Credit Suisse 20100614 china property policy outlook 1

1. 14 June 2010

Asia Pacific/China

Equity Research

Real Estate

China Property Policy Outlook: 1

Research Analysts

THEME

Jinsong Du

852 2101 6589

jinsong.du@credit-suisse.com

Property tax: would it crash the market?

Raymond Cheng, CFA

852 2101 6945

raymond.cheng@credit-suisse.com

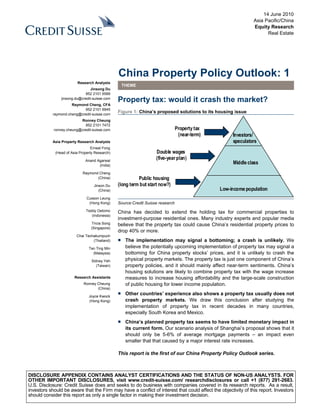

Figure 1: China’s proposed solutions to its housing issue

Ronney Cheung

852 2101 7472

ronney.cheung@credit-suisse.com Property tax

(near-term) Investors/

Asia Property Research Analysts speculators

Ernest Fong

(Head of Asia Property Research) Double wages

Anand Agarwal

(five-year plan)

(India)

Middle class

Raymond Cheng

(China) Public housing

Jinson Du (long term but start now?)

(China) Low-income population

Cusson Leung

(Hong Kong) Source:Credit Suisse research

Teddy Oetomo China has decided to extend the holding tax for commercial properties to

(Indonesia)

investment-purpose residential ones. Many industry experts and popular media

Tricia Song believe that the property tax could cause China’s residential property prices to

(Singapore)

drop 40% or more.

Chai Techakumpuch

(Thailand) ■ The implementation may signal a bottoming; a crash is unlikely. We

Tan Ting Min believe the potentially upcoming implementation of property tax may signal a

(Malaysia) bottoming for China property stocks’ prices, and it is unlikely to crash the

Sidney Yeh physical property markets. The property tax is just one component of China’s

(Taiwan) property policies, and it should mainly affect near-term sentiments. China’s

housing solutions are likely to combine property tax with the wage increase

Research Assistants measures to increase housing affordability and the large-scale construction

Ronney Cheung of public housing for lower income population.

(China)

Joyce Kwock

■ Other countries’ experience also shows a property tax usually does not

(Hong Kong) crash property markets. We draw this conclusion after studying the

implementation of property tax in recent decades in many countries,

especially South Korea and Mexico.

■ China’s planned property tax seems to have limited monetary impact in

its current form. Our scenario analysis of Shanghai’s proposal shows that it

should only be 5-6% of average mortgage payments – an impact even

smaller that that caused by a major interest rate increases.

This report is the first of our China Property Policy Outlook series.

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. FOR

OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/ researchdisclosures or call +1 (877) 291-2683.

U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result,

investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only a single factor in making their investment decision.

2. 14 June 2010

Focus charts

Figure 2: Relative performance (%) of Credit Suisse China Property indice performance vs MSCI China (1 March to

current) – property tax has been the key factor

(%)

5 24th Mar : Chongqing government announced its has s ubmitted its proposal of the implementation of property tax

0

12th May : Media reported that Shanghai

government is in the progress of drafting the

-5

property tax proposal - details include the

possibility of property tax to be levied at 0. 8% p. a

-10

-15 8th Apr il : Rumour that property tax

will be firs tly implemented in the 4 first tier cities

17th April : State Council iss ued 10 tightening

-20 17th May: An assistant manager of NDRC cit ed that

measures but no mentioning of the property t ax was in plac e.

property tax will not be implemented at least in 3 yr's time

-25 24th May : NDRC refuted the c omment above

Mar 10 Mar 10 Mar 10 Mar 10 Mar 10 Apr 10 Apr 10 A pr 10 Apr 10 May 10 May 10 May 10 May 10 May 10 Jun 10

CS China P roperty Share Price Index (rebased)

Source: Datastream; Credit Suisse research

Figure 3: South Korea – price index before and after Figure 4: Mexico – property price index before and after

implementation of property tax implementation of property tax

De c 08 = 100 (Peso/sqm)

