Building pressure? Rising rents, and what to expect in the future

HostHotels_05AnnualReport

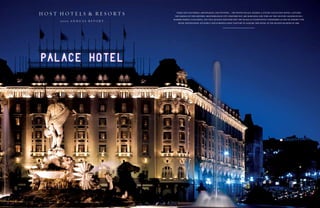

1. HOST HOTELS & RESORTS WARM AND GLITTERING, ARISTOCRATIC AND INVITING… THE WESTIN PALACE, MADRID, A LUXURY COLLECTION HOTEL, CAPTURES

THE ESSENCE OF THIS HISTORIC MEDITERRANEAN CITY. WHETHER YOU ARE SEARCHING FOR TURN-OF-THE-CENTURY GRANDEUR OR A

MODERN WORLD-CLASS HOTEL, YOU WILL QUICKLY DISCOVER WHY THE PALACE IS CONSISTENTLY CONSIDERED AS ONE OF EUROPE’S TOP

2005 ANNUAL REPORT

HOTEL DESTINATIONS. WE EXPECT OUR EUROPEAN JOINT VENTURE TO ACQUIRE THIS HOTEL IN THE SECOND QUARTER OF 2006.

2. INTERNATIONAL BRANDS AND MARKETS

upon the expected completion of the acquisition of the starwood portfolio in the second quarter of 2006,

we will have ownership interests in 137 premium-branded hotels, in nine countries and over 50 markets.

[ABOVE] The centuries-old Westin Europa & Regina is an architectural landmark

just steps from Piazza San Marco in Venice, Italy. Named to Conde Nast Traveler’s

2005 Gold List, the hotel offers guests a combination of traditional elegance and

modern technology, while providing the same magnificent views of the Grand

Canal that once inspired Monet. We expect our European joint venture to acquire

this hotel in the second quarter of 2006.

HOST HOTELS & RESORTS

will be the premier hospitality real estate

company. we will own high-quality lodging

assets in prime urban, airport and resort /

convention lo cations. creating value

through aggressive asset management and

disciplined capital allocation to generate

superior performance, we will maximize

shareholders’ returns through a combina-

tion of dividends, growth in funds from

operations and increases to net asset value

per share.

EXISTING MARKETS (AS OF DECEMBER 31, 2005)

MARKETS ACQUIRED AS PART OF THE STARWOOD ACQUISITION

EUROPEAN JOINT VENTURE MARKETS

3. F I NA N C I A L H IG H L IG H T S

2005 2004 2003

(unaudited, in millions, except per share data, hotel data, and stock price)

OPERATING DATA

Revenues $ 3,881 $ 3,574 $3,223

Operating profit 519 397 290

Net income (loss) 166 — 14

DILUTED INCOME (LOSS) PER COMMON SHARE

Income (loss) from continuing operations $ .30 $ (.34) $ (1.00)

Diluted income (loss)(1) $ .38 $ (.12) $ (.07)

Diluted weighted average shares outstanding 355.5 337.3 281.0

BALANCE SHEET DATA

Total assets $ 8,245 $ 8,421 $8,592

Debt(2) 5,370 5,523 5,486

Convertible preferred securities(2) — — 475

Equity 2,417 2,395 2,136

OTHER DATA

Adjusted EBITDA(1) $ 918 $ 790 $ 709

host hotels & resorts 2005

Funds from operations per diluted share(1) 1.15 .77 .99

Stock price on December 31st 18.95 17.30 12.32

COMPARABLE HOTEL DATA (3)

Number of properties 98 98

Number of rooms 48,785 48,785

1

Average daily rate $166.80 $154.96

Occupancy percentage 73.6% 72.4%

RevPAR(4) $122.82 $112.21

(1) Certain transactions significantly affected Funds From Operations (FFO) per diluted share, Adjusted Earnings before Interest Expense, Income Taxes,

Depreciation, Amortization and other items (Adjusted EBITDA) and income (loss) per share for all years presented. FFO per diluted share and Adjusted

EBITDA are non-GAAP financial measures within the meaning of the rules of the Securities & Exchange Commission and, accordingly, these measures

have been reconciled to comparable GAAP measures. For further discussion of FFO per diluted share, see Management’s Discussion and Analysis of

Results of Operations and Financial Condition. For further discussion of Adjusted EBITDA, see our Form 8-K dated and filed February 23, 2006.

(2) Effective January 1, 2004, we adopted a revision to Financial Interpretation No. 46 “Consolidation of Variable Interest Entities” (FIN 46R). As a result,

we deconsolidated a wholly owned limited purpose trust subsidiary (the “Trust”) and recorded the $492 million Convertible Subordinated Debentures

issued by the Trust as debt and eliminated the $475 million of Convertible Preferred Securities that were previously classified in the mezzanine section

of our consolidated balance sheet prior to January 1, 2004. For further discussion see Management’s Discussion and Analysis of Results of Operations

and Financial Condition.

(3) We define our comparable hotels as full-service properties that are owned or leased by us and the operations of which are included in our consoli-

dated results, whether as continuing operations or discontinued operations, for the entirety of the reporting periods being compared, and that have

not sustained substantial property damage or undergone large-scale capital projects during the reporting periods being compared.

(4) Room revenue per available room (“RevPAR”) represents the combination of average daily room rate charged and the average daily occupancy achieved,

and is a commonly used indicator of hotel performance. RevPAR does not include food and beverage or other ancillary revenues generated by the property.

