Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (8)

Similar to Novozymes: Customs Compliance and Leading Practices

Similar to Novozymes: Customs Compliance and Leading Practices (20)

Recently uploaded

Recently uploaded (20)

Novozymes: Customs Compliance and Leading Practices

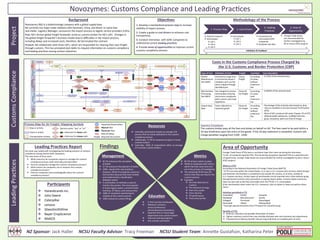

- 1. Novozymes: Customs Compliance and Leading Prac9ces 2. Cost Drivers 3a. Leading Prac9ces 3b. Areas of Opportuni9es v Contacted and interviewed SCRC companies v Analyzed raw data Valida&on & Feedback v Foreign Trade Zones are recommended for further inves9ga9on by NZ or future SCRC projects NZ Sponsor: Jack Haller NCSU Faculty Advisor: Tracy Freeman NCSU Student Team: AnneMe Gustafson, Katharina Peter Leading Prac9ces Customs Compliance Project Par&cipants v Hanesbrands Inc. v John Deere v Caterpillar v Lenovo v GlaxoSmithKline v Bayer CropScience v NAACO Educa&on v C-‐TPAT and ISA Cer9fica9on v Webinars, seminars, annual conferences and professional associa9ons v Exper9se from in-‐house legal department and customs brokers v Intensive training programs v Hire outside consultants Resources v Internally, par9cipants employ an average of 8 persons that are solely dedicated to the customs compliance process v Addi9onally, 71.4% of companies employ in-‐house customs brokers v Externally, 100% of respondents u9lize an average of 3 outside customs brokers Metrics Management v 85.7% of have metrics in place v 50.0% of companies with metrics admit that they need more and are in the process of inves9ga9ng v The remaining 50.0% have 26+ metrics that they use only for the customs process v Examples: v 85.7% outsource the calcula9on of du9es v 57.1% outsource the payment of du9es v 100% classify their own products; however, 28.6% of companies outsource this func9on because they have created and implemented a classifica9on database system v A combina9on of methods is used to monitor the process. The most popular: in-‐house legacy system, customs broker interface, GT Nexus, and manual entry v 100% of companies reported great visibility of the customs process v 100% outsource customs filings Area of Opportunity Foreign Trade Zones (FTZs) were a consistent topic that came up during the interviews. 71.4% of companies operate FTZs. The remaining companies reported FTZs as a poten9al area of opportunity. Foreign Trade Zones are recommended for further inves9ga9on by NZ or future SCRC projects. What is a FTZ? According to the Na9onal Associa9on of Foreign Trade Zones (NAFTZ), “A FTZ is an area within the United States, in or near a U.S. Customs port of entry, where foreign and domes>c merchandise is considered to be outside the country, or at least, outside of U.S. Customs territory. Certain types of merchandise can be imported into a Zone without going through formal Customs entry procedures or paying import du>es. Customs du>es and excise taxes are due only at the >me of transfer from the FTZ for U.S. consump>on. If the merchandise never enters the U.S. commerce, then no du>es or taxes are paid on those items.” Ac&vi&es permiEed in FTZ Assembled Tested Sampled Relabeled Manufactured* Stored Salvaged Processed Repackaged Destroyed Mixed Manipulated *must get special permission from FTZ board for manufacturing Benefits of FTZs v Deferral, reduc9on and possible elimina9on of du9es v Tighter inventory control that may virtually eliminate year-‐end inventory loss adjustments v Poten9al direct delivery benefit reduces long hold 9mes at crowded ports of entry Background Novozymes (NZ) is a biotechnology company with a global supply base. NZ currently has major trade rela9ons with Denmark, China, and Brazil; to name few. Jack Haller, Logis9cs Manager, outsources the import process to logis9c service providers (LSPs). Past: NZ’s former global freight forwarder acted as customs broker for NZ’s LSPs. Changes in the global freight forwarder’s business model lead to difficul9es in the import process, including delays and increased costs; therefore, NZ terminated the contract. Present: NZ collaborates with three LSP’s, which are responsible for clearing their own freight through customs. This has prompted Jack Haller to request informa9on on customs compliance and leading prac9ces among various industries. Costs in the Customs Compliance Process Charged by the U.S. Customs and Border Protec&on (CBP) Type of Cost Defini&on of Cost Freight Cost Base Cost Calcula&on Harbor Maintenance Fee (HMF) Commercial cargo from a commercial vessel is charged a port use fee when shipped through iden9fied port Ocean freight According to value, without maximum fee -‐ 0.125% of the entered value Merchandise Processing Fee (MPF) Fee charged to process merchandise entering and ensure compliance with customs and trade regula9ons Ocean & Air freight According to value, with maximum fee -‐ 0.3464% of the entered value Import Duty Rate Taxes collected on imported goods Ocean & Air freight According to value, without maximum fee -‐ Percentage of the entered value based on duty rates as classified in the Harmonized Tariff System (HTS) -‐ Most of NZ’s products fall under Chapter 35 of HTS (Albuminoidal substances; modified starches; glues; enzymes), which are free of charge Payment Procedures The customs broker pays all the fees and du9es on behalf on NZ. The fees need to be paid within a 10-‐day 9meframe upon the entry of the goods. If the 10-‐day statement is exceeded, customs will charge penal9es ranging from $100 -‐ $200. 1. Process Map 2. Cost Drivers 3. Leading Prac9ces 4. Area of Opportunity v Interviewed v External research v Interviewed v LSP 1 v LSP 2 v LSP 3 v LSP 1 v LSP 2 v LSP 3 Objec&ves 1. Develop a standardized process map to increase visibility of import process 2. Create a guide to cost drivers to enhance cost transparency 3. Conduct interviews with SCRC companies to understand current leading prac;ces 4. Provide areas of opportuni;es to improve current customs compliance process Process Map for Air Freight: Mapping Symbols Step or ac9vity Input or output Transporta9on ac9vity Decision point: “yes” or “no” Inspec9on/Examina9on Outcome for faster path Outcome for slower path Manual flow Electronic flow Risks & Delays Red Required documents Purple Leading Prac&ces Report Our team was tasked with inves9ga9ng the leading prac9ces of customs compliance among several SCRC companies. The main areas of focus were v Accurate data sent to customs v Pre-‐clearance of cargo v Post-‐entry audits v Entry volumes v ISF performance v Track entry by filer Methodology of the Process Findings v What resources do companies require to manage the customs compliance process, both internally and externally? v How do companies manage the customs compliance process? v What metrics do companies use to measure the customs compliance process? v How do companies stay knowledgeable about the customs compliance process?