12 0

12,000

10 0 11,000

Property tax 10,000

first introduced

introduced

80 9,000

8,000

60 7,000

6,000

40 5,000

Property tax

revised 4,000 Property tax first introduced

20 3,000

2,000

0 1994 1996 1998 2000 2002 2004 2006 2008

Ja n- 8 8

Ja n- 9 1

J an- 9 2

Ja n- 9 5

Ja n -9 9

Ja n-0 3

Ja n-0 6

Ja n-1 0

Jan - 86

Jan - 87

Jan - 89

Jan - 90

Jan - 93

Jan - 94

Jan -96

Jan -97

Jan -98

Jan -00

Jan -01

Jan -02

Jan -04

Jan -05

Jan -07

Jan -08

Jan -09

Source: Government websites Source: Government websites

Figure 5: Valuation summary – China developers

Share Target +/- Mkt Current (Disc)/ +12M (Disc)/ Yield P/B Net

Price Price Cap NAV Prem NAV Prem Core PE (x) (%) (x) Gearing

Company RIC Rating (HK$) (HK$) (%) (US$b) (HK$/sh) (%) (HK$/sh) (%) FY09 FY10 FY11 FY09 FY10 FY10 (%)

China developers

China Overseas Land 0688.HK O 14.60 17.70 21 15.3 16.88 (14) 19.68 (26) 15.9 15.4 13.4 1.4 2.5 59.5

China Resources Land 1109.HK O 14.50 17.00 17 9.4 21.66 (33) 24.29 (40) 22.5 15.2 12.2 1.6 1.9 44.5

China Vanke - A (Rmb) 000002.SZ O 7.15 9.50 33 10.1 8.50 (16) 10.50 (32) 14.8 11.0 10.7 1.0 2.2 34.6

China Vanke - B 200002.SZ O 7.53 7.90 5 1.3 9.66 (22) 11.93 (37) 13.7 10.1 9.9 0.9 2.0 34.6

Evergrande 3333.HK N 2.39 2.40 0 4.6 5.97 (60) 6.09 (61) 137.1 4.4 4.1 0.1 0.6 20.4

Greentown 3900.HK U 8.35 8.30 (1) 1.6 15.95 (48) 16.62 (50) 15.6 9.1 6.9 3.6 1.2 169.1

Guangzhou R&F 2777.HK N 9.88 9.80 (1) 4.1 15.80 (37) 17.80 (44) 11.1 7.7 6.8 4.1 1.4 109.7

Hopson 0754.HK N 8.93 9.90 11 1.7 22.00 (59) 24.80 (64) 5.3 4.7 3.6 2.8 0.5 42.0

Kaisa 1638.HK O 1.59 2.10 32 1.0 4.90 (68) 5.30 (70) 16.8 5.0 8.3 n.a 1.1 58.9

KWG 1813.HK O 4.43 5.90 33 1.6 10.10 (56) 10.70 (59) 14.6 8.6 7.4 1.1 1.0 70.2

Poly (A) 600048.SS O 11.05 17.30 57 6.5 16.70 (34) 19.20 (42) 10.4 10.6 8.0 1.4 1.4 66.5

Poly (Hong Kong) 0119.HK O 7.27 9.90 36 3.0 12.20 (40) 14.10 (48) 25.2 19.6 13.5 0.6 1.2 52.9

Shimao Property 0813.HK O 11.80 14.10 19 5.4 17.66 (33) 20.20 (42) 13.4 9.5 8.5 2.5 1.5 78.5

Sino Ocean 3377.HK O 5.67 8.00 41 4.1 9.60 (41) 11.44 (50) 21.4 12.1 10.6 1.4 1.1 45.1

th

Source: Prices are as of 10 Jun, Bloomberg;Company data, Credit Suisse estimates

China Property Policy Outlook: 1 2

3. 14 June 2010

Property tax: would it crash the

market?

China has decided to extend the holding tax for commercial properties to investment- China has decided to extend

purpose residential ones, to avoid legislation issues for implementing a new property tax. the holding tax for

Several industry experts, including those that we brought to meet investors recently, commercial properties to

believe that the property tax could cause China’s residential property prices to drop 40% investment-purpose

or more. In our opinion, however, property tax is just one component of China’s property residential ones

policies – it should not crash the property market and its upcoming implementation could

actually signal a bottoming in China’s property sector.