C ON T E N T S

To Our Stockholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Reports of Independent Registered Public Accounting Firm on

Internal Control Over Financial Reporting and Management’s

Board of Directors and Management Team . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 Assessment and on the Consolidated Financial Statements . . . . . . . . . . . . 70

Management’s Discussion and Analysis of Results of

Management Certifications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Operations and Financial Condition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Forward-Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Host Marriott Portfolio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Directors, Officers and Management Team . . . . . . . . . . . . . . . . Inside Back Cover

Management’s Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Management’s Report on Internal Control Over Financial Reporting . . . . . . 69 Corporate Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Inside Back Cover

4. TO OU R S TO C K HOL DE R S

We had an outstanding 2005, delivering significant

increases in operating results, earnings and dividends

and executing on strategic initiatives that will help distin-

guish our company as a global player in the lodging

industry. Throughout the year we maintained our stra-

tegic focus, aggressively managing our existing portfolio

host hotels & resorts 2005

and practicing a systematic and disciplined approach to

capital allocation. Our focus and the continued improve-

ment of lodging fundamentals have enhanced our lodg-

ing portfolio and strengthened our financial position for

the future. Some of the more significant recent accom-

CHRISTOPHER J. NASSETTA plishments include:

2

President and Chief Executive Officer

◆ Our operating results improved significantly over

RICHARD E. MARRIOTT

Chairman of the Board

2004 in nearly every measure of performance. The

RevPAR increase of 9.5% in 2005 was the highest full-year improvement since 1998, helping to drive signifi-

cant increases in operating margins and cash flow;

◆ On November 14, 2005, we entered an agreement to acquire an outstanding portfolio of hotels from Starwood

Hotels & Resorts Worldwide, Inc. On April 10, 2006, we completed the purchase of 28 of the properties and

expect to close on the remaining seven properties by the end of the second quarter. This $3.8 billion acquisi-

tion delivers on all of our qualitative and quantitative acquisition parameters and forges a new partnership

with one of the most innovative brand and management companies in the lodging industry;

◆ We formed a joint venture on March 24, 2006 to own the Starwood hotels in Spain, Italy, Poland and the

United Kingdom and to serve as a platform for further European expansion, as well as provide approximately

$560 million of financing for the acquisition of the European hotels from Starwood;

◆ On September 30, 2005, we purchased the 834-room Hyatt Regency Washington on Capitol Hill for $274 mil-

lion, the seventh Hyatt-managed property in our portfolio;

◆ We have pursued opportunities to unlock the inherent real estate value in our portfolio where it exceeds the

value of the properties as hotels, such as in the sales in 2006 of the Fort Lauderdale Marina Marriott and the

Swissôtel The Drake, New York for approximately $580 million;

5. ◆ We have enhanced our existing portfolio through investment in repositioning and return on investment proj-

ects spending over $100 million on these high yield projects in 2005;

◆ We continued to recycle capital out of assets that are not in keeping with our long-term strategic goals in

2005, including the sale of five non-core assets and 85% of our interest in the Courtyard by Marriott joint

venture for proceeds of over $240 million; and

◆ We continued to restructure our balance sheet in ways that have increased flexibility and, as a result, we are

host hotels & resorts 2005

well on our way to achieving the strongest balance sheet in our history.

We believe these accomplishments exemplify the focused and disciplined approach to running our business that

has made us the nation’s premier owner of lodging real estate. Consistent with our expectations, 2005 marked

the second year of strong growth in what we expect to be a sustained recovery in the lodging industry. Our focus

3

on luxury and upper-upscale hotels has, over the long-term, provided superior returns to our stockholders

through appreciation in net asset value and growth in earnings and dividends. We believe that the combination

of continued strong demand growth and supply growth that remains at historically low levels, particularly in our

segments and markets, will sustain the current powerful recovery in the lodging industry and produce results that

are some of the best in our history. Based on these strong fundamentals, we believe we are at an attractive point

in the lodging cycle to grow our business both in North America and, with the help of our newly-formed joint

venture, Europe as well.

While we recently renamed the company Host Hotels & Resorts, Inc. to reflect the fundamental changes that we

have undergone over the past 12 years, our vision, mission, values and strategy remain unchanged. Our evolu-

tion from a domestic company with a single brand and an enterprise value of just over $3 billion to an emerging

international company with multiple world-renowned brands and an enterprise value of over $17 billion has

been dramatic. Yet, through it all, we have remained steadfast to our demanding best-in-class standards. These

steps, the positive lodging fundamentals, and our unmatched portfolio and strong capital structure should result

in meaningful growth in RevPAR, earnings and superior returns to our stockholders next year and beyond.

RICHARD E. MARRIOTT CHRISTOPHER J. NASSETTA

Chairman of the Board President and Chief Executive Officer

APRIL 10, 2006

6. UNWAVERING S T R AT EG IC FO C U S

Our success over the past 12 years is a direct reflection of

our clear and unwavering strategic focus, which is to pro-

vide superior total returns to our stockholders through

appreciation in asset values and growth in earnings and

dividends. To achieve these goals, we have carefully exe-

cuted on a focused and disciplined long-term strategic

plan to acquire high-quality lodging assets in prime

urban and resort destinations that have the potential for

significant capital appreciation. We then work to enhance

the value of the portfolio by working with our operators

host hotels & resorts 2005

to aggressively manage our hotels to increase revenues

and minimize operating costs, while pursuing selective

capital improvements designed to increase profitability.

The building blocks of this strategic vision have been the prudent stewardship of our capital structure.

Management has made every effort to maintain the appropriate balance of debt and equity, while providing the

4

company with sufficient flexibility to be able to react to market forces. During 2005, our commitment to a strong

capital structure permitted us to move forward on several of our strategic initiatives; including the purchase of

the Hyatt Regency Washington on Capitol Hill, an aggressive capital investment program in our existing port-

folio and most significantly, the acquisition of the Starwood portfolio.

Our success in restructuring our balance sheet over the past several years has resulted in reduced overall lever-

age, expanded financial flexibility and improved interest coverage ratios. Including the first quarter of 2006 con-

version of our Convertible Subordinated Debentures into common shares and other financing activities since the

beginning of 2003 through 2005, our debt balance has decreased over $1 billion and our annual interest pay-

ments have decreased over $100 million. We will continue to pursue future opportunities to reduce leverage or

improve coverages by the selective recycling of capital and the repayment or refinancing of debt when rates are

favorable. The correct capital structure also means having ample liquidity. Our near-term liquidity, including

available cash and $575 million of capacity under our credit facility, is strong and more than sufficient to con-

tinue to invest in our existing portfolio, as well as take advantage of acquisition opportunities that meet our

investment criteria.

[ABOVE] The spectacular twin towers of the 1,356-room San Diego Marriott Hotel & Marina are adjacent to the Convention Center and Seaport

Village in the heart of downtown San Diego and is within comfortable walking distance of the Gaslamp District, Farmers market and other popular

attractions. The hotel features over 100,000 square feet of meeting space as well as a 446-slip marina, one of California’s largest.

[RIGHT] Casting its dramatic reflection onto the bay, the Tampa Marriott Waterside is a major factor in the successful redevelopment of the

city’s Channel District. Connected directly to the 353,000 square foot Tampa Convention Center and close to Ybor City, the historic and vibrant

Latin district, this property significantly enhances Tampa’s appeal as a major convention destination.

