|

THE 2016 VCFINTECH INVESTMENT

LANDSCAPE – SUMMARY (1 of 3)

5Source: Pitchbook (as at 30/01/17)

Lawrence Wintermeyer

CEO – Innovate Finance

China and the US dominate FinTech investment with a

combined $13.9 billion of the total $17.4 billion, 80% of the

global venture capital raised in 2016, and the top two ranked

future foreign investment sources for UK FinTech. Whilst UK

FinTech venture investment is down 33.7% in 2016 at $783

million, largely attributed to the uncertainty of Brexit and geo

political / macro economic factors, Q3 funding rebounded, and

9 of the top 20 deals completed in the 6 months following the

referendum, with the UK retaining its global ranking in third

place. The top three UK deals were Starling Bank (challenger

bank) at $101.0 million, iwoca (alternative finance) at $57.0

million and Nutmeg (robo advice) at $52.2 million

The loss of passporting rights will hit FinTech payments firms if

special provisions to the single market are not negotiated upon

leaving the union. However, maintaining and further improving

access to global FinTech talent has superseded passporting

across the FinTech community’s post-Brexit priorities. Over

30% of Innovate Finance FinTech founders and CxOs are non-

British with many employing European staff. Attracting further

investment to UK FinTech remains the number one priority

“

”

6.

|

THE 2016 VCFINTECH INVESTMENT

LANDSCAPE – SUMMARY (2 of 3)

6Source: Pitchbook (as at 30/01/17)

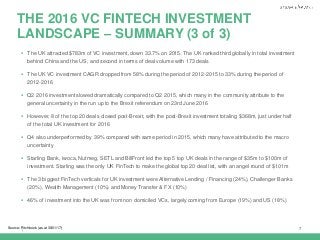

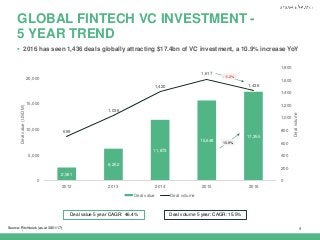

2016 saw 1,436 deals globally, attracting $17.4bn of VC investment, a 10.9% increase on 2015

China attracted the largest amount of VC investment at $7.7bn over 28 deals, an 84% increase on 2015

investment of $4.2bn, outpacing the US for the first time

US investment decreased in 2016 by 12.7% to $6.2bn despite being the global leader in deal volume at 650 deals

3 “mega-rounds”, each over $1bn, contributed to the significant increase in 2016 VC investment into China:

Alipay (Ant Financial) – $4.5bn (the biggest FinTech VC round in history)

Lufax.com – $1.2bn

JD Finance – $1.0bn

The most active global investor in 2016 was the seed fund and start up accelerator 500 Startups with 39

investments

Accelerators Startupbootcamp and Techstars were also amongst the most active global investors, with 36 and 30

investments respectively

There were no notable FinTech IPOs globally in 2016. The top global exit was the Markit’s (UK) $5.5bn merger

with IHS (US)

7.

|

THE 2016 VCFINTECH INVESTMENT

LANDSCAPE – SUMMARY (3 of 3)

7Source: Pitchbook (as at 30/01/17)

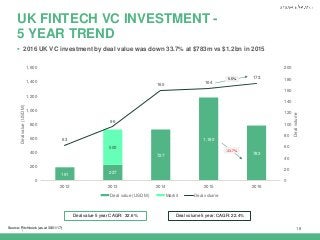

The UK attracted $783m of VC investment, down 33.7% on 2015. The UK ranked third globally in total investment

behind China and the US, and second in terms of deal volume with 173 deals

The UK VC investment CAGR dropped from 58% during the period of 2012-2015 to 33% during the period of

2012-2016

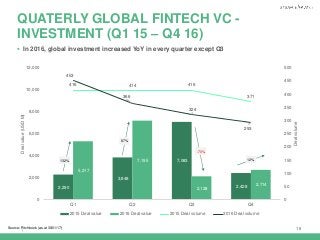

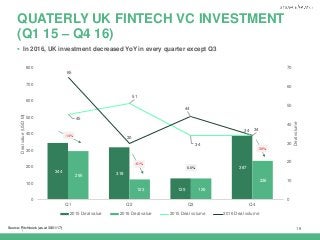

Q2 2016 investment slowed dramatically compared to Q2 2015, which many in the community attribute to the

general uncertainty in the run up to the Brexit referendum on 23rd June 2016

However, 8 of the top 20 deals closed post-Brexit, with the post-Brexit investment totaling $368m, just under half

of the total UK investment for 2016

Q4 also underperformed by 39% compared with same period in 2015, which many have attributed to the macro

uncertainty

Starling Bank, iwoca, Nutmeg, SETL and BillFront led the top 5 top UK deals in the range of $35m to $100m of

investment. Starling was the only UK FinTech to make the global top 20 deal list, with an angel round of $101m

