Healthcare Valuations in an Era of Reform and Uncertainty

CVS Health INITIATING COVERAGE REPORT

1. INITIATING COVERAGE REPORT Temple University Investment Association

The Fox Fund

October 25th

, 2016

Tyler McMahon: Lead Analyst

Tyler.mcmahon@temple.edu

Andrew Cutrona: Lead Analyst

Andrew.cutrona@temple.edu

Kevin Vo: Associate Analyst

Kevin.vo@temple.edu

Amine Aouom: Associate Analyst

Amine.aouom@temple.edu

COMPANY OVERVIEW

CVS Health Corp. is the leading health care retailer with over

9,600 stores in 49 states, including Washington D.C., Puerto

Rico, and Brazil. The company offers a broad selection of

pharmaceutical services and drugs (prescription and over-the-

counter), cosmetics, and other general merchandise, through its

convenient and smaller store size (between 10,000 to 13,000

square feet). The company derives its revenue into two

segments: Pharmacy Services (58.2% of FY 2015 revenue) and

Retail/LTC (41.8% of FY 2015 revenue). CVS Health Corp.

reports the end of its fiscal year on February 9th.

INVESTMENT THESIS

CVS Health is currently trading at a 18.21% discount to the

company’s average three-year forward P/E multiple of 16.8x.

CVS began trading at a discount when it reported declines in

earnings per share and downgraded EPS guidance in its Q1 and

Q2 of FY 2016. CVS is recognized as one of the most well-

known and profitable retail drug store chain in the United

States. CVS posted consecutive negative EPS growth in the

first two quarters of FY 2016 due to the acquisition related

costs associated with CVS Health’s acquisitions of Target

pharmacy’s and Omnicare. Even though top line growth

continued to grow at YoY rates of 19% and 17.6% respectfully,

CVS sold off 20.2% between February and October of FY

2016 as a result of YoY earnings declines of 2.8% and 23.2%

respectfully. Our sector believes that investors have

overreacted and CVS health, despite negative earnings growth,

it is as financially strong as it has ever been due to its

acquisitions of Target pharmacies and Omnicare assisted-living

and long-term-care facility. Analysts have overlooked the real

reasons for the EPS decline and the realized revenue growth

from the FY 2015 acquisitions along with the companies

MinuteClinic and Telehealth Initiatives, and the increasing

demand for prescription drugs will drive CVS back to its

average three-year forward P/E multiple of 16.8x. Using

consensus next twelve months earnings forecasts, our sector

arrived at our fair value estimate of $105, yielding a 21.2%

return.

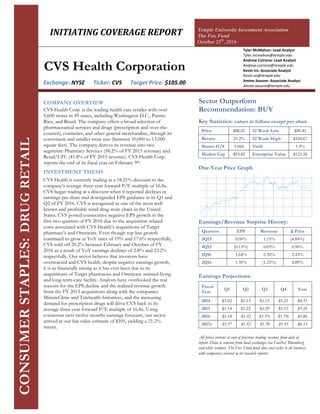

CONSUMERSTAPLES: DRUGRETAIL

CVS Health Corporation

Exchange: NYSE Ticker: CVS Target Price: $105.00

Sector Outperform

Recommendation: BUY

Key Statistics: values in billons except per share

Price $88.01 52 Week Low $85.41

Return 21.2% 52 Week High $106.67

Shares O/S 1.066 Yield 1.9%

Market Cap $93.82 Enterprise Value $121.26

One-Year Price Graph

Earnings/Revenue Surprise History:

Quarters EPS Revenue Δ Price

3Q15 0.00% 1.15% (4.84%)

4Q15 (0.13%) 0.05% 0.96%

1Q16 1.64% 0.50% 2.43%

2Q16 1.30% (1.25%) 4.89%

Earnings Projections:

Fiscal

Year

Q1 Q2 Q3 Q4 Year

2014 $1.02 $1.13 $1.15 $1.21 $4.51

2015 $1.14 $1.22 $1.29 $1.53 $5.18

2016 $1.18 $1.32 $1.57e $1.79e $5.86

2017e $1.37 $1.52 $1.70 $1.95 $6.53

All prices current at end of previous trading sessions from date of

report. Data is sourced from local exchanges via FactSet, Bloomberg

and other vendors. The Fox Fund fund does and seeks to do business

with companies covered in its research reports.

2. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 2

SEGMENTS OVERVIEW

Pharmacy Services

Revenue from the Pharmacy Services

segment accounted for 58.2% of the

total net revenue during FY 2015. CVS

Health generates most of its revenue

through a series of intermediary

operations with its clients known as

pharmacy benefit managers (PBM).

PBMs provide services including plan

design and administration, formulary

management, Medicare Part D services,

mail order, specialty pharmacy and other

miscellaneous provisions. Many of the

clients of CVS Health consist of

insurance companies, employers, unions,

public and private institutions, and so

forth. The Pharmacy Services segment

conducts most of its operations on dispensing prescription drugs through pharmacy network transactions and mail

choice. As of the FY 2015 filing, pharmacy network claims increased by 9% from 8.49 million in FY 2014 to a total of

926.2 million. Mail choice claims also grew 4% from 82.4 million in FY 2014 to a total of 85.7 million. The rising

number of claims from the pharmacy network and mail choice operations contributed to an increase of total net revenue

and operating profit from FY 2014.

Retail/LTC

The Retail/LTC segment includes over 9,600 retail stores, healthcare clinics, and online retail pharmacy services. The

segment makes up 41.8% of the total net revenue in FY 2015. CVS Health generates this portion of revenue from selling

prescription drugs and other wide assortment of general merchandise, including over-the-counter drugs, beauty products

and cosmetics, personal care, convenience foods, photo finishing, and other miscellaneous items. The Retail/LTC

segment also conducts its operations on pharmaceutical distributions, pharmacy consulting, chronic care ancillary

services, commercialization, and CVS MinuteClinic offerings. MinuteClinics are services staffed by nurse practitioners

and physician assistants taking on protocols to perform health screenings, diagnose and monitor health conditions, and

distribute vaccinations.

INDUSTRY OVERVIEW

Discretionary Spending

Consumer spending metrics in the U.S. retains its strength throughout FY 2016 despite economic slowdowns overseas.

The consumer confidence index has risen to 104.1 in September, an increase from 101.4 in the prior month. Disposable

personal income has grown 3.4% in August of FY 2016, with the growth of consumer spending at 4.4% year by year,

annual GDP growth at 1.4%, and unemployment lowering at 4.0%. This reflects stronger economic growth due to

higher income levels and rising job growth, an indication for rising consumer spending levels. The Retail/LTC segment

comprises 41.2% of CVS Health’s total net revenue in FY 2015. Thus, the growth in consumer confidence, disposable

income, and consumer spending, can help the company accumulate more net revenue and operating profit going

forward in FY 2016.

Health Care

The sales of prescription drugs and medical services consist a majority of net revenue generated from the company’s

Pharmacy Services sector. More people are currently living longer as they age, and are demanding more for prescription

drugs and medical care. Gross sales for pharmaceuticals have reached $132.4 billion in FY 2015 and is forecasted to

grow at 7.8% in FY 2016, with sales estimated to reach at $143.5 billion. However, one of the presidential candidates of

the 2016 U.S. election have announced further regulations on prescription drug pricing, in response to the massive

5000% price hike of Daraprim by Turing Pharmaceuticals. If the candidate were to win the election, uncertainties will

loom upon the trajectory of pharmaceutical sales and growth throughout FY 2016.

3. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 3

CATALYSTS

MinuteClinics

MinuteClinics are small walk-in retail health clinics

within the CVS Caremark pharmacy stores which utilize

nationally recognized protocols to diagnose and treat

minor health conditions, perform health screenings,

monitor chronic conditions and dispense vaccinations at

much lower prices than a hospital. It is usually staffed

with advanced degree nurses known as nurse

practitioners who treat routine maladies. Thanks to the

recent closing of the $1.9 billion acquisition of Target's

(NYSE:TGT) pharmacy

and clinic businesses, CVS

Health now counts more

than 9,500 retail stores in

its empire, with more than

1,100 of these stores also

offering walk-in medical

services under the MinuteClinic name. The Target deal

significantly expanded the company's footprint from the

7,800 retail stores and 900 clinics it owned at the end of

2014, and over the next two years the company plans on

adding another 400 MinuteClinics to its network.