7.

8. THE FAIRMONT KEA LANI MAUI, HAWAII’S ONLY ALL-SUITE RESORT, RESTS GRACEFULLY ON POLO BEACH, ON THE SUNNY SOUTHWEST

SHORES OF MAUI. THE NAME KEA LANI MEANS “HEAVENLY WHITE,” WHICH APPROPRIATELY DESCRIBES THE GLEAMING WHITE EXTERIOR

OF THIS LAVISH RESORT. THIS TROPICAL PARADISE RESORT OFFERS A MYRIAD OF ISLAND ACTIVITIES, INCLUDING WINDSURFING OFF THE

BEACH, RELAXING AT THE SPA OR AN INTIMATE DINNER ON YOUR PRIVATE LANAI.

9. SUPERIOR A S S E T M A NAG E M E N T

Growth in revenues and profits is not guaranteed, it is

earned. Future increases in revenues and operating profits

at our hotels will result from our aggressive approach to

asset management. As the largest owner of luxury and

upper-upscale properties, our asset management team

benefits from the diversity of premium brands and the

size and composition of our portfolio. Our broad per-

spective provides us with a unique ability to benchmark

similar hotels and identify best practices, value enhance-

ment opportunities and efficiencies that can be commu-

host hotels & resorts 2005

nicated to our managers. We work closely with our

managers to implement these strategies, which result in

enhanced revenue management, reduced operating costs

and other operating synergies, all of which will improve the long-term profitability and value of our portfolio. In

this regard, the Starwood portfolio presents an exciting opportunity as these hotels have never benefited from the

oversight of a third-party asset manager. We already have identified key opportunities and developed a strategic

8

plan for each property to uncover ways revenues can be enhanced, costs reduced and margins improved.

We have seen a marked improvement in demand in all segments of our business, which has provided our oper-

ators the ability to increase room rates while also increasing the mix of business represented by higher-rated

segments. We also experienced strong margin improvement in 2005, as the growth in RevPAR was primarily

driven by significant increases in room rates, as well as improvements in food and beverage sales. Controlling

operating costs is always a key priority. We work closely with our operators to reduce costs and generate savings

in ways that do not impact the quality of our hotels or guest satisfaction, which has resulted in increases in oper-

ating margins despite costs such as labor and utilities rising at a rate greater than inflation. As we continue to

maximize the business mix at our hotels, we expect to see further improvements in our operating margins.

Standing as a beacon in the thriving heart of Seattle, the W Seattle is a premier destination for the savvy traveler. The W Seattle’s

[ABOVE]

modern crown of a steel-and-mesh pyramid provides a magical glow 26 stories above the street reflecting this city’s architectural history

and unique northwestern style.

[RIGHT] Explore all our Nation’s capital offers from this newly renovated luxury hotel in Washington, D.C. The Hyatt Regency Washington on

Capitol Hill places you close to government and business centers, museums, memorials and other attractions. Delight in all that this downtown Washington, D.C.

hotel affords—from Grand Beds in all 834 spacious guestrooms and fine dining, to wireless Internet and 41,000 square feet of function space.

10.

11. RESEMBLING A GRAND MEDITERRANEAN VILLA, THIS LUXURIOUS 463-ROOM HOTEL IS SET AMIDST

20 BEACHFRONT ACRES ON FLORIDA’S SOUTHWEST COAST. THE RITZ-CARLTON, NAPLES HAS EARNED

BOTH MOBIL FIVE-STAR AND AAA FIVE-DIAMOND RECOGNITION AS ONE OF THE COUNTRY’S TOP RESORTS.

12. UNMATCHED P OR T FOL IO DI V E R S I F IC AT ION

Over the past 12 years, we have strategically assembled an

unmatched portfolio of luxury and upper-upscale hotels.

Our portfolio is geographically diverse within North

America and is operated under some of the most recog-

nized brand names in the hospitality industry. Our $3.8

billion acquisition of the 35 hotels from Starwood, while

vaulting us to one of the largest lodging companies in the

world, is just another step in creating a truly diversified

company both in terms of brand and global presence.

host hotels & resorts 2005

Similar to our existing hotels, the Starwood portfolio is

geographically diverse in domestic markets with strong

growth prospects and limited near-term supply. The port-

folio also represents a unique opportunity to acquire high-quality international assets, particularly in Europe, which

we believe are in the early stages of lodging cycle and, therefore, we have an increased opportunity for additional

growth outside of our domestic markets. As part of the financing for the acquisition and to create a platform for

12

future acquisitions in Europe, we formed a joint venture to own the six hotels in Italy, Spain, Poland and the

United Kingdom in which we will have a 32% ownership interest. The acquisition also provides access to key

domestic markets such as Seattle and an expanded presence in other markets such as New York, Boston and San

Diego, which we believe have strong growth prospects.

Equally important is the continued brand diversification within our portfolio and expanding our relationship

with Starwood, one of the most innovative operating and brand companies in the lodging industry. Established

brand names such as Sheraton, Westin, W and St. Regis represent some of the industry’s highest-performing and

innovative luxury and upper-upscale brands and are a perfect complement to our existing portfolio of premium

brands. Together, the combined portfolio solidifies our position as the premier owner of luxury and upper-

upscale urban and resort properties operated under world-renowned brands.

[ABOVE] The Westin Palace, Milan, a Luxury Collection Hotel, represents the perfect synthesis between style and technology. The hotel

embraces a refined elegance, inspired by the classical Empire-style and features 228 luxurious guest rooms—including 10 suites, which are

endowed with a relaxant private Turkish bath—that will make your stay truly unforgettable.

[RIGHT] The Westin Palace, Madrid, a Luxury Collection Hotel, is a monument to elegance and turn-of-the-century grandeur. Commissioned by King Alfonso XIII

in 1912, it has been a favored meeting point in the Spanish capital ever since and is just minutes from the renowned El Prado and Thyssen-Bornemisza Museums.

We expect our European joint venture to acquire both of these hotels in the second quarter of 2006.

13.

