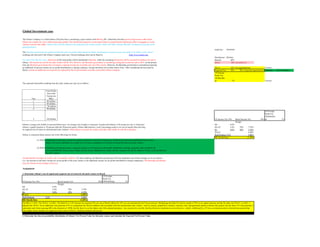

2. Year 0 N1 N2 N3 N4 N5 Initial Outflow

Total Profits in BRL 0 40,000,000$ 60,000,000$ 70,000,000$ 90,000,000$ 120,000,000$ 8,000,000$

Profits Allocated to

Gibson (40%) 0 16,000,000$ 24,000,000$ 28,000,000$ 36,000,000$ 48,000,000$

Income Taxes by Brazilian

Gov (10%) 0 1,600,000$ 2,400,000$ 2,800,000$ 3,600,000$ 4,800,000$ ##########

Profits After Brazilian

Gov Taxes 0 14,400,000$ 21,600,000$ 25,200,000$ 32,400,000$ 43,200,000$ 48,234,200.00000$

Gibson's Profits (BRL-$

Conversion @

1BRL=0.31414USD) 0 4,523,616$ 6,785,424$ 7,916,328$ 10,178,136$ 13,570,848$ BRL

Less: US Expatriated

Taxes Paid (7%) 0 316,653$ 474,980$ 554,143$ 712,470$ 949,959$

CFs From JV 0 4,206,963$ 6,310,444$ 7,362,185$ 9,465,666$ 12,620,889$

PV CFs (8,000,000)$ 3,773,738$ 5,077,688$ 5,313,930$ 6,128,629$ 7,330,020$

Total PV of CFs ########## Safety Margin 42.38% IRR 53.86%

NPV ##########

Year 0 N1 N2 N3 N4 N5 Initial Outflow

Total Profits in BRL 0 40,000,000$ 60,000,000$ 70,000,000$ 90,000,000$ 120,000,000$ 8,000,000$

Profits Allocated to

Gibson (40%) 0 16,000,000$ 24,000,000$ 28,000,000$ 36,000,000$ 48,000,000$

Income Taxes by Brazilian

Gov (30%) 0 4,800,000$ 7,200,000$ 8,400,000$ 10,800,000$ 14,400,000$ ########## 144702000.00

Profits After Brazilian

Gov Taxes 0 11,200,000$ 16,800,000$ 19,600,000$ 25,200,000$ 33,600,000$ BRL

Gibson's Profits (BRL-$

Conversion @

1BRL=0.31414USD) 0 3,518,368$ 5,277,552$ 6,157,144$ 7,916,328$ 10,555,104$

Less: US Expatriated

Taxes Paid (0%)*** 0 -$ -$ -$ -$ -$

CFs From JV 0 3,518,368$ 5,277,552$ 6,157,144$ 7,916,328$ 10,555,104$

PV CFs (8,000,000)$ 3,156,053$ 4,246,573$ 4,444,147$ 5,125,496$ 6,130,243$

Total PV of CFs ########## Safety Margin 31.89% IRR 43.37%

NPV ##########

Year 0 N1 N2 N3 N4 N5 Initial Outflow

Total Profits in BRL 0 40,000,000$ 60,000,000$ 70,000,000$ 90,000,000$ 120,000,000$ 8,000,000$

Profits Allocated to

Gibson (40%) 0 16,000,000$ 24,000,000$ 28,000,000$ 36,000,000$ 48,000,000$

Income Taxes by Brazilian

Gov (10%) 0 1,600,000$ 2,400,000$ 2,800,000$ 3,600,000$ 4,800,000$ ##########

Profits After Brazilian

Gov Taxes 0 14,400,000$ 21,600,000$ 25,200,000$ 32,400,000$ 43,200,000$

Brazil Witholding Tax

(10%) 1,440,000$ 2,160,000$ 2,520,000$ 3,240,000$ 4,320,000$ ##########

Profits After Brazilian

Withholding Taxes 12,960,000$ 19,440,000$ 22,680,000$ 29,160,000$ 38,880,000$ 28,880,000$