Excluding the Target clinics acquired in the $1.9 billion

deal, CVS Health registered a 21% year-over-year

increase in revenue from MinuteClinics YoY between

FY2014 and FY2015, and achieved the full year 2015

revenue target of about $345 million. CVS Health’s

MinuteClinic remains the largest and fastest-growing

walk-in retail clinic operator in the country operating

about 52% of all the retail health clinics in the country.

As of today, 50% of the U.S. population actually lives

within 10 miles of a MinuteClinic, and CVS Health plans

to operate about 1,500 clinics by the end of 2017, with

30% of the expansion coming from new markets. The

trend toward the use of retail clinics is a response to a

number of factors that are shaping the healthcare

marketplace. With the Affordable Care Act, there are

millions of newly insured Americans seeking care,

placing stress on a system that already suffers from a

shortage of primary care physicians. In fact, that

shortage is expected to reach 45,000 doctors by 2020.

The United states aging population is another factor

increasing the need of retail clinics. Thousands of Baby

Boomers are reaching the age of 65 every day, and the

demand for health care services will only increase as they

continue to age. Finally, the national epidemics of

obesity, diabetes and other chronic illnesses mean that

more people need more care. Retail health clinics can

address all of these issues through their convenience,

affordability and the growing list of services offered for

both common acute and chronic illnesses. CVS looks

poised to take advantage of these trends and

MinuteClinic revenue will increase exponentially.

MOATS

Sourcing Advantage: The company has a strong wide

moat, given its sourcing advantage. CVS Health's wide

moat stems from its large claim volume, allowing the

company to leverage in managing drug pricing, which in

turn helps drive additional contracts for benefits

management. The company derives a return on equity of

close to 13%, slightly below the minimum requirement for

inclusion in the dividend portfolio. Nonetheless the return

on equity has been steadily improving in recent years and it

expected this to continue higher. CVS Health' dividend has

shown consistent increases over the last 10 years, satisfying

the need for dividend growth consistency. While it’s

preferable the dividend yield to be higher, the dividend

exceeds minimum threshold for inclusion. The company

thus met most of criteria for inclusion with its dividend

accumulation portfolio.

RISKS

Discretionary Spending: The company can face a greater

amount of systematic risk based on the trajectory of its

revenue and profits being tied to consumer discretionary

spending. In the first quarter of 2016, CVS Health

exhibited strong financial results. However, that hasn’t

translated to share price gains for the company due to the

stagnation of the share price of FY 2016. There are three

main reason that may affect the stock price for the

company. The first risk highlights a weak spot in the

second quarter in drug revenue. Stealth reported solid year-

over-year growth in its pharmacy benefits management

business, but the increase stemmed primarily from the

acquisition of pharmacy services company, Omnicare.

Second quarter revenue for the segment actually came in

below the company’s expectations. The main culprit was a

decline in hepatitis C prescription volume. Furthermore,

given that the Omnicare deal closed in August 2015, CVS

Health won’t be able to rely on that acquisition to produce

attractive year-over-year comparisons much longer.

Margin Contraction: The gross profit margin fell from

5.1% to 4.6% year over year, while operating declined from

3.8% to 3.5%. In the Retail/LTC segment, gross margin

has dropped from 30.9% to 29.2% year over year, and

operating margin decreased from 9.7% to 8.5%. In other

words, costs are accelerating higher than sales. So far, the

declining margins haven’t worried any investors. However,

a sustained negative trend could ultimately take a roll on

CVS Health’s share.

Macro Environment: The third risk is the

macroeconomic woes on qualitative risk factors, this

includes the change in the economic and financial

conditions of the country, which will have a direct impact

on sales and revenue for the company.

4. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 4

Omnicare and Target Acquisitions

CVS Health acquired Omnicare for $13 billion in

August of 2015 and acquired all of Target’s

pharmacies for $1.9 billion in December of 2015.

Omnicare is a leading provider of pharmacy services

to both the assisted-living and long-term-care facility

markets. The Omnicare acquisition has significantly

expanded its ability to dispense prescriptions in

assisted living and long-term care facilities that

serve the senior patient population. The acquisition

should prove to be a significant growth opportunity

over the coming years as the graying of the

American population continues. CVS Health

acquired Target’s more than 1,660 pharmacies across 47 states and will operate them through a store-within-a-store

format, branded as CVS/pharmacy. CVS Health pharmacies will be included in all new Target stores that offer

pharmacy services. Thus, as Target continues to expand, CVS will continue to expand its pharmacies as well. In addition,

CVS Health and Target plan to develop five to ten small, flexible format stores over a two-year period following the deal

close, which will each be branded as TargetExpress and include a CVS Health pharmacy. These two acquisitions created

an expected rise in revenue of about 13% and are now becoming fully integrated and will continue to boost both top

and bottom line revenues while geographically expanding its footprint across the US particularly in the Pacific

Northwest via the Target acquisition where CVS Health has limited operations. The financial and operational returns on

investment of these acquisitions have not yet been fully felt due to the costs related to the 2015 acquisitions of Omnicare

and Target pharmacies. The biggest factors were paying off $542 million of debt early, $114 million more in interest

expense during the second quarter of 2016 versus the same quarter last year due to the issuance of debt to fund its

acquisitions of Target's pharmacies and clinics, as well as Omnicare, and CVS Health reported $81 million more in

integration costs related to these acquisitions. The Target integration activities are well underway and the remaining store

conversions expected to be completed by the end of this month.

Telehealth Incentive

CVS Health plans to enter the telehealth business because of an expected increase in patient demand for healthcare in

coming years. The company’s Telehealth incentive will provide patients with further access to doctors and will be able to

provide consultations via the phone and web. CVS Health's online site will give direct access to online consultations with

a doctor. Telehealth video consultation sessions are projected to increase from 19.7 million in 2014 to 158.4 million per

year by 2020. With the increased demand for patient care anticipated in future years, as a result of the expansion of

coverage through the Affordable Care Act, the primary care physician shortage, aging of the population and epidemic of

chronic disease, telehealth gives CVS Health the opportunity to offer high quality care to an expanded group of patients

in a variety of convenient and cost-effective locations.

The drug retail industry

The drug retail industry is expected to benefit from favorable long-term trends that include an aging population, a strong

drug pipeline, expanded healthcare coverage for Medicare participants, and millions of newly insured Americans seeking

care. New drugs are entering the market every year, and the average price for new drugs continues to rise. Growth of

prescription drugs spending is estimated to have increased 8.1% in 2015 to $321.9 billion. It is estimated that

prescription drug spending will have an average annual growth of 6.7% from 2016 to 2025, due to the continued effect

of newly approved and expensive drugs for the treatment of hepatitis C and cancer. The aging population is an

important trend, as prescription drug expenditures are highest for people aged 65 and older. In March 2016, the US

Census Bureau reported that the population aged 65 and older is projected double by 2050. Pharmacies are experiencing

an increase in demand from this aging US population. The elderly represented about 15% of the total population in

2015, and accounted for around 64% of all prescriptions written. The average annual number of prescriptions per

person increases significantly with age. Specifically, from 4.1 prescriptions for those aged 0 to 18, it increased to 16.2

prescriptions for 19- to 64-year-olds, and to 36.6 prescriptions for people aged 65 and older. The first Baby Boomers

turned 65 in 2011, and around 10,000 baby boomers turn 65 each day, CVS Health looks poised for significant growth in

the second half of 2016 and over the coming years.

5. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 5

FINANCIALS

Revenue

CVS Health derives its revenue from two

main segments: Pharmacy Services (58.0%

of FY 2015) and Retail/LTC (42.0%). Since

FY 2011, revenue has grown from $107.1

billion to $153.3 billion, illustrating a 9.4%

CAGR. Revenue in its pharmacy segment

increased by 13.5% YoY and net revenues in

its Retail/LTC segment increased 6.2%

YoY. Nearly 50% of the increase in the retail

segment was driven by the addition of long-

term care operations acquired as part of the

Omnicare acquisition. The company’s

revenue is anticipated to grow from $153.3

billion to 233.9 billion in FY 2019, at a

11.2% CAGR.

Pharmacy Services Segment (58.2%% of FY 2015 revenue)

Pharmacy Services revenue increased from $76.2 billion in FY 2013 to $100.4 million in FY 2015, illustrating a CAGR of

14.8%. Over the last fiscal year, the increase is primarily due to 11% growth in specialty pharmacy (Specialty Connect),

new clients, increased volume from new products and the addition of the specialty pharmacy operations of Omnicare.

Partially offsetting this growth was an increase in the generic dispensing rate, which grew approximately 165 basis points

year on year. CVS Health’s specialty pharmacy services continued to gain share in Q4 2015. Mail choice claims processed

increased 4% YoY to 85.7 million and revenue per mail choice increased by 17% also due to growth in specialty

pharmacy in 2015. Pharmacy network claims processed also increased 9% YoY to 926.2 million claims mostly due to net

new business. Our sector has forecasted revenue to grow 14.1%, 4 year CAGR for this segment.

Retail/LTC Segment (42.8% of FY 2015 revenue)

Revenue in Retail/LTC Segment grew from $63.7 billion in FY 2013 to $72.0 billion in FY 2015, representing a CAGR

of 6.3%. Approximately half of the increase was driven by the addition of long-term care operations acquired as part of

the $10 billion acquisition of Omnicare. Omnicare helps strengthen CVS Health’s position in the Retail/LTC segment as

well as the specialty pharmacy market. The acquisition of Omnicare boosted the revenue growth of the company by

6.3% in the second half of FY 2015 and equipped CVS Health with a new pharmacy dispensing channel, enhancing its

ability to provide the continuity of care for patients as they transition through the healthcare system. Another growth

driver was the acquisition of Target’s more than 1,600 pharmacy departments and 80 medical clinics makes CVS

Health’s network of pharmacies the largest among its competitors. The acquisition of Target increases the company’s

share of the total prescriptions filled in the U.S allowing the company to expand its retail presence into new markets.

Pharmacy same store sales rose 4.5% YoY primarily due to same script growth of 4.8%. Looking forward, our sector has

forecasted revenues to grow 7.1%, 4-year CAGR because of an increase of prescription drugs due to the Omnicare and

Target acquisitions.

Margins

The retail pharmacy chain and pharmacy benefit management businesses do not typically see high gross or net profit

margins. However, these businesses are consistent and predictable allowing for high rates of growth. From FY 2014 to

FY 2015, gross margins slightly weakened from 18.2% to 17.3%. Operating margins decreased from 5.9% in the first

half of FY 2014 to 5.2%. The drop in margins was mainly due to the major acquisitions of Target pharmaceutical

business as well as Omnicare. The integration costs related to the acquisitions inflated the company's operating expenses

by over $100 million. Excluding the acquisition and integration expenses, the company's operating profit increased 6.5%

over the prior year quarter (Q2). Once CVS Health exploits the synergies of these acquisitions, it will improve overall

margins. The decline in gross margin was also due to continued reimbursement pressures. Gross margin was positively

impacted by the increase in GDR, as well as increased front store margins due to our continued rationalization of

promotional strategies and improved mix of the products that the company sold.

6. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 6

Earnings

CVS Health has missed earning in Q1 and Q2 on FY 2016.

