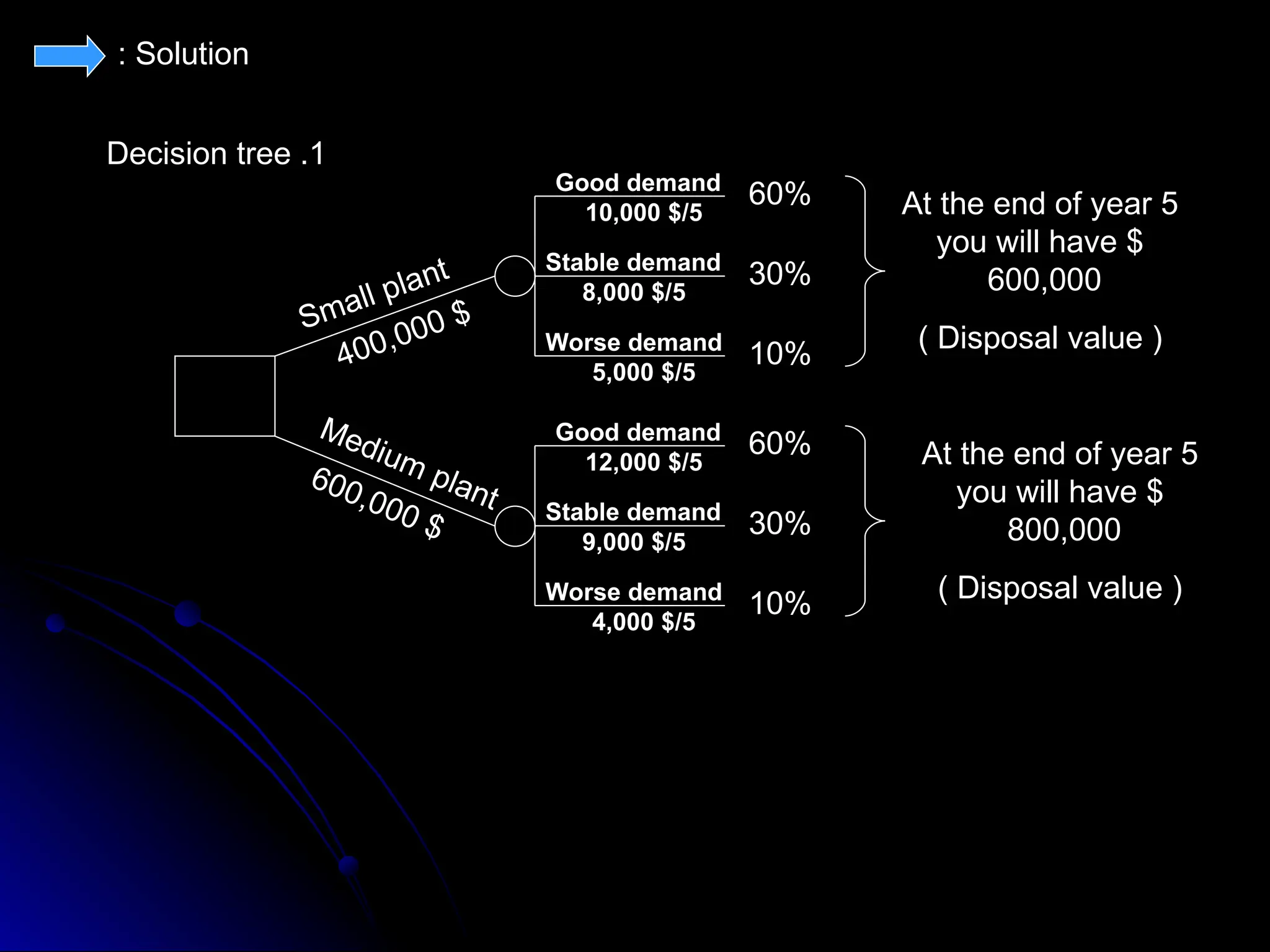

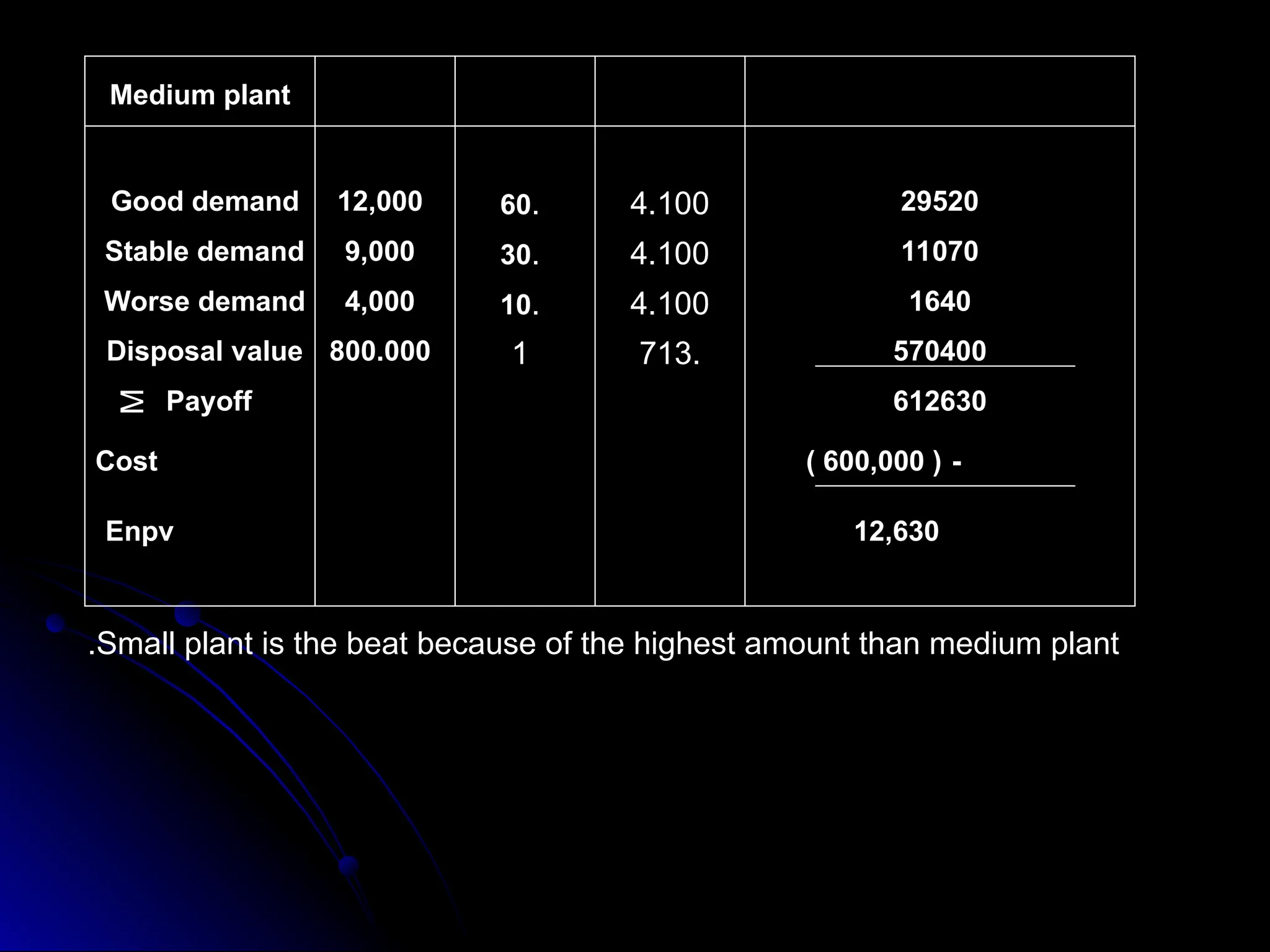

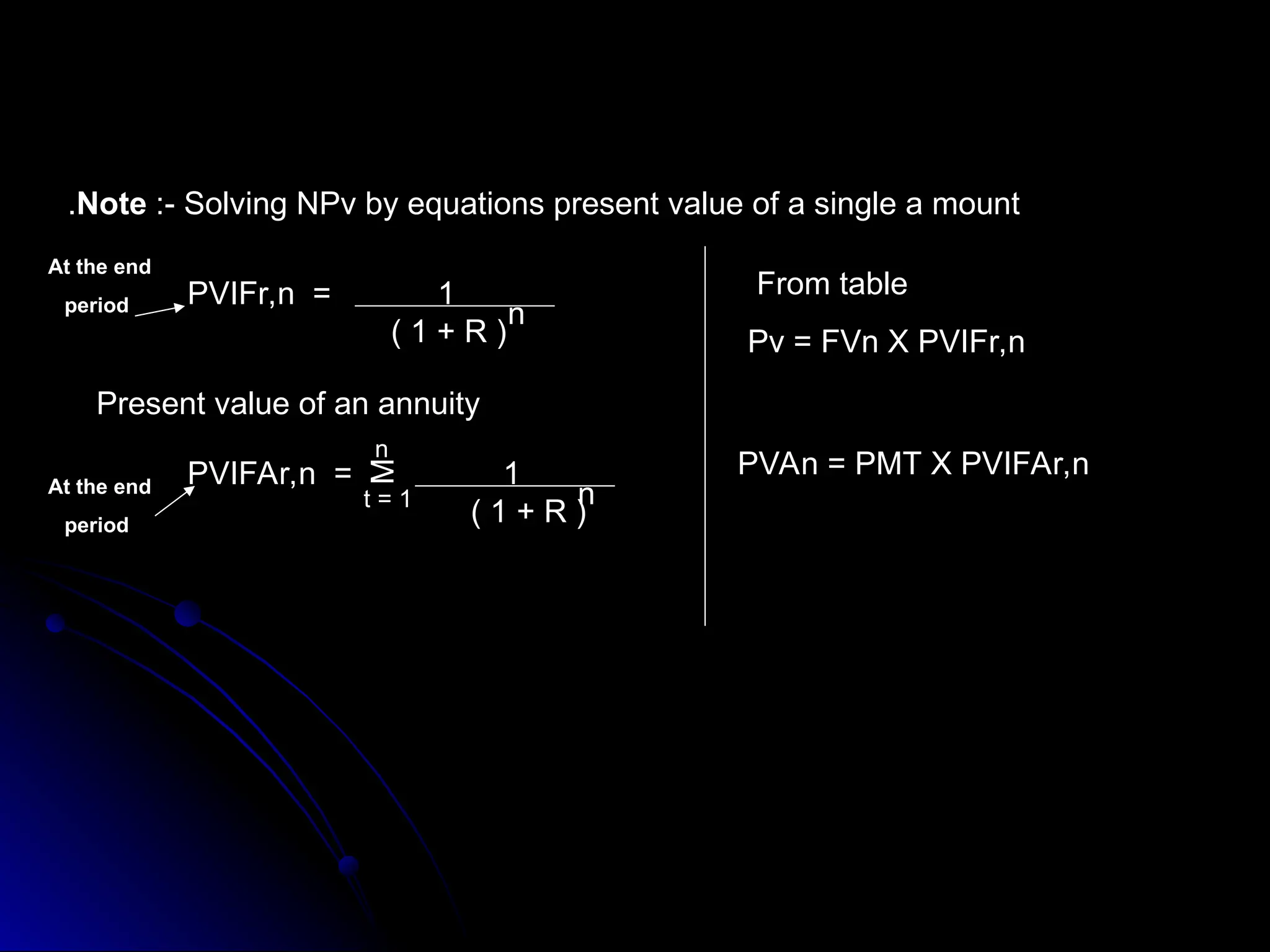

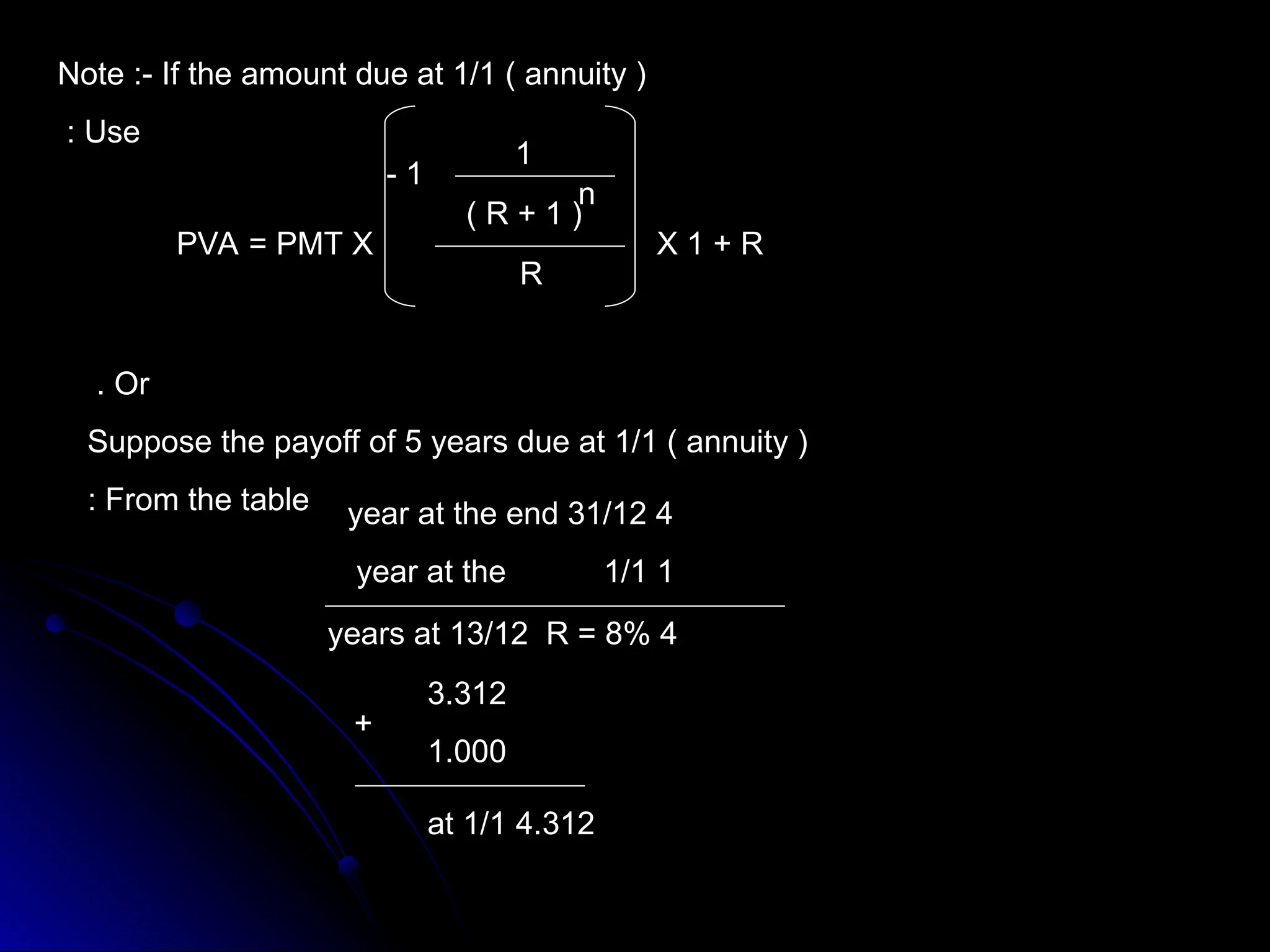

The document presents an overview of decision theory, emphasizing its applications in decision-making under certainty, risk, and uncertainty. It details constructing payoff tables and decision trees, describing the characteristics of different decision-making approaches like maxi max, maxi min, and the criterion of realism. Additionally, it incorporates practical examples to illustrate the application of these concepts in investment decisions.