Property tax – only part of the housing solution

We expect it to cool the sentiment in the near term for investment and speculation in the We expect it to cool the

property market, but property tax by itself cannot solve the housing issue. sentiment in the near term

for investment/speculation in

The Ministry of Human Resources and Social Security’s proposal to double average

the property market

wages in China within five years, if approved and implemented, should improve the

affordability ratio significantly. The Ministry of Housing and Urban-Rural Development also

announced plans of large scale Public Housing construction. If this plan is implemented

strictly, we should see a surge in public housing supply in the next few years, although the

total amount may stay small in the forseeable future – as of 2009, public housing stock

accounted for less than 5% of total housing stock in China.

Other countries’ experience – it’s unlikely to crash

the market

We draw this conclusion after studying the property tax situation in many countries. South Korea and Mexico’s

Specifically, we studied countries that started to implement property tax only in recent implementaton of property

decades, such as South Korea and Mexico – both started to implement property tax in a tax did not crash the market

hope to reverse the surge of property prices – just like China. Neither of the two countries’

implementaton of property tax caused a crash in the property market.

China’s current plan – limited monetary impact

Based on the current plan’s tax rate, scope and difficulties on implementation, we expect Scenario analysis on

the impact on the property market to be less than what the current stock market assumes. Shanghai’s proposal shows

Our detailed scenario analysis also shows that, even if the full amount of property tax can that the new property tax’s

be successfully collected, the monetary impact on home-buyers should be manageable. net impact to monthly

payment shoud be around

In fact, scenario analysis on Shanghai’s proposal shows that the new property tax’ net

5% to 6% only

impact on monthly payments shoud be only 5% to 6% – an impact even smaller that that

caused by a major interest rate increases.

A gradual reform – no near-term replacement for land

sales

One of the key targets for property tax is to reduce the local government’s reliance on land Local governments may be

sales as the main financing resource. However, this goal cannot be realised in the willing to implement property

foreseeable future, in our view. tax for additional revenue,

but will have to continue to

Land sales has been an important source of revenue for local governments and property

heavily rely on land sales for

tax has been below 4% of local government revenue. Therefore, as discussed earlier in

years to come, in our view

this report, local governments may be willing to implement property tax for additional

revenue, but will have to continue to rely heavily on land sales for years to come, in our

view.

China Property Policy Outlook: 1 3

4. 14 June 2010

Property tax – only part of the

housing solution

We expect the property tax to cool near-term sentiment for investment/speculation in the We expect the property tax

property market. This is likely to be in combination with the wage rise measures to to cool near-term sentiment

increase housing affordability and the large-scale construction of public housing for lower for investment/speculation

income population.

Property tax has undoubtedly been the key factor for

Recently, every new piece

the China property sector’s recent performance of information on the

Ever since Chongqing’s Mayor disclosed on 24 March that the city has submitted a property tax has caused

proposal for property tax implementation to the state council, every new information on China property stock

property tax has resulted in turbulence in China’s property stocks. turbulence

Figure 6: Relative performance (%) of Credit Suisse China Property index performance vs MSCI China (1 March to

current) – property tax has been the key factor

(%)

5

24th Mar : Chongqin g government announced its has subitted its proposal of the implementation of property tax

0

12th May : Media reported that Shanghai

government is in the progress of drafting the

-5

property tax proposal - details include the

possibility of property tax to be le vied at 0.8% p.a

-10

8th April : Rumour that property tax

-15

will be firstly implemented in the 4 first tier cities

17th April : State Council issued 10 tightening

-20 17th May: An assistant manager of NDRC cited that

measures but no mentioning of the property tax was in place.

property tax will not be implemented at least in 3 yr's time

-25 24th May : NDRC refuted the comment above

Mar 10 Mar 10 Mar 10 Mar 10 Mar 10 Apr 10 Apr 10 Apr 10 Apr 10 May 10 May 10 May 10 May 10 May 10 Jun 10

CS China Property Share Price Index (rebased)

Source: Datastream; Credit Suisse research

Why have local governments become much more

interested? This version of property tax is different

The public debate on implementing property tax has been ongoing since 2004 and local

governments have shown no interest in it. Why have local governments become much

more interested in implementing it this time? After Chongqing, many other cities such as

Shanghai, Wuhan and Jinan have also reportedly submitted similar proposals. The key

reason, in our view, is the central government’s decision to extend the holding tax for

commercial properties to investment-purpose residential ones, in order to avoid legislation

issues for implementing a new property tax.