14. LOCATED ON HAWAII’S ROMANTIC AND MYSTICAL ISLAND OF MAUI, THE LUXURIOUS 806-ROOM HYATT REGENCY MAUI

RESORT AND SPA OVERLOOKS 1,800 FEET OF SPARKLING WHITE SAND BEACH. A UNIQUELY ISLAND EXPERIENCE WITH TROPICAL

WATERFALLS AND BRILLIANT FOLIAGE, GUESTS CAN BE PAMPERED AT THE WORLD-CLASS SPA OR EXPERIENCE THE ENERGY

OF A HAWAIIAN LUAU, BUILDING MEMORIES THAT LAST A LIFETIME.

15. STR ATEGIC

C A P I TA L A L L O C AT ION A N D VA L U E E N H A N C E M E N T

Our goal of strategically allocating capital to create long-

term stockholder value through the ownership of luxury

and upper-upscale properties that meet our demanding,

best-in-class standards remains unchanged. The purchase

of the Hyatt Regency Washington on Capitol Hill in

Washington D.C., in October of 2005, is a recent example

of this strategy. The hotel is located in the heart of the

Nation’s capitol just a short walk from the seat of govern-

ment and the National Mall, the classic example of an

urban hotel in a difficult to duplicate location that meets

host hotels & resorts 2005

our best-in-class standard.

During 2005, we made significant progress on one of the

most ambitious capital expenditure plans in our history which included spending over $100 million on reposi-

tioning and return on investment (ROI) projects. These investments range in scope from the complete reposi-

tioning of guest rooms, restaurants and meeting space to the development of world-class spas and exhibit halls.

16

These projects provide some of our highest investment yields and ensure that our hotels are in superior physical

condition, highly competitive in the marketplace and meet our own high-quality standards. For example, in

December 2005, we completed the renovation and repositioning of the Newport Beach Marriott Hotel & Spa at

a cost of approximately $65 million, which included the addition of a spa, 20 new luxury suites, redesigned and

renovated guestrooms, a new restaurant concept and updated meeting space. We plan on investing approximately

$275 million in repositioning and ROI projects in 2006 as we accelerate our efforts to drive growth in cash flow.

We have already identified, and will continue to review, investment opportunities for the Starwood portfolio that

will increase cash flows and shareholder value.

Capital allocation also means realizing the substantial real estate value inherent in our portfolio, as well as unlocking

non-income producing assets such as at the Hyatt Regency Maui, where we are actively pursuing an opportunity to

develop timeshare units on a beachfront parking lot adjacent to our hotel to maximize the value of the real estate

and create shareholder value. Two recent asset sales, the Fort Lauderdale Marina Marriott and the Swissôtel The

Drake, New York, which resulted in combined gain of approximately $345 million, provided the purchasers with

additional development opportunities that far exceed the value of the properties as hotels. By executing on these

sales and redeploying the capital into the purchase of the Starwood portfolio, we believe we have created significant

value. In addition to these sales, we continue to dispose of non-core assets that are not in keeping with our long-

term strategic goals, or fail to meet our on-going investment criteria, provided we can obtain satisfactory pricing.

A sanctuary of quiet comfort, the Newport Beach Marriott Hotel & Spa is nestled overlooking

[ABOVE]

the Upper Back Bay. The recently renovated Lobby Bar, above, is just a small part of the $65 million

renovation recently completed at this hotel.

[RIGHT] One of the Nation’s great convention hotels, the Orlando World Center Marriott is a landmark

property in central Florida. The 2,000-room hotel can satisfy even the most discerning travelers searching for

the best in accommodations and recreational options close to the major Orlando attractions.

16.

17. THE NEWPORT BEACH MARRIOTT HOTEL & SPA OFFERS COASTAL LIVING WITH A

SLEEK, MODERN STYLE. RECENTLY RENOVATED, THE HOTEL FEATURES 532 GUESTROOMS,

MORE THAN 40,000 SQUARE FEET OF EVENT SPACE AND THE ALL NEW PURE BLU SPA.

18. B OA R D OF DI R EC TOR S

host hotels & resorts 2005

Terence C. Golden, Ann McLaughlin Korologos, John B. Morse, Jr.,

[BACK ROW, LEFT TO RIGHT]

Judith A. McHale, Christopher J. Nassetta, Richard E. Marriott, Robert M. Baylis

[FRONT ROW, LEFT TO RIGHT]

20

M A NAG E M E N T T E A M

Matthew L. Richardson, Pamela K. Wagoner, Larry K. Harvey, Gregory J. Larson, Jeffrey S. Clark

[BACK ROW, LEFT TO RIGHT]

James F. Risoleo, Elizabeth A. Abdoo, Christopher J. Nassetta, W. Edward Walter, Minaz Abji

[FRONT ROW, LEFT TO RIGHT]

19. M A NAG E M E N T ’S DI S C U S S ION A N D A NA LYS I S OF

R E S U LT S OF OP E R AT ION S A N D F I NA N C I A L C ON DI T ION

The following discussion should be read in conjunction with Starwood Acquisition

the consolidated financial statements and related notes On November 14, 2005, we announced that we had signed a

included elsewhere in this report. This discussion contains for- definitive merger agreement as amended March 24, 2006 to

ward-looking statements about our business. These statements acquire 35 luxury and upper-upscale hotels from Starwood for

are based on current expectations and assumptions that are approximately $3.8 billion. The portfolio consists of 25 domes-

subject to risks and uncertainties. Actual results could differ tic and 10 international properties and a total of 16,455 rooms

materially because of factors discussed in “Forward Looking managed under the Westin®, Sheraton®, W Hotels®, The

Statements” and “Risk Factors” contained in this report. Luxury Collection® and St. Regis® brands (collectively, the

“Starwood Portfolio”). As part of the acquisition, we expect

RECENT EVENTS AS OF APRIL 7, 2006 to assume approximately $109 million of debt and to issue

Between December 2005 and February 10, 2006, we issued approximately $2.3 billion of equity (133,529,412 common

30.8 million shares of Host common stock upon conversion shares at the exchange price of $17.00 per share) to Starwood

of $473 million principal amount of our Convertible stockholders. The remainder of the purchase price will be paid

Subordinated Debentures and corresponding Convertible in cash. On April 5, 2006, our stockholders approved the

Preferred Securities. The securities were convertible at the issuance of common stock for this transaction with over 99%

option of the holder into shares of Host common stock at the of the votes cast in favor of the issuance. In connection with the

rate of 3.2537 shares per $50 liquidation amount of Convertible completion of the Starwood acquisition, we intend to change

