QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

12 January Daily market report

1. Page 1 of 6

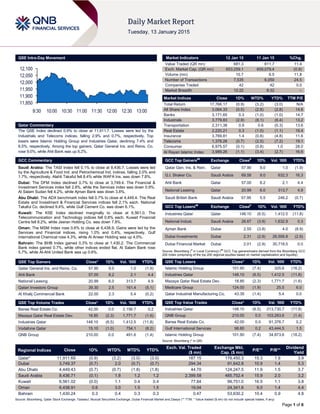

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 0.9% to close at 11,911.7. Losses were led by the

Industrials and Telecoms indices, falling 2.9% and 0.7%, respectively. Top

losers were Islamic Holding Group and Industries Qatar, declining 7.4% and

6.5%, respectively. Among the top gainers, Qatar General Ins. and Reins. Co.

rose 9.0%, while Ahli Bank was up 8.2%.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.1% to close at 8,436.7. Losses were led

by the Agriculture & Food Ind. and Petrochemical Ind. indices, falling 2.0% and

1.7%, respectively. Alahli Takaful fell 8.4% while WAFA Ins. was down 7.8%.

Dubai: The DFM Index declined 0.7% to close at 3,749.4. The Financial &

Investment Services index fell 2.8%, while the Services index was down 0.9%.

Al Salam Sudan fell 4.2%, while Ajman Bank was down 3.8%.

Abu Dhabi: The ADX benchmark index fell 0.7% to close at 4,449.4. The Real

Estate and Investment & Financial Services indices fell 2.1% each. National

Takaful Co. declined 9.4%, while Gulf Cement Co. was down 6.1%.

Kuwait: The KSE Index declined marginally to close at 6,561.0. The

Telecommunication and Technology indices fell 0.8% each. Kuwait Financial

Centre fell 8.2%, while Jeeran Holding Co. was down 7.8%.

Oman: The MSM Index rose 0.6% to close at 6,438.9. Gains were led by the

Services and Financial indices, rising 1.0% and 0.4%, respectively. Gulf

International Chemical rose 4.3%, while Al Anwar Holding was up 4.0%.

Bahrain: The BHB Index gained 0.3% to close at 1,430.2. The Commercial

Bank index gained 0.7%, while other indices ended flat. Al Salam Bank rose

5.7%, while Al-Ahli United Bank was up 0.6%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar General Ins. and Reins. Co. 57.90 9.0 1.0 (1.9)

Ahli Bank 57.00 8.2 2.1 4.4

National Leasing 20.99 6.0 313.7 4.9

Qatari Investors Group 39.30 2.5 161.4 (5.1)

Al Khalij Commercial Bank 22.00 2.3 5.4 (0.2)

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 42.00 0.0 2,156.7 0.2

Mazaya Qatar Real Estate Dev. 18.85 (2.3) 1,771.7 (1.6)

Industries Qatar 148.10 (6.5) 1,412.5 (11.8)

Vodafone Qatar 15.10 (1.0) 754.1 (8.2)

QNB Group 210.00 0.0 491.6 (1.4)

Market Indicators 12 Jan 15 11 Jan 15 %Chg.

Value Traded (QR mn) 681.3 611.7 11.4

Exch. Market Cap. (QR mn) 653,259.1 659,079.4 (0.9)

Volume (mn) 10.7 9.5 11.8

Number of Transactions 7,535 6,050 24.5

Companies Traded 42 42 0.0

Market Breadth 12:22 8:32 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 17,766.17 (0.9) (3.2) (3.0) N/A