Although the official earnings numbers reflected a decrease from

the prior-year-periods, the news was not surprising or that

concerning. The negative comparisons stemmed from the costs

related to the acquisitions of Omnicare and Target’s in-store

pharmacies and clinics that took place in December of 2015. As

mentioned before, besides paying $542 million of debt and $114

million in interest expense during Q2 of FY 2016 compared to

Q2 of FY 2015, the company reported $81 million more in

integration costs related to these acquisitions. On a positive note,

non-GAAP earnings per share grew from $1.32 from $1.22 in the

prior year period, which exceeded investors’ expectations. Prior to Q1 & Q2 of FY 2016, CVS Health has surpassed

earnings expectations 17 out of last 18 periods with an average earnings surprise of 15.92%. Our sector has forecasted

EPS of $5.08 in FY 2016 (9.7% YoY growth) and $6.18 in FY 2017 (21.7% YoY growth). CVS Health has shown the

ability to consistently grow earnings and we are very bullish that the company will continue to do so going forward as it

continues to expand and see success in both of its segments.

Cash Flows

CVS reported cash flow from operations of $9.41 billion and free cash flow of $6.89 billion of in FY 2016. In FY 2015,

cash flow from operations and free cash flow of $8.41 billion and $6.05 billion respectively. This positive growth is due

to The impact by the Medicare Part D benefit design and changes in the composition of CVS membership. The

Medicare Part D standard benefit design results in coverage that varies with a member's cumulative annual out-of-pocket

costs. As a result, the PDP plan pay percentage or benefit ratio generally decreases and operating profit generally

increases as the year progresses. Cash flow from operating is forecasted to grow at an 9.14 % CAGR between FY 2015

and FY 2018. Free cash flow is forecasted to grow at a CAGR OF 13.74 % through FY 2018. CVS Target's 1,672

pharmacies across 47 states and will operate them through a store-within-a-store format, branded as CVS Pharmacy and

expect to open up to 20 new clinics in Target stores within the next three years. That’s drive cash flow from operations

higher

Shareholder Return

Pharmacy chains have outperformed the broader S&P 500 index in 2015. The stock for CVS Health has provided total

returns of 15.1% year-to-date. In comparison, peers Walgreens Boots Alliance, Rite Aid, and Diplomat Pharmacy have

provided returns of 24.9%, 14.2%, and 66.8% year-to-date. The S&P 500 Index and the S&P 500 Food and Staples

Retailing Index have provided returns of 1.6% and 3.5%, respectively, through July 27. CVS Health, Walgreens Boots

Alliance, and Rite Aid together constitute ~3% of the portfolio holdings of the SPDR S&P Retail ETF. CVS and

Walgreens Boots Alliance together constitute ~1.7% of the portfolio holdings of the iShares S&P 100 ETF.

Debt

CVS has a higher debt to equity ratio than Walgreens. In the last 5 years CVS debt ratio and debt to equity ratio has

increased while Walgreens has stayed the same. CVS took on more debt because they needed to buy more property and

plants. Walgreens has doubled CVS in plants and property thus CVS is taking more debt to reach Walgreens.

7. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 7

VALUATION

Peer Group Analysis

Walgreens is a pharmaceutical retailer that offers prescription drugs, health and wellness products, health information

and photo services. The company operates three segments: Retail Pharmacy USA (71.4% of FY 2015 sales),

Pharmaceutical Wholesale (17.3% of FY 2015), and Retail Pharmacy International (11.3% FY 2015). Walgreen’s Retail

Pharmacy USA segment is the most comparable to CVS’s Retail/LTC segment, generating a higher revenue of $83.8

billion versus CVS Health’s $72.0 billion. Walgreens generated only $117.4 billion in net revenue compared to CVS

Health net revenue, derived from its two segments, of $153.3 billion in FY 2015.

Rite Aid is a drugstore chain retailer that operates 4,553 stores in all 50 states. As of FY 2016, Rite Aid generated a total

of $30.7 billion in net revenue, an increase of 15.9% from $26.5 billion in the prior year. Most of the revenue is

generated from Rite Aid’s Retail Pharmacy segment, constituting 87.4% in net revenue of FY 2016. The company

recently opened a new segment in Pharmacy Services, in comparison to CVS Health’s PBM operations. In October

2015, Rite Aid accepted a merger agreement from Walgreens, which is currently pending approval from governmental

regulators and its shareholders.