Preferred Security (equivalent to a conversion price of $15.367 our name to Host Hotels & Resorts, Inc. and to change the New

per share of the Company’s common stock). As of March 31, York Stock Exchange symbol that our common stock is traded

2006, $2 million of subordinated debentures and corresponding under to “HST.”

host hotels & resorts 2005

preferred securities remain outstanding and the right to convert We anticipate that the initial closing on all but seven inter-

those securities into Host common stock has expired. We national properties will occur on or about April 10, 2006. The

intend to redeem these securities in the second quarter of 2006. acquisition is subject to certain closing conditions and also sub-

On January 10, 2006, we issued mortgage debt in the ject to a number of terms and conditions that could delay or

amount of $135 million Canadian Dollars ($116 million US prevent the closing of the acquisitions, or result in modifica-

Dollars based on the exchange rate on the date of issuance) tions, such as the exclusion of particular hotels due to the fail-

with a fixed interest rate of 5.195%. The mortgage debt is ure to obtain required consents or certain other developments.

secured by four of our Canadian properties and matures on The Starwood Portfolio is comprised of luxury and upper- 21

March 1, 2011. On January 13, 2006, a portion of the proceeds upscale hotels located primarily in urban, convention or resort

were used to repay the $20 million outstanding balance under destinations with an average size of approximately 500 rooms

our credit facility. including five city-center hotels with over 750 rooms. The portfo-

On March 29, 2006, we issued $800 million of 6 3⁄4% Series P lio is geographically diverse both domestically and internationally,

senior notes due 2016. We intend to utilize the proceeds to fund with most assets located in markets with strong growth profiles

a portion of the Starwood acquisition, redeem $136 million of our and limited near-term supply. The portfolio includes 10 interna-

7 7⁄8% Series B senior notes and for general corporate purposes. tional properties, which will expand our geographic distribution

In 2006, we sold five properties (the Swissôtel The Drake, into new markets outside of the United States. Six hotels repre-

New York; the Fort Lauderdale Marina Marriott; the Albany senting 15% of the portfolio (by revenue) are located in Europe.

Marriott; the Marriott at Research Triangle Park; and the Additional hotels are located in Fiji and in Chile. As a result of the

Chicago Marriott Deerfield Suites) for total proceeds of acquisition, our percentage of revenues from international hotels

approximately $700 million and a total estimated gain in excess will increase from approximately 3% to approximately 4%. We

of $380 million. We expect to use the proceeds from the sales to believe that many of these international markets are in the early

partially fund the acquisition of the Starwood Portfolio and for stages of lodging recovery, offering the opportunity for additional

other corporate purposes. growth outside of the domestic lodging cycle. In addition, we will

We recently negotiated amendments to various management increase our presence in key domestic markets such as New York,

agreements with Marriott International and agreed, among Boston, San Diego and Seattle as a result of this acquisition.

other matters, to waive performance termination tests through We are also expanding an important relationship with

the end of fiscal year 2009, to modify certain extension tests Starwood, and thereby diversifying our brand representation.

which condition the manager’s ability to renew the management The portfolio consists of 17 Sheraton®, 13 Westins®, two W®

agreements, and to extend certain contracts for ten additional hotels, one St. Regis® hotel, one The Luxury Collection® hotel

years. As part of this negotiation, Marriott International in turn and one additional unbranded hotel. With the addition of these

agreed to make a cash payment to us, to reduce an existing cap hotels, 54% of our portfolio (by revenue) will consist of

on the costs and expenses related to chain services that are pro- Marriott-branded hotels, while Westin-branded hotels will rep-

vided on a centralized basis, as well as to establish a cap on cer- resent 9%, up from 1% prior to the acquisition, and Sheraton

tain other costs, to provide us with an incentive to increase our and W-branded hotels will represent 12% and 2%, respectively.

capital expenditures at the hotels through 2008, to waive certain Currently, we do not own any Sheraton or W-branded hotels.

deferred management fees, and to modify the incentive manage- In addition, we expect to work with Starwood to add value to

ment fee on certain contracts. In addition, we agreed to use a the portfolio through aggressive asset management and believe

portion of Marriott International’s cash payment for brand that our expanded relationship will foster additional growth

reinvestment projects at various hotels in our portfolio. opportunities for both companies in the future.

20. Upon completion of the acquisition, we expect to be one of Swissôtel The Drake, New York, the Fort Lauderdale Marina

the largest lodging companies in the U.S. and the sixth-largest Marriott, the Albany Marriott, Chicago Marriott Deerfield

public REIT. We will own 137 luxury and upper-upscale hotels Suites and the Marriott at Research Triangle Park), (ii) sales of

with approximately 70,000 rooms that are affiliated with 17 joint venture interests related to the six European assets to be

brands located in over 50 markets in nine countries. acquired and (iii) the issuance or other incurrence of indebted-

We have received commitments from Goldman Sachs Credit ness to repay any remaining draws on the bridge loan facility.

Partners, L.P., Deutsche Bank AG Cayman Islands Branch, Bank We entered into an agreement on March 24, 2006 with third

of America Bridge LLC and Merrill Lynch Capital Corporation parties regarding such a joint venture in which we will retain

in an aggregate amount of up to $1.39 billion, which is suffi- approximately 32% of the equity interests in the joint venture

cient to fund the cash portion of the purchase price of the while obtaining approximately $560 million of financing,

transactions. The bridge loan facility has a term, excluding including new debt to be issued by the joint venture but exclud-

extensions, of one year. ing our portion of the capital contributions to the joint venture.