The 3 biggest FinTech verticals for UK investment were Alternative Lending / Financing (24%), Challenger Banks

(20%), Wealth Management (10%) and Money Transfer & FX (10%)

46% of investment into the UK was from non domiciled VCs, largely coming from Europe (19%) and US (18%)

| 11

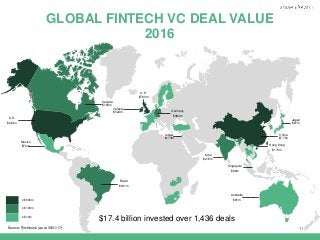

GLOBAL FINTECHVC DEAL VALUE

2016

U.S.

$6.2bn

Canada

$183m

Brazil

$161m

Australia

$91m

India

$272m

Japan

$87m

China

$7.7bn

Ireland

$524m

Hong Kong

$170m

Germany

$384m

U.K.

$783m

Israel

$173m

≥ $500m

≥ $100m

≥ $10m

$17.4 billion invested over 1,436 deals

Mexico

$72m

Singapore

$86m

Source: Pitchbook (as at 30/01/17)

12.

| 12

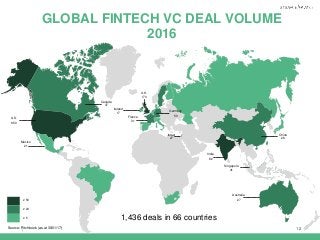

GLOBAL FINTECHVC DEAL VOLUME

2016

U.S.

650

Mexico

21

Canada

37

Australia

27

Singapore

41

India

82

China

28

Ireland

17

France

31

Germany

50

U.K.

173

Israel

27

≥ 50

≥ 20

≥ 5 1,436 deals in 66 countries

Source: Pitchbook (as at 30/01/17)

13.

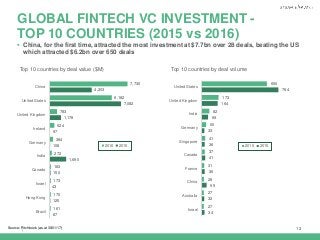

| 13

GLOBAL FINTECHVC INVESTMENT -

TOP 10 COUNTRIES (2015 vs 2016)

650

173

82

50

41

37

31

28

27

27

764

164

69

33

36

41

36

55

32

34

United States

United Kingdom

India

Germany

Singapore

Canada

France

China

Australia

Israel

2016 2015

7,730

6,182

783

524

384

272

183

173

170

161

4,203

7,082

1,178

97

108

1,690

150

43

125

87

China

United States

United Kingdom

Ireland

Germany

India

Canada

Israel

Hong Kong

Brazil

2016 2015

Top 10 countries by deal volumeTop 10 countries by deal value ($M)

China, for the first time, attracted the most investment at $7.7bn over 28 deals, beating the US

which attracted $6.2bn over 650 deals

Source: Pitchbook (as at 30/01/17)

14.

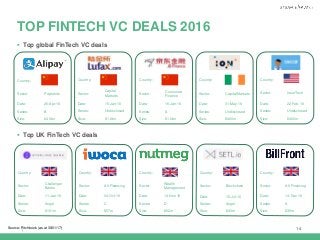

|

Country:

Sector:

Challenger

Banks

Date: 11-Jan-16

Series: Angel

Size:$101m

Country:

Sector: Alt Financing

Date: 04-Oct-16

Series: C

Size: $57m

Country:

Sector:

Wealth

Management

Date: 14-Nov-16

Series: D

Size: $52m

Country:

Sector: Blockchain

Date: 15-Jul-16

Series: Angel

Size: $40m

Country:

Sector: Alt Financing

Date: 14-Dec-16

Series: A

Size: $35m

Country:

Sector: Payments

Date: 26-Apr-16

Series: B

Size: $4.5bn

Country:

