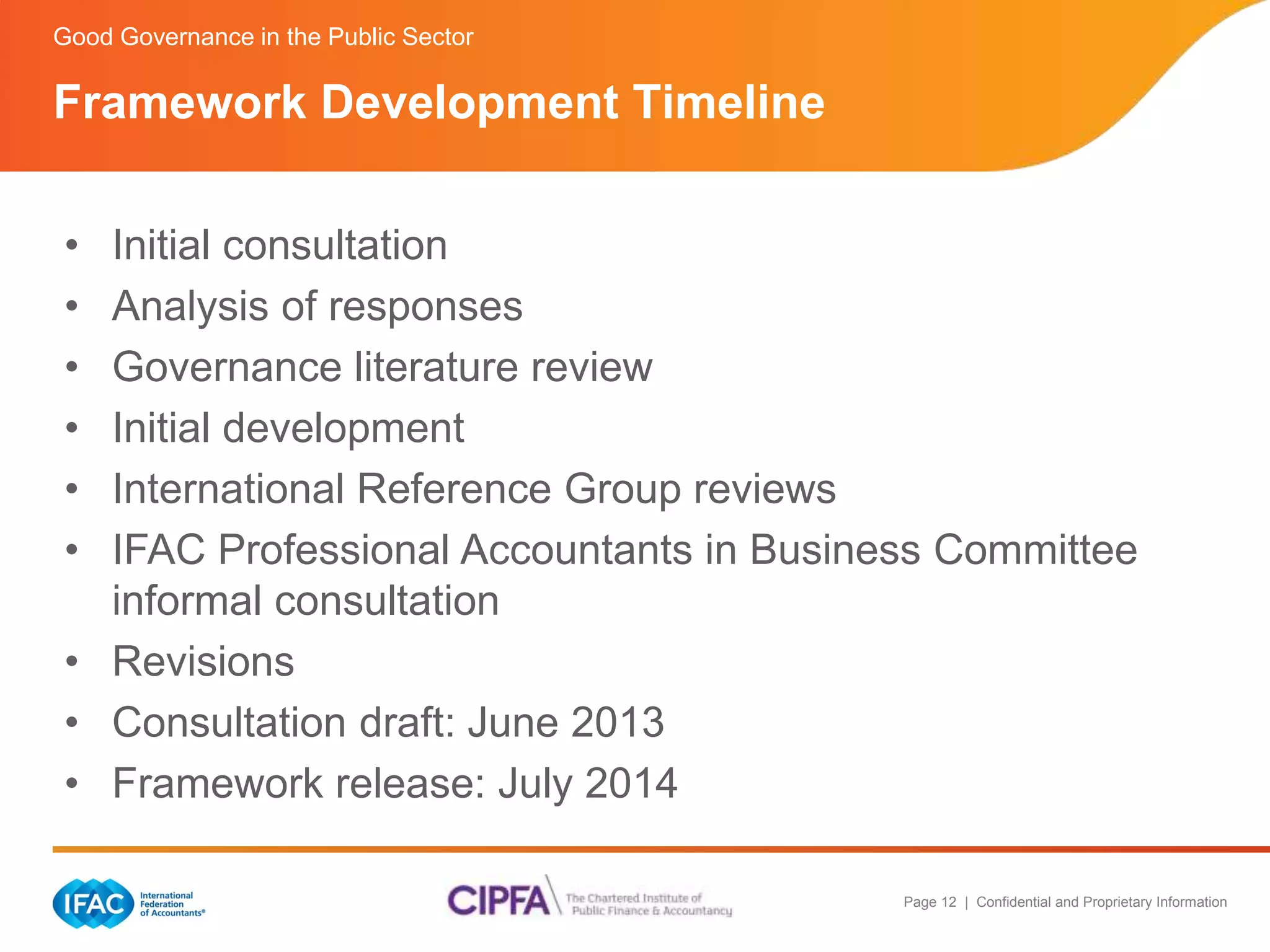

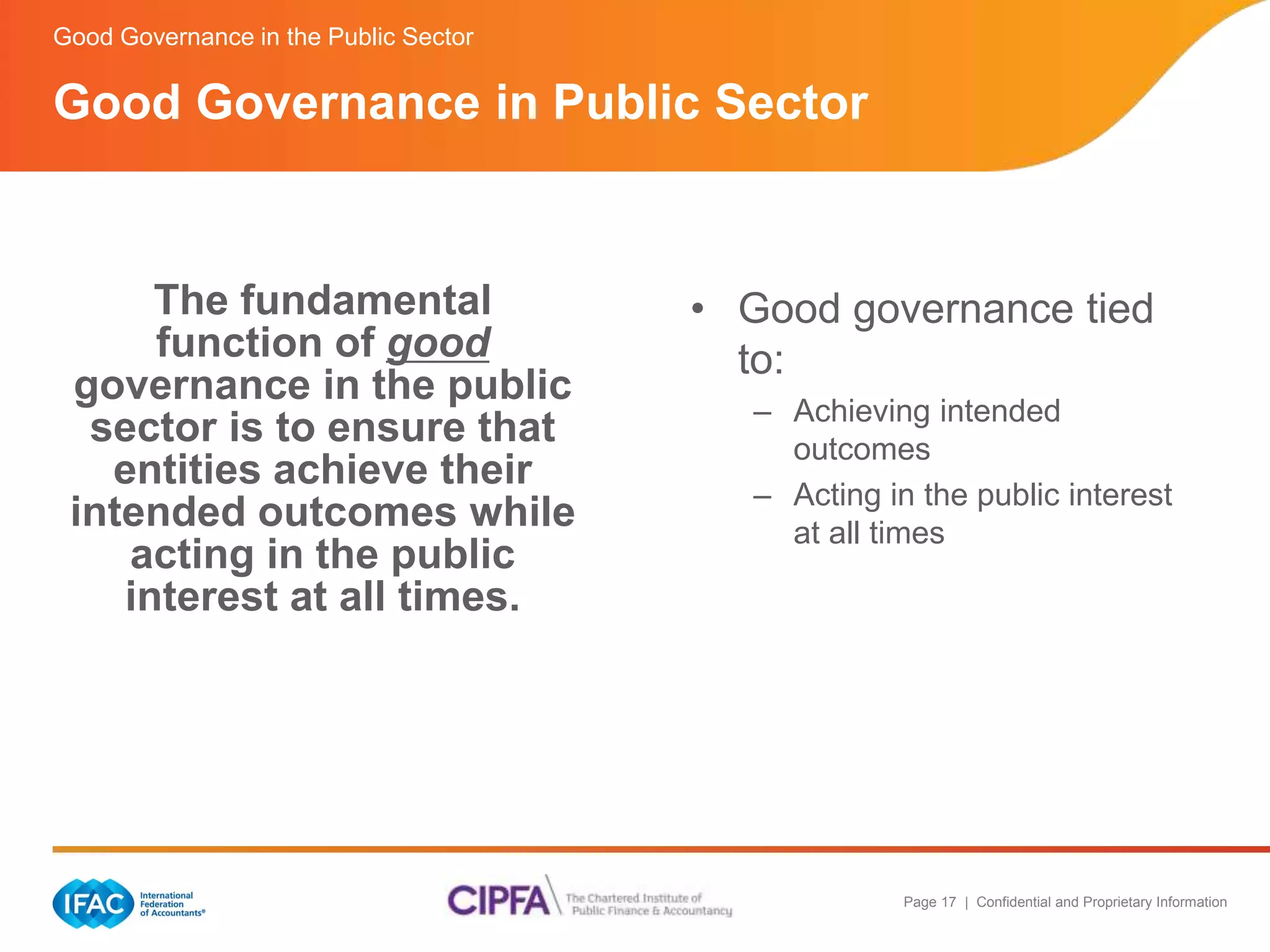

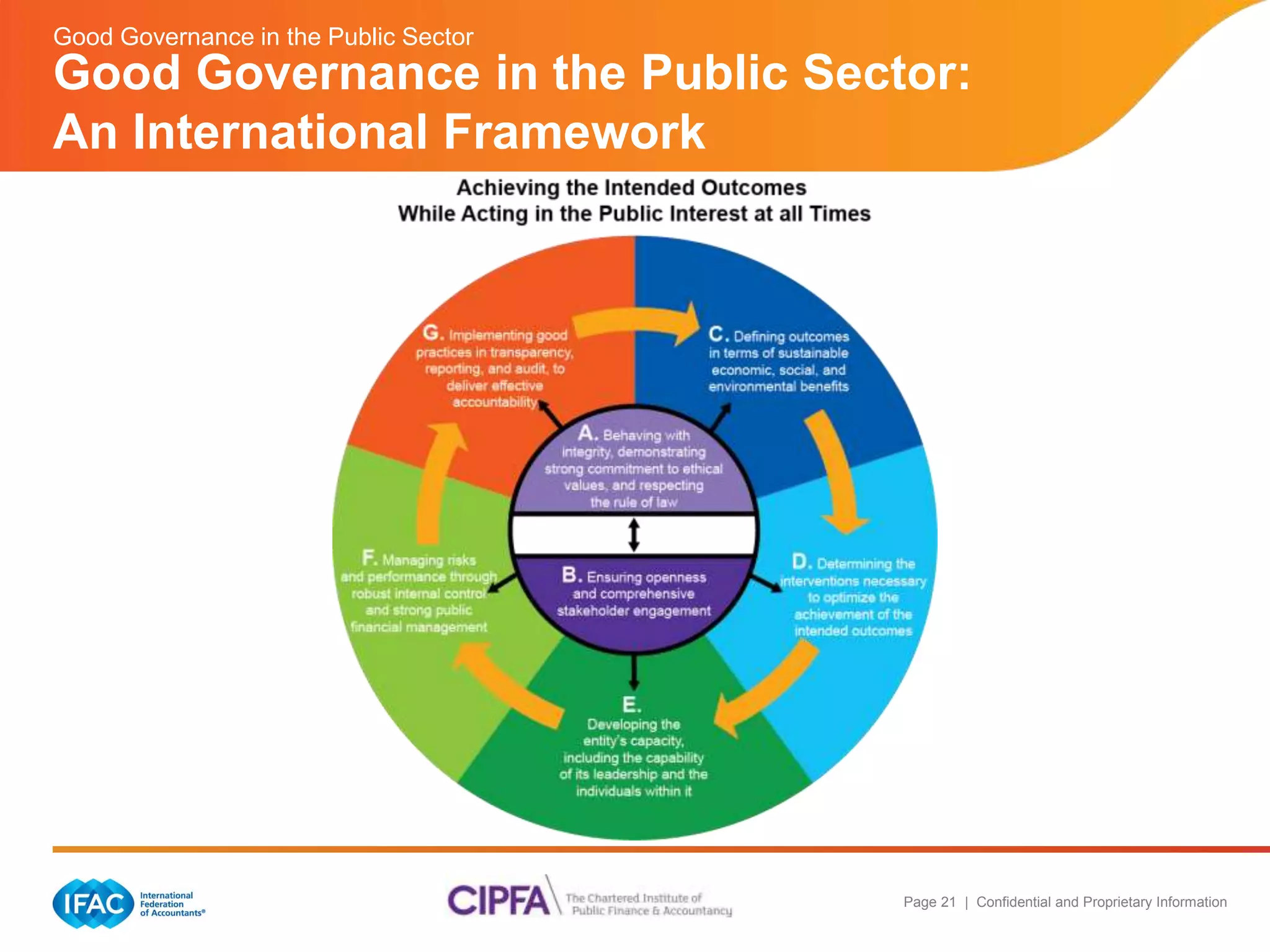

The document outlines the framework for good governance in the public sector developed by IFAC and CIPFA, emphasizing its significance in enhancing decision-making, resource use, and accountability. It discusses the characteristics of the public sector and challenges faced, proposing a benchmark for governance and presenting the principles necessary for achieving intended outcomes while acting in the public interest. The document also details the framework's development timeline and outlines principles such as integrity, stakeholder engagement, risk management, and transparency.