This net increase in corporate income taxes in Brazil resulted in an "initial" tax credit of 20% (30%Brazil vs 10%US) considering US taxes are

still 10%. Consequently, the increase in these tax outflows required by Brazil created a tax credit which eliminated the US Withholdings tax of

7%. However, this scenario resulted in a lower NPV as the tax outflows - due to increased Brazilian Gov income taxes - became greater than the

tax benefit received by the US when 0% taxes were distributed to the US via withholding taxes. This resulted in a larger tax outflow, and

consequently, lower profitability comparative to scenario 1. Undertaking this project would carry a greater opportunity cost and investment risk

considering the expected reward is lower than before, at the same project hurdle rate. In other words, the risk reward relationship is lower, or not

optimized, at the same risk requirement - lowering our Alpha = return per unit of risk. Undertaking this project would significantly reduce our

forecasted CFs, ROIC, IRR, and NPV. For example, the NPV was significantly reduced from $19,634,005 to 15,102,513. However, the NPV is

still significantly high and would produce advantageous synergies in the future regarding profitability and DCFs. Since the IRR of outcome 2

(43.37%) is still high and is > 11.48 (Hurdle Rate), and significantly larger, we have a high margin of safety (31.89%) before our actual return

using DCFs that would adversely produce a NPV of 0 or break-even - indicating we have flexibility before the returns deviate into negative

territory. The likelihood/probability of a positive return on invested capital, adjusted for various risk factors, is high.

With a RR of 11.48%; a JV project lifetime of 5 years; and PVCFs of $27,634,005 - our NPV is $19,624,005 after adjusting the WACC of 6.48%

to include an added risk premium of 5%. Consequently, our discount rate or project hurdle rate to discount CFs to their present worth today, is

11.48%. This RR accounts for country, geopolitical, increased taxes, and generated capital to finance this project. After accounting for Brazilian

and US tax implications and outflows, currency conversion assumptions, and additional risks just mentioned to discount the PV of all expected

CFs; the NPV is $19,624,005. Since the IRR of outcome 1 (53.86%) is the highest of the project scenarios and is > 11.48 (Hurdle Rate), and

significantly larger, we have a high margin of safety (42.38%) before our actual return using DCFs that would adversely produce a NPV of 0 or

break-even - indicating we have flexibility before the returns deviate into negative territory. The likelihood/probability of a positive return on

invested capital, adjusted for various risk factors, is high.

Scenario 1: Origional Assumptions

Scenario 2: Increased Brazilian Fed Income Tax

Scenario 3: Increased Brazilian Withholding Tax

3. Gibson's Profits (BRL-$

Conversion @

1BRL=0.31414USD) 0 4,071,254$ 6,106,882$ 7,124,695$ 9,160,322$ 12,213,763$

Less: US Expatriated

Taxes Paid (7%) 0 284,988$ 427,482$ 498,729$ 641,223$ 854,963$ BRL

CFs From JV 0 3,786,267$ 5,679,400$ 6,625,967$ 8,519,100$ 11,358,800$

PV CFs (8,000,000)$ 3,396,364$ 4,569,919$ 4,782,537$ 5,515,766$ 6,597,018$

Total PV of CFs ########## Safety Margin 36.05% IRR 47.53%

NPV ##########

eNPV Analysis A B eNPV

Original ########## 60% 11,774,403.03$

Increased Income Tax ########## 20% 3,020,502.64$

Increased Withholding Tax ########## 20% 3,372,320.91$

Totals 100% 18,167,226.57$

3. Would you recommend that Gibson participate in the joint venture? Explain.

eNPV Analysis A B eNPV

Original ########## 60% 11,774,403.03$

Increased Income Tax ########## 20% 3,020,502.64$

Increased Withholding Tax ########## 20% 3,372,320.91$

Totals 100% 18,167,226.57$

4. What do you think would be the key underlying factor that would have the most influence on the profits earned in Brazil as a result of the joint venture?

5. Under what circumstances might Gibson shift to more equity financing when considering joint ventures like this? What is the minimum required return that

would still make this investment worthwhile?

