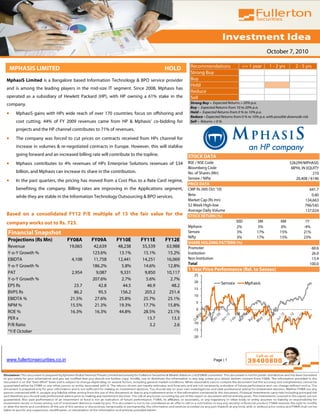

1. October 7, 2010

Recommendations <= 1 year 1 - 2 yrs 2 - 5 yrs

MPHASIS LIMITED HOLD

Strong Buy

MphasiS Limited is a Bangalore based Information Technology & BPO service provider Buy

Hold

and is among the leading players in the mid-size IT segment. Since 2008, Mphasis has

Reduce

operated as a subsidiary of Hewlett Packard (HP), with HP owning a 61% stake in the Sell

company. Strong Buy – Expected Returns > 20% p.a.

Buy – Expected Returns from 10 to 20% p.a.

• MphasiS gains with HPs wide reach of over 170 countries; focus on offshoring and Hold – Expected Returns from 0 % to 10% p.a.

Reduce – Expected Returns from 0 % to 10% p.a. with possible downside risk

cost cutting. 44% of FY 2009 revenues came from HP & Mphasis’ co-bidding for Sell – Returns < 0 %

projects and the HP channel contributes to 71% of revenues.

• The company was forced to cut prices on contracts received from HPs channel for

increase in volumes & re-negotiated contracts in Europe. However, this will stablise

going forward and an increased billing rate will contribute to the topline. STOCK DATA

• Mphasis contributes to 4% revenues of HPs Enterprise Solutions revenues of $34 BSE / NSE Code 526299/MPHASIS

Bloomberg Code MPHL IN EQUITY

billion, and Mphasis can increase its share in the contribution. No. of Shares (Mn) 210

Sensex / Nifty

• In the past quarters, the pricing has moved from a Cost Plus to a Rate Card regime, 20,408 / 6146

PRICE DATA

benefiting the company. Billing rates are improving in the Applications segment, CMP Rs (6th Oct '10) 641.7

while they are stable in the Information Technology Outsourcing & BPO services. Beta 0.60

Market Cap (Rs mn) 134,663

52 Week High-low 796/545

Average Daily Volume 137,024

Based on a consolidated FY12 P/E multiple of 15 the fair value for the STOCK RETURN (%)

company works out to Rs. 723. 30D 3M 6M 1Y

Mphasis 2% 5% 0% -4%

Financial Snapshot Sensex 3% 17% 15% 21%

Nifty 3% 17% 15% 23%

Projections (Rs Mn) FY08A FY09A FY10E FY11E FY12E

SHARE HOLDING PATTERN (%)

Revenue 19,065 42,639 48,238 55,539 63,988 Promoter 60.6

Y-o-Y Growth % 123.6% 13.1% 15.1% 15.2% Institution 26.0

EBIDTA 4,108 11,758 12,441 14,251 16,069 Non Institution 13.4

Total 100.0

Y-o-Y Growth % 186.2% 5.8% 14.6% 12.8%

1 Year Price Performance (Rel. to Sensex)

PAT 2,954 9,087 9,331 9,850 10,117

25

Y-o-Y Growth % 207.6% 2.7% 5.6% 2.7%

20 Sensex Mphasis

EPS Rs 23.7 42.8 44.5 46.9 48.2

15

BVPS Rs 86.2 95.5 156.2 203.2 251.4

10

EBIDTA % 21.5% 27.6% 25.8% 25.7% 25.1%

5

NPM % 15.5% 21.3% 19.3% 17.7% 15.8%

0

ROE % 16.3% 16.3% 44.8% 28.5% 23.1%

-5

PER x 13.7 13.3

-10

P/B Ratio 3.2 2.6

*Y/E October -15

-20

www.fullertonsecurities.co.in Page | 1

2. October 7, 2010

BUSINESS PROFILE

MphasiS is India’s fifth largest Information Technology Company and is present in the BFSI, Telecom, Manufacturing,

Airlines, Transport, Retail & Healthcare industries. In 2006, Mphasis was a subsidiary of Electronic Data Systems (EDS), which

was bought out by HP in 2008. Since then, MphasiS has been a subsidiary of HP, with HP owning a 61% stake.