A new property tax needs the People’s Congress’ approval as a formal law, which cannot Local governments were

avoid the debate on whether to remove land premium charges during local government’s previously worried that the

land sales. This is because the land premium payment is widely considered a one-off implementation of property

payment of property use rights/taxes and many believe the formal property tax should tax may take away land

premium payments

China Property Policy Outlook: 1 4

5. 14 June 2010

replace land premium – the key financing sources for local governments. Therefore, local

governments have been against this new, formal property tax.

On the other land, by extending the holding tax for commercial properties (according to a The current version of the

tax law established as early as 1986) to residential properties, local governments can property tax allows local

continue to charge a land premium while gaining an additional type of tax revenue. It is not governments to continue to

surprising that the local governments nowadays are much more interested in implementing charge land premiums while

this version of a property tax. gaining an additional type of

tax revenue

Figure 7: The key messages from the property tax as implemented in 1986

Early establishment of the property tax law and its main points

September 1986 Property tax shall be (A) 1.2% if calculated on the basis of the residual value of a building; or

(B) 12% if it is calculated on the basis of rental

For (A) – the taxable value of the building is subject to a reduction of 10-30% from its original value, the % of reduction

depending on each local government's ruling

The following are exempt from property tax:

1) properties owned and used by government agencies, military units and social organisations

2) State-allocated housing (e.g. those SOE units that were allocated to staff)

3) buildings used for parks, scenic spots and historical sites

4) properties not for operating / investment uses ( i.e. tax is levied on those that are for commercial use only)

5) Others as approved by the relevant or locat authority

Source: State Administration of Taxation

Property tax is likely to become transaction-based

rather than a holding tax

Due to the difficulties in tax administration and collection at the local level, residential Although property tax is

property-related taxes – from land sales markets to secondary housing markets – are all designed to be a holding

collected after transactions are through. According to industry experts, although property tax, it may only become

tax is designed to be a holding tax, it may become feasible to collect upon changes of feasible to collect upon

ownership. In this case, the property tax may actually propel property price appreciation in changes of ownership

the long term, although the negative market sentiment in its implementation causes could

reduce property prices in the near term.

In fact, all residential related taxes currently are transaction-based. The following table

summarises the various taxes for residential properties.

Figure 8: When the land was purchased …

Type Taxpayers Taxation base Tax rate (%)

Deed tax Developers with land use right certificates Cost of obtaining the land use rights 3

Stamp duty (on contract) Developers with land use right certificates Contractual price of the property 0.05

Stamp duty (on land use rights) Developers with land use right certificates Per document Rmb5 per document

Farmland use tax Occupants of the land Usable area of the farmland Rmb5-50 per sq m

Source: State Administration of Taxation

Figure 9: When the property was purchased from developers …

Type Taxpayers Taxation base Tax rate (%)

Deed tax Developers with land use right certificates Cost of obtaining the land use rights 3

Stamp duty (on contract) Developers with land use right certificates Contractual price of the property 0.05

Stamp duty (on land use rights) Developers with land use right certificates Per document Rmb5 per document

Farmland use tax Occupants of the land Usable area of farmland Rmb5-50 per sq m

Source: State Administration of Taxation

China Property Policy Outlook: 1 5

6. 14 June 2010

Figure 10: When the home ownership changes hands …

Type Taxpayers Taxation base Tax rate

Business tax Seller a. General commodity housing: 5.50

If holding period < 5 yrs, then it's 5.5% on the capital gain

If holding period > 5 yrs, then it's exempt from business tax

b. Non-general commodity housing

If holding period < 5 yrs, then it's 5.5% on the sales amount

If holding period > 5 yrs, then it's 5.5% on the capital gain

Personal income tax Seller Capital gain (with document of proof in relation to cost of the property) 20

Sales amount (without document of proof in relation to cost of the property) 1

LAT Seller Sales amount Ordinary housing: exempt;

Non-ordinary housing:

if holding period > 5 yrs: exempt; 3-5 yrs: 50% of tax; <3 yrs: standard cal.