We expect to permanently finance the $1.39 billion cash por- Depending upon the timing of the closing of the asset sales and

tion of the purchase price for the transactions through available permanent financing transactions, proceeds therefrom may be

cash and cash proceeds from a combination of (i) asset sales of used to repay the bridge loan facility.

existing assets of approximately $670 million (including the The following table sets forth the location and number of

rooms of hotels included in the Starwood Portfolio:

Domestic Hotels CIT Y STATE COUNTRY RO OMS

Sheraton New York Hotel & Towers New York NY USA 1,746

Sheraton Boston Hotel Boston MA USA 1,216

Sheraton San Diego Hotel & Marina San Diego CA USA 1,044

The Westin Seattle Seattle WA USA 891

The Westin Los Angeles Airport Los Angeles CA USA 740

host hotels & resorts 2005

W New York New York NY USA 688

The Westin Indianapolis Indianapolis IN USA 573

Sheraton Indianapolis Hotels and Suites Indianapolis IN USA 560

The Westin Mission Hills Resort & Spa Rancho Mirage CA USA 512

The Westin Cincinnati Cincinnati OH USA 456

Sheraton Stamford Hotel Stamford CT USA 448

The Westin Tabor Center Denver CO USA 430

W Seattle Seattle WA USA 426

22

The Westin South Coast Plaza Costa Mesa CA USA 390

Sheraton Milwaukee Brookfield Hotel Brookfield WI USA 389

Sheraton Braintree Hotel Braintree MA USA 374

Sheraton Parsippany Hotel Parsippany NJ USA 370

The Westin Waltham-Boston Waltham MA USA 346

The Westin Grand, Washington, D.C. Washington DC USA 263

Sheraton Suites Tampa Airport Tampa FL USA 259

Sheraton Needham Hotel Needham MA USA 247

St. Regis Hotel, Houston Houston TX USA 232

Sheraton Tucson Hotel & Suites Tucson AZ USA 216

Sheraton Providence Airport Hotel Warwick RI USA 206

Capitol Hill Suites Washington DC USA 152

Total—Domestic Hotels 13,174

International Hotels

Sheraton Roma Hotel & Conference Center(1) Rome Italy 634

The Westin Palace, Madrid, a Luxury Collection Hotel(1) Madrid Spain 468

Sheraton Santiago Hotel and Convention Center Santiago Chile 379

Sheraton Skyline Hotel & Conference Centre(1) Hayes United Kingdom 350

Sheraton Warsaw Hotel & Towers(1) Warsaw Poland 350

Sheraton Fiji Resort Nadi Fiji 281

The Westin Denarau Island Resort & Spa Nadi Fiji 267

The Westin Palace, Milan, a Luxury Collection Hotel(1) Milan Italy 228

The Westin Europa & Regina(1) Venice Italy 185

San Cristobal Tower, a Luxury Collection Hotel Santiago Chile 139

Total—International Hotels 3,281

Total 16,455

(1)

We anticipate that these properties will be owned by the European joint venture after the initial closing.

21. OVERVIEW Corporate: This is the benchmark rate which a hotel pub-

■

lishes and offers to the general public. It is typically the

Structure and Business

second highest category, and is for travelers that do not

As of March 1, 2006, we own 103 full-service luxury and upper-

have access to negotiate or discount rates.

upscale hotel properties and we are the largest hotel Real Estate

Special Corporate: This is a negotiated rate offered to

■

Investment Trust, or REIT, in the National Association of Real

companies and organizations that provide significant lev-

Estate Investment Trust’s composite index. A REIT is a legal

els of room night demand to the hotel. These rates are

entity that holds real estate interests and, through payments of

typically negotiated annually, at a discount to the antici-

dividends to stockholders, is permitted to reduce or avoid fed-

pated corporate rate.

eral income taxes at the corporate level. Host operates as a self-

managed and self-administered REIT and owns approximately Discount: This encompasses all discount programs, such

■

95% of the partnership interests of Host Marriott, L.P., (Host as AAA and AARP discounts, government per diem,

LP, or the Operating Partnership). rooms booked through internet distribution and whole-

Our hotels are operated under brand names that are among sale channels, frequent guest program redemptions, and

the most respected and widely recognized in the lodging indus- promotional rates and packages offered by a hotel.

try—including Marriott®, Ritz-Carlton®, Hyatt®, Four Group demand represents clusters of guestrooms booked

Seasons®, Fairmont®, Hilton® and Westin®. Approximately together, usually with a minimum of 10 rooms. Examples

85% of our hotels (as measured by sales) are currently managed include a company training session or a social event such as a

by Marriott International or its affiliates and branded under the family reunion. Group business is segmented into the following

Marriott or Ritz-Carlton brand names. The majority of our three key sub-categories:

properties are located in central business districts of major

Association: Group business related to national and

■

cities, near airports and in resort/conference destinations. The

regional association meetings and conventions.

target profile for our portfolio includes luxury and upper-

Corporate: Group business related to corporate meetings

■

upscale full-service properties in urban and resort/conference

(e.g., product launches, training programs, contract nego-

destinations that benefit from significant barriers to entry by

tiations, and presentations).

competitors. Though hotels meeting this target profile will still

host hotels & resorts 2005

be subject to competitive pressures, we believe this will allow us Other: Group business predominately related to social, mil-

■

to maintain room rate and occupancy premiums over our com- itary, education, religious, fraternity and youth and ama-

petitors. We also seek to maximize the value of our portfolio teur sports teams, otherwise known as SMERF business.

through aggressive asset management by assisting the managers The final segment is contract demand, which refers to

of our hotels in maximizing property operations and by com- blocks of rooms sold to a specific company for an extended

pleting strategic capital improvements. period of time at significantly discounted rates. Contract rates

The majority of our customers fall into three broad groups: are usually utilized by hotels that are located in markets that are 23

transient business, group business, and contract business, experiencing consistently low levels of demand. Airline crews

approximately 57%, 41% and 2%, respectively, of our business are typical generators of contract demand for our hotels.

in 2005. Similar to the majority of the lodging industry, we fur- Our hotels are operated by third-party managers under

ther categorize business within these segments based on charac- long-term agreements under which they typically earn base and

teristics they have in common as follows: incentive management fees related to the revenues and prof-

Transient demand broadly represents individual business or itability of each individual hotel. We provide operating funds,

leisure travelers and is divided into four key sub-categories: or working capital, which the managers use to operate the

premium, corporate, special corporate and discount. Overall, property, including purchasing inventory and paying wages,

business travelers make up approximately 80% of transient utilities, property taxes and other expenses. We generally receive

demand at our hotels, with leisure travelers making up the a cash distribution, which reflects hotel-level sales less property-

remainder. Therefore, our business will be more significantly level operating expenses (excluding depreciation), from our

affected by trends in business travel versus leisure demand: hotel managers each four week or monthly accounting period,

Premium: Sometimes referred to as “rack rate,” typically depending on the manager.