MphasiS is looking to

MphasiS employs over 38,000 people across its delivery centers globally and has a client base of 170 at the end of FY09. The

acquire small

company operates in three segments, Application Services (Apps), Infrastructure Technology Outsourcing (ITO) and Business companies and scale up

Process Outsourcing (BPO). The Apps business consists of building customized softwares to client requirements & their business.

contributed to 64% of revenues in FY 2009. The ITO business contributes to 17.5% of revenues and consists of end-to-end

services for workplace management, mainframe and web hosting services and datas center services. The BPO segment for

the same period contributed to 18.5% of revenues and consists of Voice & Non-Voice Data Processing services. On a

Geographical basis, the US contributed to 67% of revenues, Europe chipped in with 20%, and Asia Pacific & Middle East

contributed 6% and 7% respectively.

The company acquired AIG Systems Solutions (now MphasiS Solutions) in October 2009, strengthening its foray in the

Insurance Sector. MphasiS also acquired Fortify in April 2010, which specializes in the Remote Operations Management

(ROM) space. The ROM market globally is about $12 billion globally. MphasiS paid $15.5 million and 26 clients were added.

The deal is expected to increase margins, as Mphasis boosts the scale of Fortify.

Revenue Composition as of October 2009 Geographical Segmentation as of October 2009

Manufacturing Healthcare Logistics & Europe India & Middle East

& Retail 7% Transport 20% 7%

13% Telecom 5%

11%

Asia Pacific

6%

Technology &

OEMs

23% US

BFSI 67%

41%

HP parentage, Volume growth, Cash reserves to benefit; but geographical concentration is a concern

The company now generates 71% of revenues through the HP channel, with 44% of all revenues coming from co-bidding of

Mphasis has a net cash

projects. HP has been shifting more work offshore with lower pricing in return for higher volumes. With Cash balance of Rs balance of nearly Rs.

1487 crores at the end of July 2010, the company actively looking at acquisitions to boost growth. 15bn

The company generates 67% of revenues in the US & 20% in Europe, which makes the company highly vulnerable to Exchange

Rate movements. Mphasis has increased focus on India to mitigate the risk, but this will take time to materialize. Also, the

company is bearish on Europe where negotiations on pricing continue.

www.fullertonsecurities.co.in Page | 2

3. October 7, 2010

BUSINESS PERFORMANCE

Strong Revenue Growth ahead….

For the quarter ended July 2010, Mphasis added 22 clients and 63 since October 2009, taking the total client base to

233. Most of these new additions came through HP. Stability in rates and

For the Quarter ended July 2010, healthy volume growth, an uptick in ITO pricing and the acquisition of Fortify improving business

outlook will improve

helped the revenues to rise by 4.8% on a QoQ basis. EBIDTA was lower by 240 bps on a QoQ basis and 120 bps on a margins.

YoY basis on account of lower pricing and not because of higher wage expenses. Net Profit for the same period

ended higher by 1.5% because of Tax benefits and onetime gains. However, with change from Cost Plus to Rate

Card Model and improving business outlook, prospects for the company improve.

Revenue, Operating & PAT Margin Quarterly Performance

70,000 25% 14000

60,000 12000 28%

20%

Revenues (Rs mn)

50,000 10000

27%

Margins(%)

40,000 15% 8000

6000 26%

30,000 10%

4000

20,000 25%

5% 2000

10,000

0 24%

- 0%

FY08 FY09 FY10E FY11E FY12E

Revenue (Rs Mn) EBIDTA Margin PAT Margin Net Revenue (Rs mn) EBITDA Margins

Peer Group Comparison

Revenue EBIDTA PAT P/E P/B CMP FV

Companies ROE (%)

(Rs. mn) Margin (%) Margin (%) (x) (x) (Rs.) (Rs.)