Stamp duty (on contract) Sellers and home buyer Sales amount 0.30

Stamp duty (on land use rights) Home buyer Per document Rmb5 per document

Deed tax Home buyer Contractual price of the property General residential: 1.5

Source: State Administration of Taxation

Limitations determine that property tax itself cannot

be the solution to China’s housing problem

Given the limitations discussed above, we believe the implementation of property tax itself We believe the

cannot solve China’s housing problems. More sustainable measures include the wage implementation of property

increase to raise housing affordability and the large-scale construction of public housing tax itself cannot solve

for the lower income population. China’s housing problem

Recently, the Ministry of Human Resources and Social Security submitted its proposal to

double average wages in China within five years. If this proposal is approved and

implemented, the affordability ratio in China should improve significantly. Earlier this year,

the Ministry of Housing and Urban-Rural Development also announced plans of large

scale Public Housing construction, and signed agreements with local goverments to start

the construction with scale within 2010. If this plan is implemented strictly, we should see a

surge in public housing supply in the next few years, although the total amount may stay

small in the forseeable future – as of 2009, public housing stock took up less than 5% of

total housing stock in China.

Figure 11: China’s proposed solutions to its housing issue

Property tax

(near-term) Investors/

speculators

Double wages

(five-year plan)

Middle class

Public housing

(long term but start now?)

Low-income population

Source: Credit Suisse research

China Property Policy Outlook: 1 6

7. China Property Policy Outlook: 1

Figure 12: A brief history of China’s property-related policies vs property prices and volume changes

(%) (%)

35 Suppress demand (05-07) Stimulate demand (08) 220

2005-07: The 70/90 rule was introduced. 2008: Reduced the dis count to frm 15% to 30% for

210

Required down payment ratio raised from 1st home buyers. Reduced down payment ratio from

200

30 20% to 30% for 1st home buyers. Benchmark 30% to 20% for 1st home buyer. Reduced of deed tax

lending rate raised by 27bpts to 7.47% - a total from 1.5% to 1%. Business tax for individual ppty 190

of six times in 07 transactions is exempt if holding period > 2 years. 180

25 Stimulate demand (98-99)

170

1998: Housing reform: Abolished the

160

state-allocated housing policy & introduced Stablise supply (02-04

20 150

the transfer of state-owned land use rights 2002: Rules regarding grant of Land

1999: Maximum mortgage term extended Use Rights by way of 1. Tender, 140

15 to 30 yrs and max. mortgage financing 2. Auction or 3. Listing for 130

increased from 70% to 80% sale were issued. ) 120

Suppress demand 110

10

End 2009-10: 100

Min down payment is at

90

5 50% of the total land

80

premium. Down payment

ratio = 50% (vs previous 70

0 40%) for 2nd home buyers 60

50

-5 40

30

20

-10

10

0

-15

-10

-20

-20 -30

Mar 99 Mar 00 Mar 01 Mar 02 Mar 03 Mar 04 Mar 05 Mar 06 Mar 07 Mar 08 Mar 09 Mar 10

YTD GFA sold - yoy % change ASP (residential) - yoy % change - LHS

Source: CEIC, Credit Suisse research

14 June 2010

7

8. 14 June 2010

Other countries’ experience – it’s

unlikely to crash the market

We studied property tax policies in other countries and conclude that property tax should

be a common practice and not a main factor for property price changes.

Figure 13: Property-related tax policies in other countries

Country Type Tax payers Taxable items Taxation base Tax rate (%)

US Property tax Property owners Property Current market value of the property 0.12-3.05

Land Current market value of the land 1

France Land tax Owner of land Land and property Est. rental income 3-10

Residency tax Owners or tenants Property Est. rental income 5-13

England City tax Owners or tenants Residential Current market value of property 0.67-2

Commercial property Owners or tenants Non-residential Est. rental income ~40

tax (non-residential)

Chille Fixed assets tax Owners of all fixed All types of buildings Cost of the building 2

assets (including property)

Japan Fixed assets tax Owners All types of fixed Market value (revalued once 1.4%;capped at 2.1

assets every three years)