All Share Index 3,064.33 (0.5) (2.8) (2.8) 14.6

Banks 3,171.65 0.3 (1.0) (1.0) 14.7

Industrials 3,779.83 (2.9) (8.1) (6.4) 13.2

Transportation 2,311.38 0.9 0.6 (0.3) 13.6

Real Estate 2,220.21 0.3 (1.0) (1.1) 19.4

Insurance 3,769.81 1.4 (0.8) (4.8) 11.6

Telecoms 1,378.28 (0.7) (2.5) (7.2) 19.1

Consumer 6,975.57 (0.1) (0.8) 1.0 28.0

Al Rayan Islamic Index 3,989.26 (1.1) (3.4) (2.7) 16.6

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Qatar Gen. Ins. & Rein. Qatar 57.90 9.0 1.0 (1.9)

G.I. Shaker Co. Saudi Arabia 69.58 9.0 632.3 16.3

Ahli Bank Qatar 57.00 8.2 2.1 4.4

National Leasing Qatar 20.99 6.0 313.7 4.9

Saudi British Bank Saudi Arabia 57.95 5.5 246.2 (0.7)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Industries Qatar Qatar 148.10 (6.5) 1,412.5 (11.8)

National Indust. Saudi Arabia 26.67 (3.9) 1,632.9 0.3

Ajman Bank Dubai 2.55 (3.8) 4.0 (8.9)

Dubai Investments Dubai 2.31 (2.9) 26,556.8 (2.9)

Dubai Financial Market Dubai 2.01 (2.9) 30,718.5 0.0

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 101.90 (7.4) 325.6 (18.2)

Industries Qatar 148.10 (6.5) 1,412.5 (11.8)

Mazaya Qatar Real Estate Dev. 18.85 (2.3) 1,771.7 (1.6)

Medicare Group 124.00 (1.9) 25.5 6.0

Qatar Industrial Manufacturing Co. 43.35 (1.4) 5.4 0.0

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Industries Qatar 148.10 (6.5) 213,730.7 (11.8)

QNB Group 210.00 0.0 103,283.6 (1.4)

Barwa Real Estate Co. 42.00 0.0 91,376.7 0.2

Gulf International Services 98.60 0.2 43,444.5 1.5

Islamic Holding Group 101.90 (7.4) 34,873.6 (18.2)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,911.69 (0.9) (3.2) (3.0) (3.0) 187.15 179,450.3 15.3 1.9 3.9

Dubai 3,749.37 (0.7) 2.0 (0.7) (0.7) 294.34 91,642.8 10.9 1.4 5.3

Abu Dhabi 4,449.43 (0.7) (0.7) (1.8) (1.8) 44.70 124,247.5 11.9 1.5 3.7

Saudi Arabia 8,436.71 (0.1) 1.8 1.2 1.2 2,399.58 485,752.4 15.9 2.0 3.2

Kuwait 6,561.02 (0.0) 1.1 0.4 0.4 77.84 99,751.0 16.5 1.1 3.8

Oman 6,438.91 0.6 3.0 1.5 1.5 19.04 24,341.6 9.0 1.4 4.4

Bahrain 1,430.24 0.3 0.4 0.3 0.3 0.47 53,630.2 10.4 0.9 4.8

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,850

11,900

11,950

12,000

12,050

12,100

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index declined 0.9% to close at 11,911.7. The

Industrials and Telecoms indices led the losses. The index fell on

the back of selling pressure from non-Qatari shareholders

despite buying support from Qatari shareholders.

Islamic Holding Group and Industries Qatar were the top losers,

declining 7.4% and 6.5%, respectively. Among the top gainers,

Qatar General Ins. and Reins. Co. rose 9.0%, while Ahli Bank

was up 8.2%.

Volume of shares traded on Monday rose by 11.8% to 10.7mn

from 9.5mn on Sunday. Further, as compared to the 30-day

moving average of 15.5mn, volume for the day was 31.1% lower.