Sector: InsurTech

Date: 22-Feb-16

Series: Undisclosed

Size: $400m

Country:

Sector:

Capital

Markets

Date: 15-Jan-16

Series: Undisclosed

Size: $1.2bn

Country:

Sector:

Consumer

Finance

Date: 16-Jan-16

Series: A

Size: $1.0bn

Country:

Sector: Capital Markets

Date: 31-May-16

Series: Undisclosed

Size: $400m

Top UK FinTech VC deals

14

TOP FINTECH VC DEALS 2016

Top global FinTech VC deals

Source: Pitchbook (as at 30/01/17)

15.

|

4,500

1,200

1,013

400

400

394

237

220

212

180

165

153

150

150

115

103

103

101

100

100

100

100

AliPay (China)

Lu.com (China)

JDFinance (China)

ION Trading (Ireland)

Oscar (US)

51credit.com (China)

QuarterSpot (US)

Solar Mosaic (US)

PowerPlan (US)

Payoneer (US)

WeLab (Hong Kong)

Weidai.com (China)

Stripe (US)

LendUp (US)

PaySimple (US)

Zibby (US)

Kreditech (Germany)

Starling Bank (UK)

LendingHome (US)

DPO Group (Ireland)

Affirm (US)

Betterment (US)

Most active global investors by deal volume

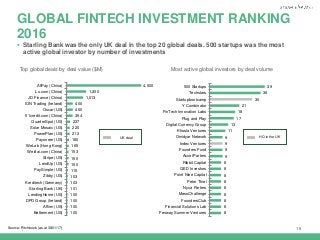

15

GLOBAL FINTECH INVESTMENT RANKING

2016

Top global deals by deal value ($M)

Starling Bank was the only UK deal in the top 20 global deals. 500 startups was the most

active global investor by number of investments

39

36

30

21

18

17

13

11

9

9

9

9

8

8

8

8

8

8

8

8

8

500 Startups

Techstars

Startupbootcamp

Y Combinator

FinTech Innovation Labs

Plug and Play

Digital Currency Group

Khosla Ventures

Omidyar Network

Index Ventures

Founders Fund

Accel Parters

Ribbit Capital

QED Investors

Point Nine Capital

Peter Thiel

Nyca Parters

MassChallenge

FoundersClub

Financial Solutions Lab

Fenway Summer Ventures

UK deal HQ in the UK

Source: Pitchbook (as at 30/01/17)

16.

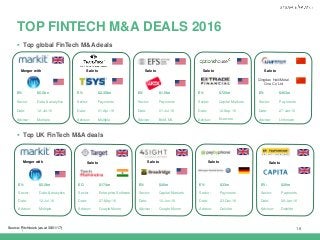

|

Top UKFinTech M&A deals

16

TOP FINTECH M&A DEALS 2016

Top global FinTech M&A deals

EV: $20m

Sector: Payments

Date: 08-Jan-16

Advisor: Deloitte

Sale toMerger with

EV: $5.5bn

Sector: Data & analytics

Date: 12-Jul-16

Advisor: Multiple

EC: $174m

Sector: Enterprise Software

Date: 27-May-16

Advisor: Quayle Munro

EV: $40m

Sector: Capital Markets

Date: 10-Jun-16

Advisor: Quayle Munro

EV: $33m

Sector: Payments

Date: 23-Dec-16

Advisor: Deloitte

Sale to Sale to Sale to

EV: $2.35bn

Sector: Payments

Date: 01-Apr-16

Advisor: Multiple

EV: $1.5bn

Sector: Payments

Date: 01-Jul-16

Advisor: BofA ML

EV: $725m

Sector: Capital Markets

Date: 12-Sep-16

Advisor: Evercore

EV: $463m

Sector: Payments

Date: 27-Jan-16

Advisor: Unknown

Sale to Sale to Sale to Sale to

Qingdao Haili Metal

One Co Ltd

Merger with

EV: $5.5bn

Sector: Data & analytics

Date: 12-Jul-16

Advisor: Multiple

Source: Pitchbook (as at 30/01/17)

|

Challenger

Banks,

20%

Money

Transfer &

FX, 10%

Digital

Currencies&

Blockchain,

6%

Crowdfunding,

6%

Alternative

Lending /

Financing,

29%

Payments,

6%

Enterprise

Software,

5%

Wealth

Management,

10%

Capital

Markets,

2%

RegTech,

3%

Financial

inclusion,

3% Cyber

security,

2%

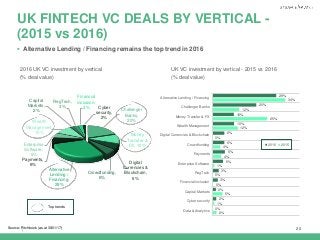

Alternative Lending / Financing remains the top trend in 2016

20

UK FINTECH VC DEALS BY VERTICAL -

(2015 vs 2016)