Singapore Property tax Owners/Government Private and public Rental income Self-use: progressive:

assigned land lords housing first S$6,000 taxed at

0%; Next S$50,000 at

4%; >S$65,000 at 6%

Other purpose: 10%

Hong Kong Rates Owners Property Est. rental income 5

Goverent rent Owners Property Est. rental income 3

Property tax Owners Property Rental income 15

Taiwan Land tax Land owners Land Government appraisal value 0.2-5.5

Property tax Property owners Property Government appraisal value Residential: 1.2

Non-residential: 1.5-5

Source: Relevant Tax Authorities

Specifically, we studied countries that only started to implement property tax in recent Both South Korea and

decades, such as South Korea and Mexico – both started to implement property tax in a Mexico started to implement

hope to reverse the surge of property prices – just like China. Neither of the two countries’ property tax to try to reverse

implementaton of property tax caused a crash in the property market. the surge in property prices

The property tax in both South Korea and Mexico is based on the value of property and

Neither South Korea nor

collected at a progressive rate, e.g. the higher the value, the higher the rate.

Mexico’s implementation of

For Mexico, the rate is 0.275-1.35% and was implemented in 1999. From the price chart property tax caused a crash

below, it had some impact on price, as reflected by a 4% YoY decline in prices for 2000. in the property market

But the impact seems to have been short-lived, as prices resumed their upward trend later.

For Seoul, it was first implemented in 1988 and revised in 2006. The rate is from 1-3%.

From the chart below, we can see that the implementation of property tax seems to have

not had much impact on property prices, which continued to rise after its implementation/

revision.

China Property Policy Outlook: 1 8

9. 14 June 2010

Figure 14: South Korea – price index before and after Figure 15: Mexico – property price index before and after

implementation of property tax implementation of property tax

De c 08 = 100

12 0 (Peso/sqm)

12,000

10 0 11,000

Property tax

10,000

first introduced

introduced

80 9,000

8,000

60 7,000

6,000

40 5,000

Property tax

revised 4,000 Property tax first introduced

20 3,000

2,000

0

1994 1996 1998 2000 2002 2004 2006 2008

Ja n- 8 8

Ja n- 9 1

J an- 9 2

Ja n- 9 5

Ja n -9 9

Ja n-0 3

Ja n-0 6

Ja n-1 0

Jan - 86

Jan - 87

Jan - 89

Jan - 90

Jan - 93

Jan - 94

Jan -96

Jan -97

Jan -98

Jan -00

Jan -01

Jan -02

Jan -04

Jan -05

Jan -07

Jan -08

Jan -09

Source: Government websites Source: Government websites

China Property Policy Outlook: 1 9

10. 14 June 2010

China’s current plan – limited

monetary impact

Based on the current plan’s tax rate, scope and difficulties on implementation, we expect

the impact on the property market to be less than what the current stock market assumes.

Our detailed scenario analysis also shows that, even if the full amount of property tax can

be successfully collected, the monetary impact to home buyers should be manageable.

Shanghai’s proposal targets only large-size property

with only 0.8% tax rate

The recent public attention on property tax has focused on Shanghai. Shanghai is said to Shanghai is said to have

have submitted proposals to implement property tax. The recently discussed tax rate is submitted proposals to

about 0.6-0.8% – at the low end of the international range. The scope of property tax is implement property tax

also limited to families with more than one property and the taxable property size more

than 70 sq m per person.

Figure 16:The two version of Shanghai’s proposal for property tax – their conditions:

Proposal A – “the milder” plan Proposal B – the “stricter” plan

Implementation date The property would be subject to a property tax if the A property tax would be levied on all properties bought

property is bought after the date of implementation (i.e. irrespective of the date of implementation AND

property purchased before that would not be subject to

property tax) AND

Unit size The purchase is a 2nd purchase with an average unit size The purchase is a 2nd purchase with an avg. unit size >

> 70 sq m per capita or 3rd or more purchase of any 70 sq m per capita or 3rd or more purchase of any unit

unit size (i.e. first purchase would not be subject to size (i.e. first purchase would not be subject to property

property tax)' tax)'

Source: Company data, Credit Suisse estimates

More importantly, since the current version of the residential property tax is an extension

of the 1986 tax law currently used only for commercial properties, the residential property

tax would very likely follow the following principles:

1) The tax is based on the purchase value of the property, rather than current market

value;

2) The taxable amount is 70-90% of the purchase value.