Barwa Real Estate Co. and Mazaya Qatar Real Estate Dev.

were the most active stocks, contributing 20.2% and 16.6% to

the total volume respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Finance House

(FH)

Capital

Intelligence

Abu

Dhabi

LT CR/ST CR BBB-/A3 BBB-/A3 – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency, CR – Corporate Ratings)

Earnings Releases

Company Market Currency

Revenue

(mn) 4Q2014

% Change

YoY

Operating Profit

(mn) 4Q2014

% Change

YoY

Net Profit (mn)

4Q2014

% Change

YoY

Saudi Arabia Fertilizers Co. Saudi SR – – 715.0 8.7% 779.0 -2.9%

Gulf Mushroom Products* Oman OMR 6.1 4.0% – – 0.3 -38.0%

Source: Company data, DFM, ADX, MSM (*FY2014 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

01/12 US US Treasury 3M High Yield Rate 12-January 0.03% – 0.03%

01/12 US US Treasury 6M High Yield Rate 12-January 0.09% – 0.11%

01/12 France Ministry of Economy 3M T-Bill Amount Sold 12-January EU2,991M – EU3,999M

01/12 France Ministry of Economy 3M T-Bill Average Yield 12-January -0.11% – -0.05%

01/12 France Ministry of Economy 3M T-Bill Bid/Cover Ratio 12-January 3.7 – 2.6

01/12 France Ministry of Economy 6M T-Bill Amount Sold 12-January EU1,594M – EU1,894M

01/12 France Ministry of Economy 6M T-Bill Average Yield 12-January -0.10% – -0.04%

01/12 France Ministry of Economy 6M T-Bill Bid/Cover Ratio 12-January 4.2 – 2.9

01/12 France Ministry of Economy 12M T-Bill Amount Sold 12-January EU1,995M – EU1,493M

01/12 France Ministry of Economy 12M T-Bill Average Yield 12-January -0.10% – -0.05%

01/12 France Ministry of Economy 12M T-Bill Bid/Cover Ratio 12-January 3.2 – 3.7

01/12 UK Lloyds Bank Lloyds Employment Confidence December -2.0 – 1.0

01/12 UK London Gold Market Fix. London Gold Market PM Fix 12-January 1,226.5 – 1,217.8

01/12 Spain INE House transactions YoY November 14.00% – 16.00%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

MEED: Qatar to see $30bn new project deals in 2015 –

According to the latest data from MEED Projects, Qatar's

infrastructure projects pipeline is set to soar with more than

$30bn worth of new projects deals happening in 2015. There will

be major project awards as part of the Public Works Authority’s

(Ashghal) expressway, local roads and drainage programs, as

well as significant investment in real estate and transport

projects such as Lusail and the New Port Project. This year will

be boosted by project awards on the Al Karaana petrochemical

complex worth more than $5bn, the rolling stock & systems

contract on the Doha Metro exceeding $2bn, and five multi-

billion dollar packages on the mega water reservoirs.

Meanwhile, the MEED Qatar Projects Conference will be held

on March 10 and 11, 2015 on the theme: The resilience of

Qatar’s economy and its commitment to the objectives of the

Qatar National Vision 2030. (Gulf-Times.com, Peninsula Qatar)

MEC issues 629 commercial licenses in December – The

Ministry of Economy & Commerce (MEC) issued 629 new

commercial licenses in December 2014, registering a drop of

14.5% over November 2014. Al Rayyan Area got the largest

number of new licenses (279), followed by Doha (239). Both

municipalities constituted 82.4% of the newly issued commercial

licenses in December. Further, MEC issued 570 main

commercial registrations, and 559 branch commercial

Overall Activity Buy %* Sell %* Net (QR)

Qatari 67.18% 59.17% 54,556,856.09

Non-Qatari 32.82% 40.83% (54,556,856.09)

3. Page 3 of 6

registrations. The total number of new commercials registrations

dropped by 2% as compared to November. (Gulf-Times.com)

Amwal: Qatar may see deficit if oil stays at $50 in 2015 –

According to Amwal, Qatar's leading independent asset

management firm, Qatar may see a budget deficit of $5-10bn in

2015 if crude remains at $50 in 2015, but massive sovereign

wealth fund (SWF) assets will provide cushion to support capital

spending. Oil prices currently hover around a five-and-a-half

year low with the possibility of dropping further to $40 a barrel.