Mphasis 42,639 28% 21% 45% 15.0 6.7 642 10

Oracle 22,435 35% 29% 16% 28.4 4.5 2238 5

HCL Tech 102,294 20% 13% 25% 23.4 5.9 433 10

*FY09 consolidated figures for Mphasis & HCL Technologies, FY10 for Oracle & HCL Tech

Peer Comparison

Mphasis’ margins lie between that of Oracle & HCL Technologies, because of Oracle’s Niche focus & parentage. HCLs Mphasis has a higher

RoE compared to its

strategy has been of being a volume player. However, Mphasis has been facing pricing pressures from HP & a high

peers.

geographical and revenue concentration compared to its peers, giving it a lower Earnings Multiple. Going forward,

profitability will improve as pricing pressure eases.

www.fullertonsecurities.co.in Page | 3

4. October 7, 2010

VALUATION

We estimate Mphasis Software’s revenues to grow at a CAGR of 14.5% over FY2009-12 to Rs 63.98bn by

Based on a consolidated

FY2012. We further estimate that PAT would grow at a CAGR of 3.6% over FY2009-12 to Rs 10.11bn in FY12 P/E multiple of 15, the

FY2012 from Rs 9.08bn in FY2009. fair value for the company

works out to Rs 723.

Based on a consolidated FY12 P/E multiple of 15, the fair value for the company works out

to Rs 723.

We recommend a ‘HOLD’ rating on the stock.

Financial Analysis and Projections

Particulars (Rs Mn) FY08A FY09A FY10E FY11E FY12E

Net Revenue 19,065 42,639 48,238 55,539 63,988

Other Income 218 562 569 576 583

Total Income 19,283 43,201 48,807 56,115 64,571

Operating Expenditure 15,175 31,443 36,366 41,863 48,502

Depreciation 1,005 2,022 1,948 2,231 2,572

EBIT 3,103 9,736 10,493 12,021 13,497

EBIT Margin (%) 16.3% 22.8% 21.8% 21.6% 21.1%

Interest 6 8 8 8 8

Profit Before Tax 3,097 9,728 10,485 12,012 13,489

Less: Tax 143 641 1,153 2,162 3,372

Profit After Tax 2,954 9,087 9,331 9,850 10,117

PAT Margin (%) 15.5% 21.3% 19.3% 17.7% 15.8%

ROE (%) 16.3% 16.3% 44.8% 28.5% 23.1%

EPS (Rs) 23.7 42.8 44.5 46.9 48.2

BVPS (Rs) 86.2 95.5 156.2 203.2 251.4

*Y/E October

Valuation Ratios (x) FY11E FY12E

P/E 13.7 13.3

P/B 3.2 2.6

www.fullertonsecurities.co.in Page | 4

5. October 7, 2010

Board of Directors

Director Name Current Position Description

Dr. Friedrich Froeschl is Non-Executive Chairman of the Board of Mphasis Ltd. He joined the Board of MphasiS in March

2009. Dr. Froeschl is a Physicist with PhD and an executive MBA. He currently heads Hi Tec Invest GmBH & Co. which is a

private equity management and consulting company with focus on information and communication technology

Non-Executive

Friedrich Froeschl industries. Dr. Froeschl was CEO of Computer Sciences Corporation, a global player in IT, Outsourcing and Consulting

Chairman

based in Germany. Before that, he held positions as Vice President and Business Head at Digital Equipment Corporation

and Messerschmitt-Bölkow-Blohm (today EADS) respectively. Throughout his career, Dr. Froeschl has been actively

involved in both larger multi-billion dollar deals as well as mid-size M&A projects.

Mr. Balu Ganesh Ayyar is the Chief Executive Officer, Executive Director of Mphasis Ltd. He joined MphasiS as the CEO in

January 2009. Ganesh is responsible for the overall management of the Company.Ganesh joins MphasiS from HP where his

CEO, Executive

Balu Ayyar last assignment was that of Vice President, Managed Services, Asia Pacific & Japan selective sourcing and small and

Director

medium outsourcing deals. His experience across a portfolio of functions and geographies brings a global perspective to

MphasiS. Born in India, Ganesh is a Chartered Accountant from the Institute of Chartered Accountants of India.