UK VC investment by vertical - 2015 vs 2016

(% deal value)

2016 UK VC investment by vertical

(% deal value)

Source: Pitchbook (as at 30/01/17)

Top trends

29%

20%

10%

10%

6%

6%

6%

5%

3%

3%

2%

2%

0%

34%

12%

25%

12%

0%

4%

4%

1%

0%

0%

5%

1%

2%

Alternative Lending / Financing

Challenger Banks

Money Transfer & FX

Wealth Management

Digital Currencies & Blockchain

Crowdfunding

Payments

Enterprise Software

RegTech

Financial inclusion

Capital Markets

Cyber security

Data & Analytics

2016 2015

21.

|

Most active UKinvestors by deal number

21

UK FINTECH INVESTMENT RANKING -

2016

Top UK deals by deal value ($M)

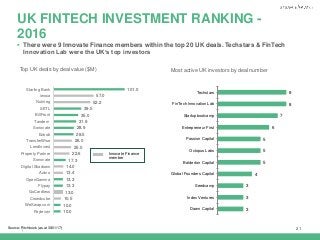

There were 9 Innovate Finance members within the top 20 UK deals. Techstars & FinTech

Innovation Lab were the UK’s top investors

101.0

57.0

52.2

39.5

35.0

31.9

28.9

28.5

26.0

25.0

22.6

17.3

14.0

13.4

13.3

13.3

13.0

10.5

10.0

10.0

Starling Bank

iwoca

Nutmeg

SETL

BillFront

Tandem

Sonovate

Ezbob

TransferWise

LendInvest

Property Partner

Sonovate

Digital Shadows

Azimo

OpenGamma

Flypay

GoCardless

Crowdcube

WeSwap.com

Payleven

8

8

7

6

5

5

5

4

3

3

3

Techstars

FinTech Innovation Lab

Startupbootcamp

Entrepreneur First

Passion Capital

Octopus Labs

Balderton Capital

Global Founders Capital

Seedcamp

Index Ventures

Dawn Capital

Innovate Finance

member

Source: Pitchbook (as at 30/01/17)

22.

|

10.0

39.5

10.5

57.0

13.3 13.3

17.3

52.2

35.0

22

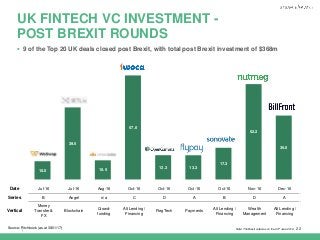

UK FINTECHVC INVESTMENT -

POST BREXIT ROUNDS

9 of the Top 20 UK deals closed post Brexit, with total post Brexit investment of $368m

Source: Pitchbook (as at 30/01/17) Note: The Brexit vote was on the 23rd June 2016

Date Jul-16 Jul-16 Aug-16 Oct-16 Oct-16 Oct-16 Oct-16 Nov-16 Dec-16

Series B Angel n/a C D A B D A

Vertical

Money

Transfer &

FX

Blockchain

Crowd-

funding

Alt Lending /

Financing

RegTech Payments

Alt Lending /

Financing

Wealth

Management

Alt Lending /

Financing

23.