Even at lower oil prices, Amwal does not expect current

expenditure to be immediately affected, since the GCC countries

have “significant” savings to weather a period of low oil prices.

(Gulf-Times.com)

SIIS BoD to meet on February 1 – Salam International

Company’s (SIIS) board of directors will meet on February 1,

2015 to discuss and approve the financial results for the year

ended December 31, 2014. (QSE)

ORDS to pay interest to bondholders – Ooredoo (ORDS)

announced that its wholly owned subsidiary, Ooredoo

International Finance Limited (OIFL) will pay its Global Medium

Term Note (GMTN) holders both principal and interest payments

amounting $11.3mn, on February 2, 2015. (QSE)

MoE drafts new law to protect environment – The Minister of

Environment (MoE) HE Mr. Ahmed Amer Mohamed Al Humaidi

said that the Ministry has drafted a new law to protect wildlife

and end the growing violations that threaten Qatar’s

environment. The proposed law is ready and will be tabled

before the Cabinet soon for approval. The ministry set up a legal

committee to amend the existing environment law. Meanwhile,

Al Sharq has reported that the ministry cancelled the licenses of

10 winter camps on moral ground. The Minister said that the

violators have been blacklisted and will not get license next year

for camping. (Peninsula Qatar)

Al Dhameen offers QR174mn aid to 69 SMEs in 2014 – Qatar

Development Bank’s (QDB) Al Dhameen Manager Jawaher al-

Noaimi said that ‘Al Dhameen’ program has guaranteed some

69 SME with a total value of QR174mn in 2014. Al Dhameen

has helped SMEs in Qatar overcome the challenges they face

when seeking commercial financing. The program has also

helped banks overcome reservations about financing SMEs due

to the high-risk ratio of some in the sector. Doha Bank (DHBK)

organized a SME customer meet related to the projects financed

under the Al Dhameen guarantee program of QDB. Doha Bank’s

Group CEO, Dr. R Seetharaman said that SMEs are expected to

play an important role in supporting Qatar’s economic

diversification. Doha Bank will participate in Qatar’s

diversification story by encouraging the SME sector. (Gulf-

Times.com, Peninsula Qatar)

International

OECD indicator signals stable growth; Germany flagging –

The Organization for Economic Cooperation & Development

(OECD) said economic growth is set to remain stable across the

OECD area as a whole and in the Eurozone, despite signs that

Germany losing steam. The Paris-based organization’s monthly

leading indicator covering 33 countries, showed further signs of

slowing in Germany and Italy, but there was stability in the

Eurozone. France saw marginal improvement with the OECD's

index of growth, rising from 100.2 in October to 100.3 in

November. However, the index dipped in Germany to 99.5 in

November from 99.6 in October and in Italy to 101.0 in

November from 101.1 in October. The index remained stable at

100.6 for the Eurozone as a whole. For the broader OECD area,

it nudged up to 100.5 in November from 100.4 October. China's

reading ticked up to 99.3 in November from 99.2 in October and

India's to 99.5 from 99.3. The US reading remained at 100.4 and

Japan held steady at 99.8. Britain's reading dipped to 100.3

from 100.4 and Russia's dipped more notably, to 99.8 from

100.2. (Reuters, WSJ)

ECB member calls for cap on possible QE program – The

European Central Bank’s (ECB) Governing Council Member

Christian Noyer said the ECB should cap the size of its

proposed government bond purchase plan, so as to avoid

crowding out private sector investors. The ECB Governing

Council meets on January 22 for its next policy meeting, when it

could decide to start printing money to buy large amounts of

government bonds, a step also known as Quantitative Easing

(QE) to prevent deflation. However, Noyer, who is also the

Governor of the French central bank, said nothing has been

decided so far. Meanwhile, ECB policymaker Ewald Nowotny

thinks that a Greek exit from the Eurozone would be a disaster

for Greece. The radical leftist Syriza Party is leading opinion

polls ahead of Greece's snap election on January 25, triggering

fears of a standoff with EU/IMF lenders that could result in

Greece leaving the Eurozone. (Reuters)