Serafini is executive Vice President of Emerging Markets at HP. In this role, he heads strategy, planning, coordination and

growth initiatives across Emerging Markets globally. From 2005 until April 2010, Serafini served as Managing Director for

Vice Chairman of the HP Europe, the Middle East and Africa (EMEA) and as Senior Vice President for the Enterprise Business in EMEA. He chaired

Serafini Francesco

Board the regional leadership team, and was responsible for the company’s strategy in EMEA, developing partnerships and key

stakeholder relations for HP. Serafini joined HP in 1981 and held several senior management positions. Serafini holds an

engineering degree in electronics from Politecnico of Turin.

Nawshir Mirza is a Fellow of the Institute of Chartered Accountants of India having qualified in the year 1973. He spent

most of his career with Ernst & Young and its Indian member firm, S.R.Batliboi & Co., Chartered Accountants, and its

Nawshir H Mirza Director predecessor firm, Arthur Young, being a partner from 1974 to 2003. He joined the Board of MphasiS in January 2004. He

has contributed to the accounting profession, being a speaker or the chairperson at a large number of professional

conferences in India and abroad.

D S Brar is a B.E. (Electrical) from Thapar Institute of Engineering & Technology, Patiala, and a Masters in Management from

Faculty of Management Studies, University of Delhi (Gold Medalist - 1974). He joined the Board in April 2004. Brar started

Davinder Singh Brar Director his career with Associated Cement Companies (ACC) and later joined Ranbaxy Laboratories Limited where he rose to the

position of CEO and Managing Director. He is also a Member of the Board of Governors in Indian Institute of Management,

Lucknow and Special Advisor to the Board of Directors of Codexis, a California based Company.

Prakash Jothee joined the Board of MphasiS in February 2009. At HP, he is vice president in the Office of Strategy and

Technology. Jothee is responsible for leading all major high-value strategic HP initiatives and leads all major HP Enterprise

Services transformation efforts. Before joining HP in 2005, Jothee was a principal in A.T. Kearney's Communications and

Prakash Jothee Director

High Tech practice, focusing on client projects in the corporate strategy and M&A, marketing, and sales strategy arenas.

Prakash Jothee has a Bachelor's degree in Physics and Chemistry and a graduate degree in management from Stanford

University.

Balu Doraisamy joined the Board of MphasiS on July 15, 2010. Balu has more than 25 years of experience with HP

(including acquisitions). Balu is currently the Senior Vice President of HP’s Enterprise Business in Asia Pacific and Japan

Balu Doraisamy Director

(APJ). Prior to his regional roles, Balu served as the Managing Director of HP India, having joined HP from Compaq. Balu

holds a post graduate degree in Computer Science and a Master’s degree in Mathematics.

Juergen Reiners, joined the Board of MphasiS on July 15, 2010. Reiners is Vice president of HP’s Global Business Services,

and is responsible for developing the company’s shared services strategy and global operating model. His current scope of

functions includes Finance and Accounting, Human Resources, Supply Chain, Service Administration and Marketing

Support. In his current role, Juergen leads a team of more than 16,000 people spread across 12 major hubs and co-located

Juergen Reiners Director

in 56 major countries including the U.S, India, China, Mexico, Costa Rica, Argentina, Poland, Romania and Singapore,

among others. With over two decades of experience, Juergen has held a variety of international senior management

positions both for HP and other companies. From 2004 - 2008, he was instrumental in setting up HP’s commercial BPO

outfit.

Gerard Brossard joined the Board of MphasiS on July 15, 2010. Brossard is Vice President of Strategy and Corporate

Development at HP. In this role, he is chartered with optimizing HP’s labor model and location footprint to create a

competitive human capital advantage that better positions the company to drive growth through improved sales

Gerard Brossard Director coverage, more effective service delivery and lower costs. He is accountable directly to the CEO and executive committee.

Prior to this role, as the Vice president of the Mergers & Acquisitions Integration organization, Brossard lead all aspects of

HP’s $13.9B acquisition and integration of EDS, delivering financial and operational targets on plan and budget. Brossard

has a Master of Science degree in Computer Science from MIAGE LYON 1 University in Lyon, France.

www.fullertonsecurities.co.in Page | 5