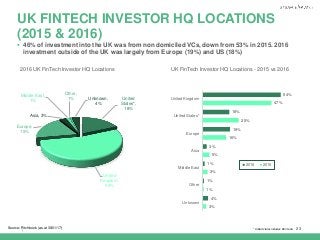

| 23

UK FINTECHINVESTOR HQ LOCATIONS

(2015 & 2016)

46% of investment into the UK was from non domiciled VCs, down from 53% in 2015. 2016

investment outside of the UK was largely from Europe (19%) and US (18%)

* United states includes BermudaSource: Pitchbook (as at 30/01/17)

United

States*,

18%

United

Kingdom,

54%

Europe,

19%

Asia, 3%

Middle East,

1%

Other,

1% Unknown,

4%

UK FinTech Investor HQ Locations - 2015 vs 20162016 UK FinTech Investor HQ Locations

54%

18%

19%

3%

1%

1%

4%

47%

25%

16%

5%

3%

1%

3%

United Kingdom

United States*

Europe

Asia

Middle East

Other

Unknown

2016 2015

24.

| 24

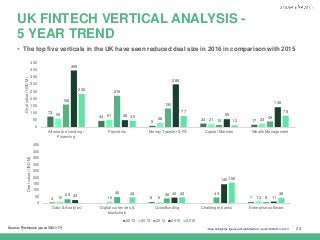

UK FINTECHVERTICAL ANALYSIS -

5 YEAR TREND

The top five verticals in the UK have seen reduced deal size in 2016 in comparison with 2015

73

44

9

24 17

59 51

28 21 23

158

219

130

15

39

395

48

298

55

138

230

45

77

12

78

0

50

100

150

200

250

300

350

400

450

Alternative Lending /

Financing

Payments Money Transfer & FX Capital Markets Wealth Management

Dealvalue(USDM)

4 8 710 10 6 13

29

46 36 43

823

42

145

11

43 43

158

38

0

50

100

150

200

250

300

350

400

450

Data & Analytics* Digital currencies &

blockchain

Crowdfunding Challenger banks Enterprise software

Dealvalue(USDM)

2012 2013 2014 2015 2016

Source: Pitchbook (as at 30/01/17) *Data & Analytics figures exclude Markit VC round of $500m in 2013

25.

| 25

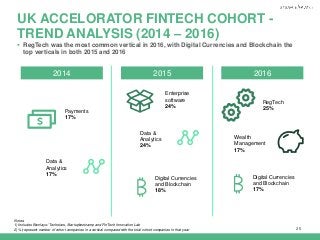

Notes:

1) IncludesBarclays / Techstars, Startupbootcamp and FinTech Innovation Lab

2) % represent number of cohort companies in a vertical compared with the total cohort companies in that year

UK ACCELORATOR FINTECH COHORT -

TREND ANALYSIS (2014 – 2016)

2014

RegTech

25%

Digital Currencies

and Blockchain

17%

Wealth

Management

17%

Enterprise

software

24%

Data &

Analytics

24%

Digital Currencies

and Blockchain

18%

Payments

17%

Data &

Analytics

17%

2015 2016

RegTech was the most common vertical in 2016, with Digital Currencies and Blockchain the

top verticals in both 2015 and 2016

26.

|

26

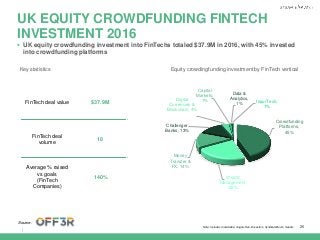

UK EQUITY CROWDFUNDINGFINTECH

INVESTMENT 2016

Equity crowdingfunding investment by FinTech verticalKey statistics

Note: Includes Crowdcube, Angels Den, Envestors, SyndicateRoom, Seedrs

Source:

UK equity crowdfunding investment into FinTechs totaled $37.9M in 2016, with 45% invested

into crowdfunding platforms

Crowdfunding

Platforms,

45%

Wealth

Management,

22%

Money

Transfer &

FX, 14%

Challenger

Banks, 13%

Digital

Currencies &

Blockchain, 4%

Capital

Markets,

1%

Data &

Analytics,

1% InsurTech,

1%

FinTech deal value $37.9M

FinTech deal

volume

18

Average % raised

vs goals

(FinTech

Companies)

140%

|

2016 GLOBAL VCFINTECH INVESTMENT

LANDSCAPE – ANALYST SUPPLEMENT

28Source: Pitchbook (as at 30/01/17)

Investors

The most active FinTech investor in 2016 was the seed fund and start up accelerator 500 Startups with 39

investments. In June 2016, 500 Startups announced it was raising a $25m FinTech fund to invest in ~100 early

stage companies globally

Accelerators Startupbootcamp (UK based) and Techstars (US based) were also amongst the most active global

investors, with 36 and 30 investments respectively. Startupbootcamp has FinTech accelerators in London,

Mumbai, New York and Singapore. Techstars has partnered with Barclays and has FinTech accelerators in New

York, London and in 2016 launched programs in Tel Aviv and Cape Town

Exits

In contrast to 2015, which saw two large FinTech IPOs (Square and Worldpay), 2016 did not see any notable

FinTech companies IPO, with several companies postponing them (e.g. SoFi, Elevate Credit Inc.)