Deutsche Bank to present strategy changes in 2Q2015 –

According to the Deutsche Bank's two Chief Executives, Anshu

Jain and Juergen Fitschen, the bank will provide details of a new

strategy plan to its investors in 2Q2015. They said the bank

would review its strategy and profit targets in 2015 and possibly

sell its Postbank-branded retail unit, which would be a major

reversal since a planned turnaround in profitability has fallen

short of hopes. Fitschen said the bank's management was

convinced that its universal strategy was the right one but it

would change course if tighter regulations made it sensible to do

so. Germany's largest universal bank currently offers a broad

array of financial services worldwide, covering everything from

retail accounts to merger advice. (Reuters)

Japan can meet deficit-halving goal with FY2015-16 budget

– The Japanese Prime Minister Shinzo Abe said the country is

on course to meet his promise of halving the primary budget

deficit – excluding new bond sales and debt servicing – in the

FY2015-16. Abe, who is about to decide on a record budget with

reduced new borrowing, made this remark at a meeting of

officials from the government where the annual draft budget for

the fiscal year beginning April 1 was put forward. The annual

budget, to be approved by the cabinet and sent to the

Parliament later in January, highlights the need for the PM to

sustain growth, while curbing the heaviest debt burden in the

industrial world. (Reuters)

China’s December trade better than market forecasts – The

Chinese Customs Administration said the country’s exports rose

9.9% YoY in December, while imports fell 2.3%, which were

better than market expectations That left the country with a trade

surplus of CNY304.5bn for the month and has cushioned

pressure on the domestic economy from rising debt levels and a

soft property sector. Economists polled by Reuters had

estimated exports in December to accelerate to 6.8% YoY from

4.7% in November, while imports were forecast down 7.4%,

following a 6.7% drop in November. The official percentage

change figures were based on yuan, whereas previous changes

were calculated on a dollar basis. (Reuters)

India’s inflation quickens less than predicted as output

grows – Retail inflation in India accelerated less than

economists predicted and factory output grew before the central

bank Governor Raghuram Rajan reviews interest rates in

February and the government presents its annual budget. The

Statistics Ministry said consumer prices rose 5% YoY in

4. Page 4 of 6

December 2014, which when compared with November’s

4.38%, was the slowest since the index was created in January

2012. The Bloomberg median of estimates had forecasted for a

5.35% gain. Meanwhile, industrial production rose 3.8% in

November. That compared well with a 2.3% predicted gain, after

output shrank 4.2% in December. Rajan has held the

benchmark rate unchanged for a fifth meeting in December after

Finance Minister Arun Jaitley called for lower borrowing costs.

Rajan has indicated that he may ease policy in 2015, depending

on the pace of inflation, as well as expectations about price

pressures being lowered and the government meeting its budget

goals. (Bloomberg)

Regional

MENA M&A market sees $41bn deals in 2014 – According to

a report by Bureau van Dijk and MENA Research Partners, the

M&A market in the MENA region depicted strong activity during

4Q2014, prolonging its steady performance of the last two

years. The total number of M&A deals in the MENA region

climbed significantly in 4Q2014, with 137 deals worth an

aggregate $8.98bn. While the total number of completed deals

has been stabilizing at the low-end of its range since 2009, the

announced value of M&A reached $50bn in 2013 and $41bn in

2014, ahead of an average of $34bn during the previous three

years. From a geographic perspective, deal activity remains

driven by a strong performance in the GCC region, coupled with

an ongoing pick-up in selected Arab Spring countries like Egypt

and Morocco. The GCC region accounts for the bulk of the

deals, with 44% and 43%, respectively, of the announced value

and the volume of completed deals during 2014. (Zawya)