Undervaluation

CVS Health is currently trading at 18.21% discount to the company’s average three-year forward P/E multiple of 16.8x,

and a 6.67% discount to its average three-year historic EV/EBITDA multiple of 12.6x. Despite surpassing top line

expectations, CVS Health began trading at discount after it missed earnings projections in Q1 FY 2016. The earnings

reflected a negative YoY growth of 2.7% which was the direct result of costs related to the 2015 acquisitions of

Omnicare and Target's in-store pharmacies and clinics. The company also lowered its GAAP earnings guidance to $5.24

to $5.39 per diluted share from $5.28 to $5.43 per diluted share which contributed to the selloff. This subpar news

caused traders to sell off CVS Health 14.14% after the Q1 earnings call (P/E multiple from 21.8x to 18.8x). After a

quick price rebound in the days leading up to Q2 FY 2016 earnings call, traders once again started selling off the stock

following another earnings miss. The earnings miss reflected a negative YoY growth of 23.2% that resulted from paying

off $542 million of debt early, $114 million more in interest expense during the second quarter of 2016 versus the same

quarter last year due to the issuance of debt to fund its acquisitions of Target's pharmacies and Omnicare, and $81

million more in integration costs related to these acquisitions. Based on its second-quarter results, CVS Health also

revised guidance for full-year GAAP earnings per share to $4.92 to $5.00 from $5.24 to $5.39. This negative change

caused traders to sell off CVS Health 12.1% after the Q2 earnings call (P/E multiple from 19.8x to 17.4.8x). We believe

that management will continue to alleviate investors’ concerns over consecutive negative earnings growth after the Q3

conference call (November 8th) by proving strong revenue and earnings growth showing that the original selloff was

overblown and due to acquisitions related costs and that future growth prospects are not in jeopardy. The combination

of our valuation methodologies, strong Q3 earning results, and continued attractive top-line growth solidifies our

opinion that CVS is a value opportunity with favorable growth prospects.

Fair Value Calculations

To calculate a fair target price, we used two different valuation multiples/methodologies to see the various ranges of

target prices. Our sector calculated our fair value estimates using forward P/E and historical EV/EBITDA multiples.

Using consensus NTM EPS of $6.25 estimates with an average three-year forward P/E multiple of 16.8x we calculated a

fair value estimate of $105. Using consensus LTM EBITDA estimates of $12,386 million with an average one-year

historical EV/EBITDA multiple of 11.3x we calculated the fair value estimate of $98. Our sector decided to derive our

target price using the company’s average three-year forward P/E multiple of 16.8x, which calculates a fair value of $105,

implying CVS Health is trading 18.21% below its intrinsic value.

8. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 8

APPENDIX

Exhibit I: Three-year price graph

Exhibit II: Three-year historical and forward P/E

9. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 9

Exhibit III: Three-year historical and forward EV/EBITDA

10. Fall, 2016

T e m p l e U n i v e r s i t y I n v e s t m e n t A s s o c i a t i o n : T h e F o x F u n d Page 10

DISCLAIMER

This report is prepared strictly for educational purposes and should not be used as an actual investment guide.

The forward looking statements contained within are simply the author’s opinions. The writer does not own any

CVS Health Corporation stock.

TUIA STATEMENT

Established in honor of Professor William C. Dunkelberg, former Dean of the Fox School of Business, for his

tireless dedication to educating students in “real-world” principles of economics and business, the William C.

Dunkelberg (WCD) Owl Fund will ensure that future generations of students have exposure to a challenging,

practical learning experience. Managed by Fox School of Business graduate and undergraduate students with

oversight from its Board of Directors, the WCD Owl Fund’s goals are threefold:

• Provide students with hands-on investment management experience

• Enable students to work in a team-based setting in consultation with investment professionals.

• Connect student participants with nationally recognized money managers and financial institutions

Earnings from the fund will be reinvested net of fund expenses, which are primarily trading and auditing costs

and partial scholarships for student participants.