This net increase in Brazilian Withholding taxes resulted in a lower NPV as the tax outflows - due to increased Brazilian Withholding taxes -

were greater than the outflows required by the initial assumptions (Option 1), but these outflows were still lower than the cash outflows required

by Option 2 when Brazil's Federal Income Taxes were substantially higher. Undertaking this project would carry a greater opportunity cost and

investment risk comparative to Scenario 1 considering the expected reward is lower than before, at the same project hurdle rate. In other words,

the risk reward relationship is lower, or not optimized, at the same risk requirement - lowering our Alpha = return per unit of risk. Undertaking

this project would Moderately reduce our forecasted CFs, ROIC, IRR, and NPV. The NPV is still significantly high and would produce

advantageous synergies in the future regarding profitability and DCFs. Since the IRR of outcome 3 (47.53%) is still high and is > 11.48 (Hurdle

Rate), and significantly larger, we have a high margin of safety (36.05%) before our actual return using DCFs that would adversely produce a

NPV of 0 or break-even - indicating we have flexibility before the returns deviate into negative territory. The likelihood/probability of a positive

return on invested capital, adjusted for various risk factors, is high. This scenario would produce greater DCFs and NPV if this option

materialized instead of option 2 where income taxes were increased.

Yes. Under either scenario, the NPV is highly positive and, when combined, The NPV is still high and close the best scenario available - Scenario

1. Either outcome will help generate a risk-adjusted return provided to shareholders via wealth maximization thru value-added expansion

opportunities, create prosperous financial economic benefits for the firm's future, its operating capacity, and help spread fixed costs. Simply, the

project is profitable and beneficial regardless of which mutually exclusive scenario plays out. Scenario 1, however, will maximize shareholder

wealth creation and optimize alpha and firm profitability.

Additionally, FCF would increase if the firm decided to retain a portion of its ROIC a few years after expansion as long as its future operating

cash flows increased and its future CapEX decreased proportionately. This would fuel money to develop new and/or existing products, improve

the quantity and scope of value-added investments, enable the firm to maintain its payout ratio while still increasing dividends, and increase stock

buybacks to improve EPS and share price appreciation.

The IRR of all outcomes are significantly larger than our hurdle rate, and we have a high margin of safety before our actual return using DCFs

that would adversely produce a NPV of 0 or break-even - indicating we have flexibility before the returns deviate into negative territory. The

likelihood/probability of a positive return on invested capital, adjusted for various risk factors, is high regardless of which option plays out.

First off, the tax implications are a key factor that will have an impact on profits earned in Brazil. The implications and milestones of this project

must be prudently analyzed considering this project has a definite lifetime and benefits will stop in the future after the terminal value. An

additional key variable to consider is the future economic conditions such as GDP per capita, export costs and tariffs; GDP; and existing market

share and potential for our firm to capture a portion of it. Coffee is heavily demanded from local Brazilian “coffee farmers” where cut-rate prices

are offered to big business such as Starbucks in the US. Will foreign demand really be high? Brazil is an emerging market which implies added

risk is necessary considering political and economic forces are more volatile than here in the US. Consequently, profit estimates are extremely

volatile. The tax implications, followed by adjustments made to the WACC for an additional risk premium of 5% to compensate the firm for

addition risk associated with this international joint venture - such as country, geopolitical, currency risks, and generated capital to finance this

project; and the fact that future tax implications are not known - volatile. Additionally, a JV has a set duration and is a limited time partnership.

This implies future benefits are capped and must return a ROI in a definitely defined time period.

Gibson might consider additional equity financing as their capital structure is burdened with debt of 70%. This implies the firm is highly levered.

If Gibson believes these CFs are highly volatile, the firm should use equity to deleverage this investment so it can ensure sufficient cash is

available to repay debt and interest expenses as they mature. If additional equity were used, this would increase the WACC and RR as equity is

always more expensive to finance than debt; and decrease the eNPVs, profitability, and expected returns associated with each mutually exclusive

option.

4. 6. When Gibson was assessing this proposed joint venture, some of the managers in the company recommended that it borrow the Brazilian currency rather

than using US dollars to obtain some of the necessary capital for the initial investment. They suggested that such a strategy could reduce Gibson’s exchange

rate risk. Do you agree? Explain.