Bank AlBilad to increase capital by 25% – The board of

directors of Bank AlBilad have recommended raising the bank’s

share capital by 25% through an issue of bonus shares at a rate

of one bonus share for every four shares held. The capital will

stand at SR5bn after the increase. Shareholders registered at

the end of the trading day of Extraordinary General Assembly

meeting will be eligible for bonus shares. (GulfBase.com)

BSF reports 211% surge in 4Q2014 net profit – Banque Saudi

Fransi (BSF) reported a net profit of SR851mn in 4Q2014,

reflecting an increase of 210.6% YoY. EPS amounted to SR2.92

in 2014 as against SR2.0 a year earlier. The bank’s total assets

stood at SR188.8bn at the end of December 2014 as against

SR170.1bn a year ago. Loans & advances stood at SR116.5bn,

while customer deposits stood at SR145.3bn. (Tadawul)

Saudi CMA imposes penalty on various companies – The

Saudi Capital Market Authority’s (Saudi CMA) announced the

issuance of a board resolution to impose penalty on various

Saudi companies due to the violation of clause (A) of Article (9)

of the Corporate Governance Regulations. The companies are:

Najran Cement Company with a penalty of SR30,000, Saudi

Airlines Catering Company (SR40,000), Gulf Union Cooperative

Insurance Company (SR20,000), National Gypsum Company

(SR80,000), the National Agriculture Marketing Co. (SR40,000),

Bawan Company (SR10,000), Wafrah for Industry &

Development (SR30,000), and Northern Region Cement

Company (SR20,000). The board of directors’ report of the

above companies for FY2013 did not include the provisions that

were not implemented as per the Corporate Governance

Regulations and the reasons behind that. (Tadawul)

UAE to boost oil output even as prices drop – The UAE will

stick with its plan to increase its oil production capacity to 3.5mn

barrels a day by 2017, even as oversupply pushed global prices

to the lowest in more than five years. The UAE Energy Minister,

Suhail Al Mazrouei said that during this time of unstable oil

prices, the UAE remain dedicated to reach its long-term

production goals. (Reuters)

DDF targets AED7.7bn sales in 2015 – Dubai Duty Free

(DDF), helped by its first major push into online retailing, aims to

achieve AED7.7bn sales in 2015, a 10% rise over the

AED6.99bn sales achieved in 2014. Part of the growth is

expected form a new online sales channel offering more than

3,500 products. The move online is intended to save travelers’

time in Dubai’s duty free shopping concourses by offering a pay-

and-pick-up service before travel. It also adds an additional

sales channel where customers can compare prices before

travelling. (GulfBase.com)

DW reaches deal with creditors on $14.6bn debt – Dubai

World (DW) has reached a deal with a majority of its creditor

banks to amend and extend terms on debt worth about $14.6bn.

DW said the deal with lenders includes early repayment of 2015

maturities totaling $2.92bn and the extension of 2018 maturities

to 2022. DW said it would use a special law, ‘Decree 57’, issued

to help government-related companies push through debt

restructurings following the financial crisis, to process the new

extension and amendment. To use the law, companies must

have an approval from at least two thirds of creditors by value.

(WSJ)

Nakheel, E&V to set up JV realty firm – Dubai-based real

estate developer Nakheel has signed a JV agreement with

Engel & Völkers (E&V), a Germany-based real estate brokerage

firm to create a new company specializing in selling and leasing

properties in Dubai. The agreement follows a letter of intent

signed between the two companies in 2014, which seeks global

opportunities by bringing together Nakheel’s Dubai real estate

expertise and E&V’s long-standing international brokerage

experience and network. The new company will operate under

the E&V brand. (Bloomberg)

UAB opens new branch in Dubai – United Arab Bank (UAB)

has opened its 12th branch in Dubai on Jumeirah Beach Road,

extending its branch network to 31 locations across the UAE.

