Download to read offline

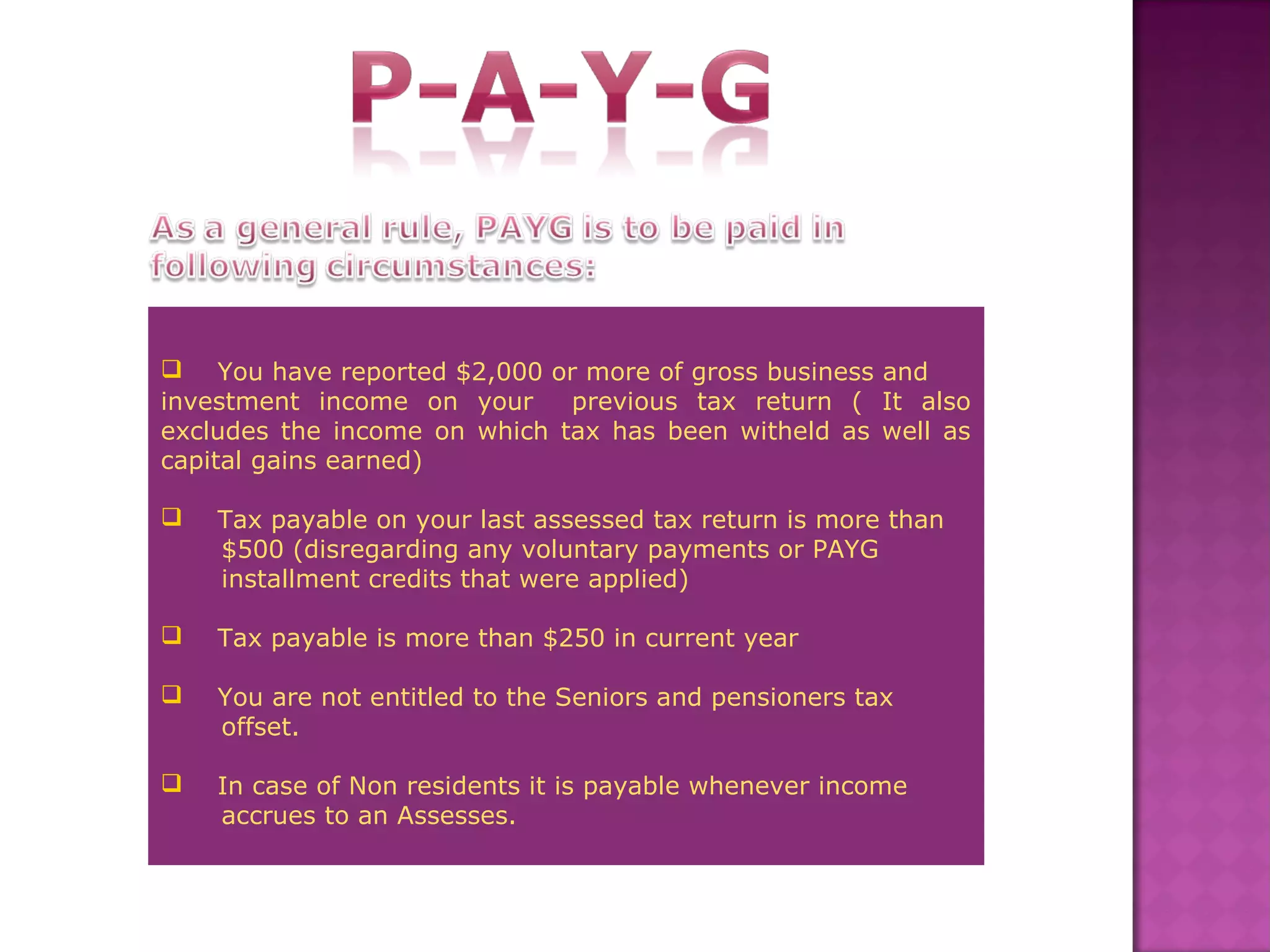

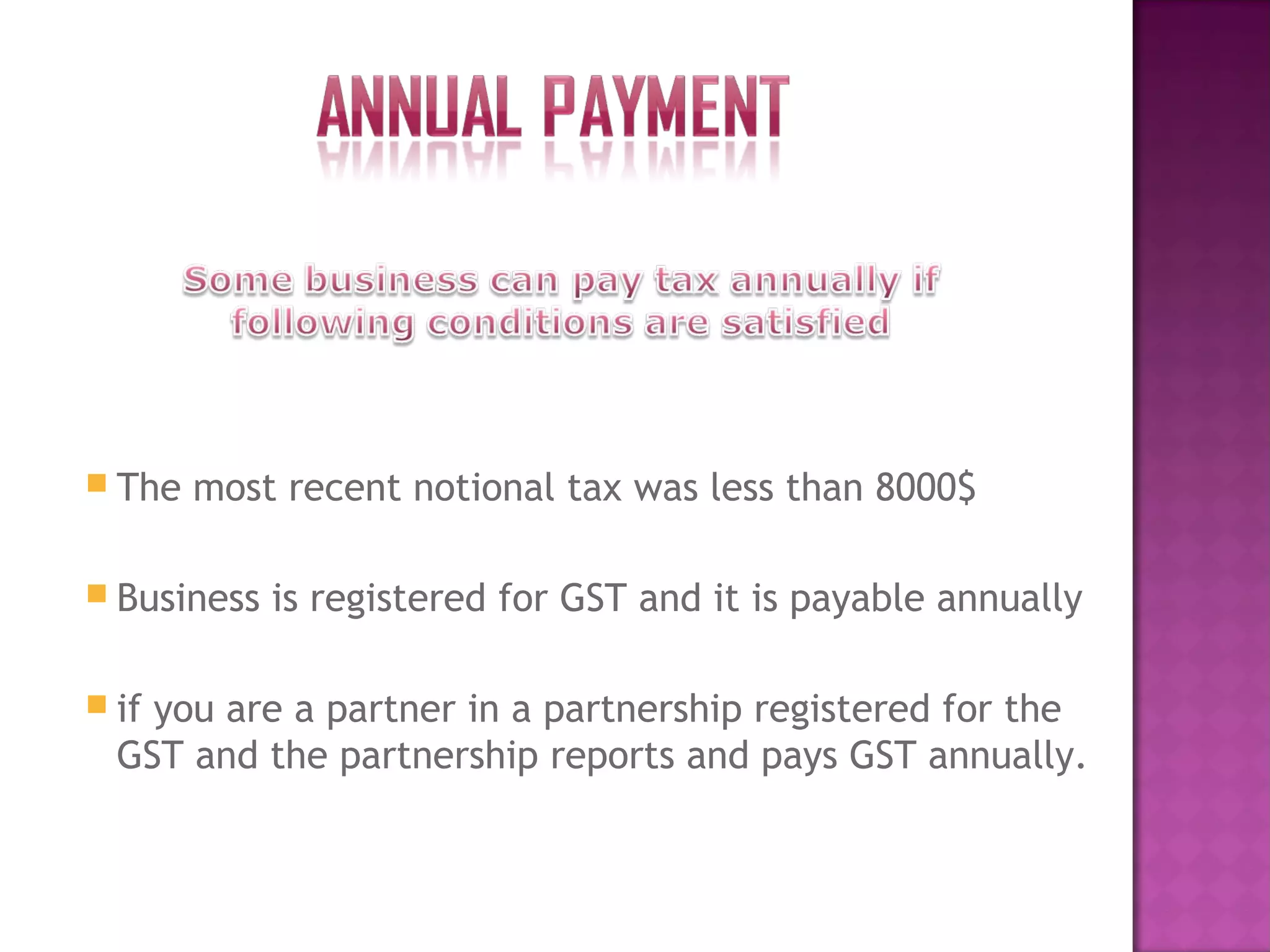

This document provides an overview of the Pay As You Go (PAYG) installment compliance requirements, detailing when individuals are liable to make payments based on gross business and investment income. It outlines specific conditions for liability, payment schedules, and the implications of self-calculating installments versus using ATO calculations. Additionally, it addresses the filing procedures for business partnerships and considerations for non-residents.