Property tax’s impact would be similar to interest

rate increase for those who buy and hold

For home buyers that have no plans to sell their property in the foreseeable future, the Scenario analysis shows

property tax can be viewed as a payment similar to mortgage payments. that the new property tax’

net impact to monthly

Using Shanghai as an example, the proposed policy implies a taxable unit should be at

payment shoud be around

least 140 sq m for a couple with no children. Therefore, the minimal value of an housing

5% to 6% only – even

unit in Shanghai city area should be around Rmb3 mn in order to be affected by the new

smaller impact than what a

property tax policy. The tables below shows that the new property tax should only be 5%

major interest rate increase

to 6% of average mortgage payments – even smaller impact than what a major interest

can cause

rate increase can cause.

China Property Policy Outlook: 1 10

11. 14 June 2010

Figure 17: Additional mortgage payment incurred based on Proposal A & B of the above

Ppty tax rate 0.60% 0.80% 1.00%

A. Sales amount = Rmb 3mn

Yearly mortgage payment: without property tax - Rmb 134,330 134,330 134,330

Yearly total payment: with property tax - Rmb 140,711 142,870 145,045

Additional payment per year - Rmb 6,381 8,540 10,715

Additional payment per year - % 5% 6% 8%

B. Sales amount = Rmb 6mn

Yearly mortgage payment: without property tax - Rmb 223,883 223,883 223,883

Yearly total payment: with property tax - Rmb 234,518 238,116 241,742

Additional payment per year - Rmb 10,634 14,233 17,859

Additional payment per year - % 5% 6% 8%

C. Sales amount = Rmb 10mn

Yearly mortgage payment: without property tax - Rmb 447,767 447,767 447,767

Yearly total payment: with property tax - Rmb 469,035 476,233 483,484

Additional payment per year - Rmb 21,268 28,466 35,718

Additional payment per year - % 5% 6% 8%

Source: Credit Suisse estimates

Detailed calculation of Scenario A - C above

Figure 18: Property tax impact on mortgage rate for 2nd home buyers – if sales value = Rmb3 mn

Case 1 Case 2 Case 3

Property holding tax (%) 0.60% 0.80% 1%

Property purchase value (Rmb 3,000,000 3,000,000 3,000,000

Before property tax

Mortgage payment per year (for a 25-year mortgage 134,330 134,330 134,330

with interest rates = average of 2007-curent)

After property tax

Property tax needs to be paid ^ 7,200 9,600 12,000

Mortgage payment per year 140,711 142,870 145,045

Increase in total payment per year (Rmb) 6,381 8,540 10,715

Increase in total payment per year (%) 5% 6% 8%

Source: Credit Suisse estimates: ^ assuming there will be a 20% reduction of the original property value

Figure 19: Impact of property tax on mortgage rate for 2nd home buyers – if sales value = Rmb6 mn

Case 1 Case 2 Case 3

Property holding tax (%) 0.60% 0.80% 1%

Property purchase value (Rmb 5,000,000 5,000,000 5,000,000

Before property tax

Mortgage payment per year (for a 25-year mortgage 223,883 223,883 223,883

with interest rates = average of 2007-curent)

After property tax

Property tax needs to be paid ^ 12,000 16,000 20,000

Mortgage payment per year 234,518 238,116 241,742

Increase in total payment per year (Rmb) 10,634 14,233 17,859

Increase in total payment per year (%) 5% 6% 8%

Source: Credit Suisse estimates;^ assuming there will be a 20% reduction of the original property value

China Property Policy Outlook: 1 11

12. 14 June 2010

Figure 20: Impact of property tax on mortgage rate for 2nd home buyers –if sales value = Rmb10mn

Case 1 Case 2 Case 3

Property holding tax (%) 0.60% 0.80% 1%

Property purchase value (Rmb 10,000,000 10,000,000 10,000,000

Before property tax

Mortgage payment per year (for a 25-year mortgage

447,767 447,767 447,767

with interest rates = average of 2007-curent)