Earlier in December 2014, UAB opened three new branches in

Dubai: the Business Bay branch located in Executive Towers,

the Media City branch at the Media City Tram Station and the

TECOM branch, located in the Grosvenor Business Tower.

(Gulf-Base.com)

CEO: Marka to turn profitable in 4Q2015 – Dubai-based retail

operator Marka’s CEO Nick Peel said that the company expects

to turn profitable in 4Q2015. Peel also said the firm was looking

at new acquisitions. He said that the company was also looking

at four asset purchases in the food & beverage sector. (Reuters)

NBAD hires Head of Debt Origination for South East Asia –

The National Bank of Abu Dhabi (NBAD) has hired Wynce Low

as a new Head of Debt Origination for South East Asia. Wynce

Low will be based in Kuala Lumpur, Malaysia and will be

responsible for the origination and distribution of conventional

and Islamic debt products in the area. He was previously head

of debt capital markets for HSBC in Malaysia. (Reuters)

AIB soft launches branch in Salalah – Alizz Islamic Bank

(AIB) announced the soft launch of its branch in Salalah, Oman.

The launch is part of the AIB’s s strategic initiatives to reach new

customers with innovative and value added products and

services. (GulfBase.com)

Ooredoo Oman signs 17 MoUs with government entities in

2014 – Omani Qatari Telecommunications Company (Ooredoo

Oman) has signed and completed 17 MoUs with a group of

ministries and government entities in 2014. The company

worked with the Ministry of Civil Service on the development of

5. Page 5 of 6

several training programs and workshops, while also working

with the Ministry of Awqaf & Religious Affairs and the Ministry of

Social Development on programs such as Istiqrar. Other

agreements included the Public Authority for Craft Industries,

the Oman Establishment for Press, Publishing & Advertising,

and the General Union of Workers of the Sultanate of Oman.

(Bloomberg)

ORC: Center of excellence for railway sector in Oman soon

– Oman Railway Company (ORC) said that a major center of

excellence catering to the emerging requirements of

professionals in railway sector will be formed in the country

soon. The new center, which is being formed by ORC, is aimed

at ensuring high standards among professional colleges and

vocational training institutes for training professionals for the

railway sector. (Bloomberg)

Oman's oil production rises in December – Oman's Ministry

of Oil & Gas said that the Sultanate's crude oil and condensate

production registered an increase in December 2014 by 1.15%

on a MoM basis, amounting to 28.9mn barrels, with an average

of 932,096 barrels a day (bpd). The Ministry added that the total

exported crude oil in December 2014 amounted to 24mn

barrels, an average of 774,189 bpd, which is decline of 3.45%

MoM. (Bloomberg)

Alba sales up 1.3% in 2014 – Aluminium Bahrain (Alba) said

that the sale of its products rose 1.3% in 2014 to reach 931,526

tons versus 919,722 tons in 2013. Production increased by 2.1%

to reach 931,427 tons versus 912,700 tons in 2013. Sales were

up 2% YoY to 242,322 tons in 4Q2014. Alba will release its full-

year and 4Q2014 financial results on February 9, 2015.

(GulfBase.com)

Armacell plans new manufacturing plant in Bahrain –

Armacell, a manufacturer of flexible insulation foams for the

equipment insulation market, announced that it will build a new

manufacturing facility in Bahrain. The new plant will produce

elastomeric rubber insulation for the heating, ventilating, and air

conditioning (HVAC) market in the GCC region, and will be

located at the Bahrain International Investment Park.