2016 Exits were realised through M&A via trade or private equity. The largest exit was UK based data & analytics

company Markit’s merger with US based IHS for $5.5bn

FinTech M&A activity is likely to increase in 2017 as the number of mature FinTech companies in the market

increases

29.

|

2016 UK VCFINTECH INVESTMENT

LANDSCAPE – ANALYST SUPPLEMENT

29Source: Pitchbook (as at 30/01/17)

Investors

The top investors in the UK were Techstars and FinTech Innovation Labs – both US domiciled accelerators with

specific London FinTech cohorts

46% of investment into the UK was from investors not domiciled in the UK, the largest of these being Europe at

19% and the US at 18%. Within Europe, large amount of investment from France and Germany – other notable

FinTech hubs

UK accelerators

25% of the London FinTech accelerator cohorts in 2016 were RegTech companies, supporting the prediction that

RegTech will emerge as an important FinTech vertical in 2017

Blockchain is also a top vertical (17% of the cohorts in both 2015 & 2016), indicating that this technology is still

receiving investment and development attention on the path to wider industry application and adoption

Equity crowdfunding

Equity crowdfunding is performing not only as a strong and stable asset class in its own right, but also a growing

vertical in the alternative finance industry

$37.9m was raised by FinTechs across platforms in 2016, with crowdfunding platforms raising 45% of the total

FinTech investment through platforms. As the sector matures, we are more than likely to see other verticals

seeking to capitalise on this new fundraising method

30.

| 30

For thefull speaker list go to www.ifgs2017.com

Rajesh Agrawal

Deputy Mayor of

London for Business

Maria Gotsch

President and CEO of the

Partnership Fund for

New York City

Giles Andrews

Co-Founder & Executive

Chairman, Zopa

Ian Dyson

Commisoner

City of London Police

Steel Mohnot

Partner, 500 Startups

Brett King

CEO of Moven and Host of

Breaking Banks

Jens Spahn

Parliamentary State

Secretary Federal Ministry

of Finance, Germany

2000+ ATTENDEES

300+ FINTECHS

100+ SPEAKERS

Platinum Sponsor Lead Media Partner

10th

- 11th

April 2017

Guildhall, London

Tickets available now at £795

Poppy Gustafsson

CEO (EMEA),

Darktrace

|

32

APPENDIX I: VERTICALDEFINITIONS

Alternative Lending / Financing – P2P lending, invoice financing, SME financing, e-lending platforms, credit

scoring

Capital Markets – innovation relating to primary issuance, securities trading, M&A, trade and advisory services

in a B2B

Challenger Banks – new digital banks that are challenging the large established High Street banks

Crowdfunding – platforms that allow investment for projects / companies / property

Cyber Security - technology designed to protect companies infrastructure from attack, damage or

unauthorised access

Data & Analytics – analysis of data within the financial industry to support data driven decisions

Digital Currencies & Blockchain – digital ledger technology, in which transactions made in bitcoin or digital

currency are recorded chronologically and publicly

Enterprise Software – software solutions for financial service industry

Financial Inclusion – delivery of financial services to the unbanked / unbankable

InsurTech – technology applied to the insurance industry

Money Transfer & FX – money transfer, international remittance & currency conversion

Payments – innovation in payments, including cashless, online / ecommerce, mobile, B2B, merchant / POS,

wallets, P2P, recurring

RegTech – technology applied to resolve issues regarding regulation within the financial industry

Wealth Management – innovation within pensions, savings, personal financial management, investment

platforms and management of personal assets and investments (e.g. robo-advisors)

33.

|

33

APPENDIX II: METHODOLOGY

VC deal value figures include the deal types:

- Angel

- Accelerator / incubator

- Crowdfunding

- VC (all rounds)

- Private Equity (Growth/Expansion rounds only)

VC deal value figures include all deals completed or announced (verified to press releases) in 2016

Deal volume figures include deals without a disclosed deal value

UK VC deal value represents investment into FinTech companies which are Head Quartered in the UK