■

consists of rooms booked close to arrival during high Hotel revenue is approximately 97% of our total revenue.

demand periods and is the highest rate category available. The following table presents the components of our hotel rev-

Room rates will fluctuate depending on anticipated enue as a percentage of our total revenue:

demand levels (e.g. seasonality, weekday vs. weekend stays).

% OF 2005 REVENUES

Rooms revenue. Occupancy and average daily room rate are the major drivers of rooms revenue. The business

mix of the hotel (group versus transient and premium versus discount business) is the key driver of room rates. 60%

Food and beverage revenue. Occupancy and the type of customer staying at the hotel are the major drivers of

food and beverage revenue (i.e., group business typically generates more food and beverage business through

catering functions when compared to transient business, which may or may not utilize the hotel’s restaurants). 30%

Other revenue. Occupancy, the nature of the property (i.e., resort, etc.) and its price point are the main drivers of

other ancillary revenue, such as parking, golf course, spa, telephone, entertainment and other guest services. 7%

22. Hotel operating expenses are approximately 98% of our total operating costs and expenses. The following table presents the

components of our hotel operating expenses as a percentage of our total operating costs and expenses:

% OF 2005 OPERATING

COSTS AND EXPENSES

Rooms expense. These costs include housekeeping, reservation systems, room supplies, laundry services and front

desk costs. Occupancy is the major driver of rooms expense. These costs can increase based on increases in salaries

and wages, as well as the level of service and amenities that are provided. 17%

Food and beverage expense. These expenses primarily include food, beverage and labor costs. Occupancy and

the type of customer staying at the hotel (i.e., catered functions generally are more profitable than outlet sales)

are the major drivers of food and beverage expense, which correlates closely with food and beverage revenue. 26%

Hotel departmental expense. These expenses include labor and other costs associated with the other ancillary revenues

such as parking, golf courses, spas, telephones, entertainment and other guest services, as well as labor and other costs

associated with administrative departments, sales and marketing, repairs and minor maintenance and utility costs. 30%

Management fees. Base management fees are computed as a percentage of gross revenue as set forth in our management

contracts. Incentive management fees generally are paid when operating profits exceed threshold levels established in

our management agreements. 5%

Other property-level expenses. These expenses consist primarily of real and personal property taxes, ground rent,

equipment rent and property insurance. Many of these expenses are relatively inflexible and do not necessarily change

in tandem with changes in revenues at our hotels. 9%

Depreciation and amortization expense. This is a non-cash expense that is relatively inflexible and changes primarily

based on the acquisition and disposition of hotel properties and the level of post-acquisition capital expenditures. 11%

The expense components listed above are based on those property’s market share. For example, a RevPAR penetration

host hotels & resorts 2005

presented in our consolidated statement of operations. It is also index of 100 would indicate that a hotel’s RevPAR is, on aver-

worth noting that wage and benefit costs are spread among var- age, the same as its competitors. A RevPAR penetration index

ious line items, however, taken separately these costs represent exceeding 100 would indicate that a hotel maintains a RevPAR

approximately 50% of our total expenses, making wages and premium in relation to its competitive set, while a RevPAR pen-

benefits the most significant component of our cost structure. etration index below 100 would be an indicator that a hotel is

underperforming its competitive set. One critical component in

Key Performance Indicators this calculation is the determination of a hotel’s competitive set.

We have several key indicators that we use to evaluate the per- Factors that we consider include geographic proximity, as well

24

formance of our business. Revenue per available room, or as the level of service provided at the property. For example, a

RevPAR, is a commonly used measure within the hotel industry hotel located near a convention center might have a competitive

to evaluate hotel operations. RevPAR is defined as the product set that includes other hotels located in close proximity to the

of the average daily room rate charged and the average daily convention center. Additionally, a luxury hotel might include

occupancy achieved. RevPAR does not include revenues from other luxury or upper-upscale hotels in its competitive set but

food and beverage or parking, telephone, or other guest services not economy hotels. Competitive set determinations are highly

generated by the property. Although RevPAR does not include subjective, however, and our methodology for determining a

these ancillary revenues, it is generally considered the leading hotel’s competitive set may differ materially from those used by

indicator of core revenues for many hotels. We also use RevPAR other owners and/or managers.

to evaluate the results of individual hotels between periods and We assess profitability by measuring changes in our operat-

our comparable hotels. See “Comparable Hotel Operating ing margin, which is operating profit as a percentage of total

Statistics” for further discussion of what we consider to be our revenue. Another key profitability indicator we use is hotel

comparable hotels. adjusted operating profit which is a non-GAAP measure, and

RevPAR changes driven predominately by occupancy have which is used to evaluate the profitability of our comparable

different implications on overall revenue levels as well as incre- hotels. Hotel adjusted operating profit measures property-level

mental operating profit than do changes driven predominately results before debt service and is a supplemental measure of

by average room rate. For example, increases in occupancy at a individual property-level profitability. The comparable hotel

hotel would lead to increases in rooms revenues and ancillary adjusted operating profit that we discuss is an aggregation of

revenues, such as food and beverage, as well as additional incre- the adjusted operating profit for each of our comparable hotels.

mental costs (including housekeeping services, utilities and See “Non-GAAP Financial Measures—Comparable Hotel

room amenity costs). RevPAR increases due to higher room Operating Results” for further discussion. We also use, among

rates, however, would not result in these additional room-related other things, FFO per diluted share as a supplemental measure

costs. For this reason, while operating profit typically increases of company-wide profitability. See “Non-GAAP Financial

when occupancy rises, RevPAR increases due to higher room Measures—FFO per Diluted Share” for further discussion.

rates would have a greater impact on our profitability. Each of the non-GAAP measures should be considered by

A related revenue measure for our hotels is the RevPAR investors as supplemental measures to accounting principles

penetration index. The RevPAR penetration index reflects generally accepted in the United States of America, or GAAP,

each property’s RevPAR in relation to the RevPAR for that prop- performance measures such as total revenues, operating profit

erty’s competitive set. We use the measure as an indicator of a and earnings per unit.