PPP

IRP

7. Discuss the benefits of the joint venture from the perspective of Brasilia. What is the maximum amount of money Brasilia should invest?

For the Government, great benefits - considering implications of increased tax revenue (especially under scenario 2 or 3), but no benefits

regarding worker implications of increased competition (rivalry) and local business market share dilution - this could impact the prospects of local

emerging market synergies.

For the firm to invest more in its Brasilia plant, it would be most advantageous to invest (accordingly) if option 1, 3, or 2 occurred respectively.

If the Brasilia division were to invest more than 60% of aggregate profits and remit less than 40%, the RR would increase as additional risk would

need to be accounted for. I believe this combination (60 vs 40) is exceptional considering the majority of these earnings are being reinvested into

the core operations at the Brasilia plant, while the remitted earnings are benefiting the US firm to expand with more capital towards more and

diversely beneficial investments. This combination seems to benefit both plants involved. If an increase was desired I would place a 70%

reinvested cap as any greater would leave the firm unruly exposed and leveraged beyond their means.

Such an increase in the currently retained earnings (60%) at the Brasilia plant would increase the firms degree of finanvial leverage as the

majority of financing seems to be levered via debt. As long as the interest expense tax deductions produce synergies - and the capital

structure permits greater debt financing without being over-levered - an increase in financial leverage will produce greater shareholder

weath maximization (greater increases in EPS and EBIT correlation) as long as the DOL is low and ROIC > Kd.

If Brasilia's government were to invest, per say, they should invest accordingly to their net advantage in increased tax revenue provided each

scenario. Scenario 2 is best for Brasilia, followed by scenario 3 and 1. Scenario 2 = $45,600,000 or BRL 144,702,000 in aggregate tax revenue;

Scenario 3 = $28,880,000 or BRL 91,644,900; and Secnario 1 will generate $15,200,000 or BRL 48,234,200.

The minimum required return that will make this investment worthwhile is our adjusted WACC or project hurdle rate of 11.48%. Any return at or

below will produce a neutral or negative ROIC respectively. Thus, as long as the return is slightly greater than the RR, the investment is

worthwhile as it will produce profitable DCFs.

Purchasing Power Parity (PPP) suggests that a home currency will depreciate if the current home inflation rate exceeds the current foreign inflation rate. In other

words, PPP indicates that relatively high inflation will cause imports to increase, exports to decrease, and the local currency should depreciate by the inflation

differential between the two countries; or vice versa. This will help restore the currencies towards equilibrium, overtime, where the same basket of goods costs

the same in both currencies. For example, assume that the inflation rate in The US is 3%, while the inflation rate in Brasilia is 8%. According to PPP, the USD

should appreciate by 4.85% ((1+0.08)/(1+0.03)-1) as demand for the BRL, comparative to the USD, will decrease – pushing the two currencies towards parity.

I agree. The Predetermined fixed exchange rate will produce a loss or a gain if BRL is converted to USD. If US inflation > BR inflation; there will be an

inflation loss upon conversion of the BRL to USD; as the USD would depreciate comparative to the BRL. If US inflation is < BR inflation, the fixed

exchange rate will increase purchasing power and generate a gain when the BRL is converted into USD; as the USD would appreciate comparative to the BRL.

Consequently, borrowing money in BRL and receiving profits in BRL would eliminate inflation risk as it takes cash flows denominated in USD (if we

were to borrow in USD) out of the equation – eliminating the PPP inflation volatility effect - reducing a portion of its exchange rate risk and helping it

have more certainties regarding principal and interest payments to monitor its levered capital investment into Brasilia.

An increase in US interest rates will cause an increase in demand for the Dollar, supply would decrease, and the value of the Dollar would appreciate. A higher

US interest rate, comparative to a foreign currency with a lower interest rate, leads to an increase in demand for US deposits and a decrease in demand for foreign

deposits, leading to an increase in demand for USD and an increased exchange rate for the dollar. However, a strong Dollar places downward pressure on

inflation, which consequently places upward pressure on the dollar and will typically increase unemployment.