After property tax

Property tax needs to be paid ^ 24,000 32,000 40,000

Mortgage payment per year 469,035 476,233 483,484

Increase in total payment per year (Rmb) 21,268 28,466 35,718

Increase in total payment per year (%) 5% 6% 8%

Source: Credit Suisse estimates;^ assuming there will be a 20% reduction of the original property value

For the sell-at-higher-price type, property tax is likely

to be treated as a transaction cost

For home buyers that plan to sell their property in the foreseeable future, the property tax Property tax as part of the

can be viewed as part of the transaction costs. transaction costs should be

manageable as well –

As discussed earlier in this report, the table below shows that currently total taxes for

especially if the costs are

secondary housing transactions should be around 10% of the transaction value or higher

borne jointly by both the

(depending on the capital gains tax). If the home buyer sells the property five years after

seller and the buyer

the purchase, the cumulative property tax should be 2.4-3.2% of the purchase value (with

a property tax rate of 0.6-0.8%). Therefore, property tax as part of the transaction costs

should be manageable as well – especially if the costs are borne jointly by both the seller

and the buyer.

Figure 21: When the home ownership changes hands …

Type Taxpayers Taxation base Tax rate (%)

Business tax Seller a. General commodity housing: 5.50

If holding period < 5 yrs, then it’s 5.5% on the capital gain

If holding period > 5 yrs, then it's exempt from business tax

b. Non-general commodity housing

If holding period < 5 yrs, then it's 5.5% on the sales amount

If holding period > 5 yrs, then it's 5.5% on the capital gain

Personal income tax Seller Capital gain (with document of proof in relation to cost of the property) 20

Sales amount (without document of proof in relation to cost of the property) 1

LAT Seller Sales amount Ordinary housing: exempt;

Non-ordinary housing:

if holding period > 5 yrs: exempt; betw 3-5 yrs: 50% of tax; <3yrs: standard cal.

Stamp duty (on contract) Sellers and home buyer Sales amount 0.30

Stamp duty (on land use rights) Home buyer Per document Rmb5 per document

Deed tax Home buyer Contractual price of the property General residential: 1.5

Source: State Administration of Taxation

China Property Policy Outlook: 1 12

13. 14 June 2010

A gradual reform – no near-term

replacement for land sales

One of the key targets for property tax is to reduce the local government’s reliance on land

sales as the main financing resource. However, this goal cannot be realised in the

foreseeable future, in our view.

As shown in the two tables below, land sales has been an important source of revenue for

local governments, and property tax has been below 4% of local government revenue.

Therefore, as discussed earlier in this report, local governments may be willing to

implement property tax for additional revenue, but will have to continue to heavily rely on

land sales for years to come, in our view.

Figure 22: Top 10 cities’ land sales vs local government revenue (2009)

Land Land sales revenue to the local Local government Land sales revenue / local

sales government (assuming 70% revenue government revenue

City (Rmb bn) allocation) (Rmb bn)* (excluding land sales) (excluding land sales) (%)

Hangzhou 112 79 52 151

Shanghai 103 72 254 28

Beijing 93 65 203 32

Tianjin 74 52 82 63

Guangzhou 48 34 70 48

Chongqing 45 31 68 46

Ningbo 42 29 43 68

Wuhan 36 25 32 80

Chengdu 36 25 39 64

Foshan 34 24 25 94

Source: Company data, Credit Suisse estimates; *assume 70% being allocated to local government

Figure 23: Government’s tax revenue breakdown

Local govt’s (Property + Urban Land tax) /

Year Total tax Local govt’s revenue Property Urban Local govt’s revenue

(Rmb bn) revenue tax revenue (ex. land sales) tax land tax (ex. land sales) (%)

1998 909 295 498 16 5 4.2

1999 1,032 331 560 18 6 4.3

2000 1,267 373 641 21 7 4.4

2001 1,517 472 480 23 7 6.3

2002 1,700 531 852 28 8 4.2

2003 2,047 630 985 32 9 4.2

2004 2,572 786 1,189 37 11 4.0

2005 3,087 953 1,510 44 14 3.8

2006 3,764 1,145 1,830 52 18 3.8

2007 4,945 1,503 2,357 58 39 4.1

Up to 3Q08 4,606 1,426 2,865 49 61 3.8

Source: State Administration of Taxation

China Property Policy Outlook: 1 13