23. expired in 2004. One outcome of these negotiations could be

Outlook

potential increases in labor costs (by increased wages, benefits

For 2005, RevPAR for our comparable hotels increased 9.5% as

and/or changes in work rules that increase costs). Any increases

compared to 2004. Improvements in RevPAR at our comparable

in labor costs are likely to increase labor costs in these markets

hotels for 2005 were primarily driven by significant increases in

generally, including at non-union hotels, because of competi-

average room rates, and, to a lesser extent, by increases in occu-

tive pressure to pay market wages. Other potential affects of

pancy. This is a result of a number of positive trends, such as

these negotiations could include temporary disruptions in

strong United States Gross Domestic Product, or GDP, growth,

group bookings and/or hotel operations and it is difficult to

low growth in the supply of new luxury and upper-upscale

predict their outcome at this time, although we do not believe

hotels and the strengthening in the group and transient seg-

the outcome of these negotiations will have a material effect on

ments of our business. As a result of these trends, we expect

our 2006 results of operations.

comparable hotel RevPAR to increase approximately 7% to 10%

Operating margins are also affected by our food and bever-

for full year 2006.

age operations, which represented 30% of our 2005 revenues.

We expect the supply growth of luxury and upper-upscale

During 2005, food and beverage revenue growth at our compa-

hotels to continue to be low for the next two to three years.

rable hotels was 5.6%, with a food and beverage margin

Although always subject to uncertainty, supply growth is

increase of 0.9 percentage points. As the economy continues to

relatively easier to forecast than demand growth due to the long

grow, we expect food and beverage revenue to continue to

permit, approval and development lead-times associated with

increase, in particular catering revenue, which should result in

building new full-service hotels or expanding existing full-

further improvement in our operating margins.

service hotels. Based on data provided by Lodging Econometrics,

We also expect to see improvements in RevPAR and operat-

luxury and upper-upscale hotel supply growth in the top 25

ing margins as we continue our strategy of recycling assets.

U.S. markets is expected to increase by approximately 1.4% and

Over the past two years, we have acquired individual luxury

1.9% in 2006 and 2007, respectively.

and upper-upscale properties in urban and resort/convention

The performance of our portfolio is also significantly affected

destinations, where further large-scale lodging development

by the results of our large hotels, including our convention

typically is limited, and have disposed of individual assets pri-

hotels, the majority of which are located in major urban markets.

host hotels & resorts 2005

marily in suburban and secondary markets. The assets we have

Convention hotels have historically outperformed in the early

acquired have higher RevPAR, higher margins and, we believe,

stages of an industry downturn; however, they also lag the indus-

higher growth potential than those we have sold. Over time,

try in performance in the early stages of recovery. This primarily

these assets should contribute to improvements in overall

is due to the longer booking lead-time for large group business

RevPAR and margins, as well as an increase in the average per

and the need for transient demand in a market to recover to

room replacement cost of our portfolio. The expected RevPAR

more substantial levels given a greater capacity of rooms. In

for the Starwood Portfolio is roughly comparable to the

2005, we saw significant improvement in the operations of our

RevPAR for our current hotel portfolio. 25

convention hotels in certain markets, such as New York City and

During 2005, the average RevPAR penetration index for our

Washington D.C. Our large hotels situated in weaker markets

comparable hotels declined slightly as we continued to work

continue to lag the portfolio, but we are beginning to see signs of

with our managers to optimize the market positioning and

improving market strength in several of these markets including

business mix of our hotels. We believe that this decline in mar-

Boston and to a lesser extent San Francisco. We have also recently

ket share has occurred because:

initiated major projects at our convention hotels in Atlanta and

Orlando with the intention of enhancing their competitive mar- many of our hotels occupy the number one or number

■

ket position and improving performance. We expect increasing two positions in their competitive set and achieve mean-

demand to continue to improve operations at our large conven- ingful RevPAR premiums. In several markets lower-

tion hotels as markets strengthen, which should positively affect ranked hotels have improved their competitive position

margin and RevPAR growth. (through renovation or other means) resulting in a nar-

Operating margins improved in 2005, as the average room rowing of our RevPAR premium.

rate increases at our hotels significantly exceeded the rate of our hotels generally have a higher percentage of their rev-

■

inflation, a trend we expect to continue. Operating margins enues generated by corporate group and corporate tran-

continue to be affected, however, by certain costs, primarily sient customers than many of our competitors and that

wages, benefits, utilities and sales and marketing, which business in the luxury and upper-upscale segment did not

increased at a rate greater than inflation, a trend that we also begin to significantly increase until the second half of 2004;

expect to continue in the near term. We expect utility costs to

we have a significant number of large hotels in our port-

■

increase by over 10% in 2006, although these costs represent

folio, including nine convention hotels with greater than

only approximately 3.6% of our revenues. Additionally, as a

1,000 rooms, which require longer periods of time to

result of the large-scale devastation due to hurricanes this year,

achieve optimal group bookings and business mix.

we expect insurance costs, which were approximately 1% of our

As lodging demand continues to grow and, in particular, as

total costs and expenses in 2005, to increase in 2006 at a rate

corporate group and corporate transient business strengthens,

that significantly exceeds inflation.

we believe our RevPAR penetration index will improve.

In addition, several markets have union contracts that

While we believe the combination of improving demand

expire in 2006, including New York, Hawaii, Chicago, Toronto,

trends and low supply trends in the lodging industry discussed

Boston and Los Angeles. The union contracts in San Francisco

![INTERNATIONAL BRANDS AND MARKETS

upon the expected completion of the acquisition of the starwood portfolio in the second quarter of 2006,

we will have ownership interests in 137 premium-branded hotels, in nine countries and over 50 markets.

[ABOVE] The centuries-old Westin Europa & Regina is an architectural landmark

just steps from Piazza San Marco in Venice, Italy. Named to Conde Nast Traveler’s

2005 Gold List, the hotel offers guests a combination of traditional elegance and

modern technology, while providing the same magnificent views of the Grand

Canal that once inspired Monet. We expect our European joint venture to acquire

this hotel in the second quarter of 2006.

HOST HOTELS & RESORTS

will be the premier hospitality real estate

company. we will own high-quality lodging

assets in prime urban, airport and resort /

convention lo cations. creating value

through aggressive asset management and

disciplined capital allocation to generate

superior performance, we will maximize

shareholders’ returns through a combina-

tion of dividends, growth in funds from

operations and increases to net asset value

per share.

EXISTING MARKETS (AS OF DECEMBER 31, 2005)

MARKETS ACQUIRED AS PART OF THE STARWOOD ACQUISITION

EUROPEAN JOINT VENTURE MARKETS](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)