(GulfBase.com)

SLRB: 2014 real estate trading sets record in Bahrain – The

Survey & Land Registration Bureau’s (SLRB) President, Shaikh

Salman bin Abdulla Al Khalifa said the real estate trading in

Bahrain had recorded unprecedented figures of BHD1,292.5mn

in 2014. He said the 2014 figures represent a great leap in terms

of the trading volume estate in Bahrain, rising 50% as compared

to 2013. He added that the huge increase in figures have been

attained due to the royal reforms, with its fruitful results collected

through the progress witnessed in various fields, including real

estate across Bahrain. (Bloomberg)

Bahrain’s GDP growth reaches 5.1% in 3Q2014 – The

Bahrain Economic Development Board (EDB), in its latest

Bahrain Economic Quarterly (BEQ) report said the Kingdom's

GDP growth reached 5.1% YoY in 3Q2014, which continues the

momentum from earlier quarters. Overall growth is forecasted to

have been in excess of 4% in 2014, which reflects the positive

impact of the initiation of a number of significant infrastructure

projects. The BEQ also highlights the resilience of Bahrain's

non-oil growth. This was particularly apparent in the construction

sector, which experienced acceleration from 3.6% annual

growth in 2Q2014 to 12.3% in 3Q2014, making it the fastest

growing sector of the economy. The hotels & restaurants sector

also posted strong YoY growth of 7.4%. The hydrocarbons

sector in Bahrain has continued to expand throughout the year,

with a 4.7% YoY gain in 3Q2014. (Zawya)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only.

It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this

report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make

any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (

#

Market closed on 13 January 2015) Source: Bloomberg (*$ adjusted returns;

#

Market closed on 13 January 2015)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

QSE Index S&P Pan Arab S&P GCC

(0.1%)

(0.9%)

(0.0%)

0.3%

0.6%

(0.7%) (0.7%)

(1.0%)

(0.6%)

(0.2%)

0.2%

0.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,233.26 0.9 0.9 4.1 MSCI World Index 1,676.71 (0.4) (0.4) (1.9)

Silver/Ounce 16.58 0.5 0.5 5.6 DJ Industrial 17,640.84 (0.5) (0.5) (1.0)

Crude Oil (Brent)/Barrel (FM

Future)

47.43 (5.3) (5.3) (17.3) S&P 500 2,028.26 (0.8) (0.8) (1.5)

Crude Oil (WTI)/Barrel (FM

Future)

46.07 (4.7) (4.7) (13.5) NASDAQ 100 4,664.71 (0.8) (0.8) (1.5)

Natural Gas (Henry

Hub)/MMBtu

2.90 (1.9) (1.9) (3.3) STOXX 600 339.87 0.5 0.5 (3.0)

LPG Propane (Arab Gulf)/Ton#

45.25 0.0 0.0 (7.7) DAX 9,781.90 1.3 1.3 (3.0)

LPG Butane (Arab Gulf)/Ton 62.88 0.2 0.2 0.2 FTSE 100 6,501.42 0.1 0.1 (3.6)

Euro 1.18 (0.1) (0.1) (2.2) CAC 40 4,228.24 1.1 1.1 (3.3)

Yen 118.35 (0.1) (0.1) (1.2) Nikkei#

17,197.73 0.0 0.0 (0.7)

GBP 1.52 0.1 0.1 (2.6) MSCI EM 955.53 (0.6) (0.6) (0.1)

CHF 0.99 (0.1) (0.1) (2.0) SHANGHAI SE Composite 3,229.32 (1.6) (1.6) (0.1)

AUD 0.82 (0.6) (0.6) (0.2) HANG SENG 24,026.46 0.5 0.5 1.8

USD Index 91.98 0.1 0.1 1.9 BSE SENSEX 27,585.27 0.5 0.5 2.2

RUB 63.14 1.8 1.8 4.0 Bovespa 48,139.74 (2.2) (2.2) (4.3)

BRL 0.38 (1.1) (1.1) (0.6) RTS 756.63 (3.3) (3.3) (4.3)

171.2

132.4

121.3