5. Problem Assignments: Week 8

Assigned

Problems

1 Ann Page Co. … fixed costs $30,000 per year. Variable costs per unit are $17. Sales price per unit is $30.

a) What is the contribution margin of the product?

Fixed Costs 30,000$

Var $ Per Unit 17$

MSRP 30$

Variable Cost

Per Unit

(VCR) 56.67%

CM Ratio 43.33%

CM Per Unit 13.00$

b) Calculate the breakeven point in unit sales and dollars.

69,230.77$

2,308

c) What is the operating profit (loss) at:

i) 1,500 units per year?

Revenue 45,000$

Var Costs 25,500$

Fixed Costs 30,000$

Profit (NOL) (10,500)$

ii) 3,600 units per year?

Revenue 108,000$

Var Costs 61,200$

Fixed Costs 30,000$

Profit (NOL) 16,800$

d) Plot a breakeven chart using the foregoing figures.

Units 1,500 2,308 3,600

Fixed $ 30,000$ 30,000$ 30,000$

Var $ 25,500$ 39,230.77$ 61,200$

Fixed + Var $ 55,500$ 69,230.77$ 91,200$

Sales 45,000$ 69,230.77$ 108,000$

Profit (NOL) (10,500)$ -$ 16,800$

2 Mrs. Jones owns 100 shares of stock in Daimler-Benz valued at 16.5 Euros per share. What is the value in $U.S. of her stock if:

a) 0.90 € = $1 16.5 EUR Per

Value USD 1,485.00$ Less than 1,650 EUR Good 100 Shares

1,650.00 EUR

b) 0.70 € = $1

Value USD 1,155.00$ Less Good

c) 1.20 € = $1

Value USD 1,980.00$ Greater Good

3 John is planning on purchasing his German dream car for 65,000 Euros

How much does he need in $U.S. if there are 0.98 Euros to the $U.S.?

63,700$ USD

For every unit sold the Contribution Margin Ratio is 43.33% of the Selling Price of $30 or equivalent to $13. This implies the

company makes $13 per unit when accounting for variable costs that increase in proportion with the number of units produced.

When marginal costs = marginal revenue (economies of scale), profitability will be maximized, fixed costs will be spread out,

and variable costs will be efficiently minimized per unit of output.

Breakeven Sales in $ = Fixed Costs/(1-VCR)

Breakeven Sales in Units =Breakeven Sales/MSRP

Since the EUR is worth more than the USD, the EUR-USD conversion will produce a smaller number. When 0.98EUR = $1USD; 65,000

EUR = $63,700USD

When the USD>EUR; the US denominated value of the stock will be greater than the value of the same amount of stock in EURs - and

vice versa. Simply multiply the USD value per EUR with the amount the stock is valued at (16.50 EUR) then multiply this value by the

number of stocks owned (100). When the USD>EUR, her stocks are worth more in USD - and vice versa.

This number implies the firm must make $69,230.77 in Sales Rev to breakeven. Anything less will result in a NOL.

This number implies the firm must sell 2,308 Units to breakeven. Anything less will result in a NOL.

Inferred from the graph, when the firm produces and sells 3,600 units, its fixed costs are spread out more per unit which

decreases the cost per unit sold on a fixed cost basis. This results in a Net Profit vs a NOL (as when the firm sold 1,500 units).

The firm must sell 2,308 units or make $69,230.77 in sales revenue to breakeven. With 1,500 units sold a NOL will result as

the number of units sold is less than what the firm needs to breakeven. Any sales scenario to the right of this breakeven plot,

the firm will make a profit - and vice versa. With a Variable Cost Ratio of 56.67%, sales and profitability are highly sensitive.

1,500 2,308 3,600

$30,000 $30,000 $30,000

$25,500

$39,230.77

$61,200

$55,500

$69,230.77

$91,200

$45,000

$69,230.77

$108,000

-

20,000

40,000

60,000

80,000

100,000

120,000

1 2 3

Profit

Units

Breakeven Sensitivity Analysis

Units

Fixed $

Var $

Fixed + Var $

Sales