1. Haryana

Haryana Dadri

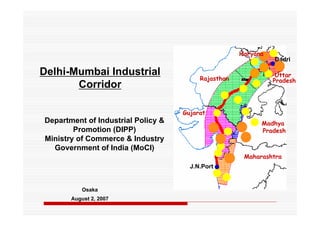

Delhi-Mumbai Industrial Uttar

Rajasthan Pradesh

Corridor

Gujarat

Department of Industrial Policy & Madhya

Promotion (DIPP) Pradesh

Ministry of Commerce & Industry

Government of India (MoCI)

Maharashtra

J.N.Port

Osaka

August 2, 2007

2. Overview

DMIC along Dedicated Freight Corridor (DFC) to optimize on

connectivity offered

MOU between MoCI and METI, Japan in December, 2006

Inter-Ministerial Group formed to evolve the Project Outline

Indo Japanese Task Force to guide the process

First Taskforce Meeting held at Tokyo on 25th May, 2007

Second Task Force Meeting held at New Delhi on July 02, 2007

Third Task Force Meeting at Tokyo on July 23, 2007

Observations of Task Force Meetings incorporated in Concept Paper

Project Outline finalization before Aug 22, 2007 visit of Premier Abe

Feasibility Studies of Phase by December 2008

Project launch January 2008

Completion of Phase I by 2012 coinciding with Western DFC.

2

3. Delhi-Mumbai Industrial Corridor (DMIC)

Haryana The 1483-km long DFC Project to be

commissioned in 2012

Dadri

Uttar Focus is on ensuring high impact

Rajasthan

Pradesh developments within 150km distance

on either side of alignment of DFC

Area under Project Influence is 14%

Gujarat

and population is 17% of the Country

Madhya Pradesh

20% more than Japan

Total Population in the Project

Maharashtra Influence Area : 173.4Mn

J.N.Port

Total Workers in the Project Influence

Area: 68.36Mn

End Terminals

DFC Alignment

As per Census-2001 3

5. Vision for DMIC

“To create strong economic base with globally competitive environment

and state-of-the-art infrastructure to activate local commerce, enhance

foreign investments and attain sustainable development”

Delhi-Mumbai Industrial Corridor is conceived to be developed as “Global

Manufacturing and Trading Hub” supported by world class infrastructure

and enabling policy framework

Project Goals

Double employment potential in five years (14.87% CAGR)

Triple industrial output in five years (24.57% CAGR)

Quadruple exports from the region in five years (31.95% CAGR)

5

6. Project Objectives

Industrial Infrastructure

Developing new industrial clusters

Upgradation of existing industrial estates/clusters in the corridor

Developing Modern Integrated Agro-Processing Zones with allied infrastructure

Development of IT/ITeS Hubs and other allied infrastructure

Providing efficient logistics chain with multi-modal logistic hubs

Physical Infrastructure

Development of ‘Knowledge Hubs’ with integrated approach

Feeder Road/Rail connectivity to ports, hinterlands and markets;

Development of existing Port infrastructure and Greenfield Ports;

Upgradation/ Modernization of Airports;

Setting up Power Generation Plants with transmission facilities;

Ensuring effective environment protection mechanism

Development of integrated townships

6

7. Integrated Corridor Development

The development strategy for the DMIC is based on the competitiveness

of each of the DMIC states :

Holistic approach adopted to identify High Impact/Market Driven Nodes along

the DMIC

Each Node will be self-sustained regions with world class infrastructure and

enhanced connectivity to DFC, Ports, and Hinterlands

Market Driven Nodes are proposed to be in two categories

Investment Regions - Approx. 200 sq km Area (Minimum)

Industrial Areas - Approx. 100Sqkm Area (Minimum)

7

8. Integrated Corridor Development

Criteria for Selection of Investment Region

Each DMIC State to have at least one node to spread economic benefit

Proximity to major urban agglomerations

Potential for Developing Greenfield Ports (or) Augmentation

Availability of land parcels and established industrial base

Criteria for Selection of Industrial Area:

To take advantage of inherent strengths of specific locations

Mineral Resources

Agriculture

Industrial development, and,

Skilled Human Resource base

To spread the benefits of the corridor the project will also seek to link Under-

Developed Regions along the Corridor to Well Developed Regions

8

9. Nodes for Phase-I Development (2008-12)

Haryana

Haryana a Short listed Investment Regions:

Dadri

2 1 1) Dadri-Noida-Ghaziabad (Uttar Pradesh);

3 b Uttar Manesar-Bawal Region (Haryana);

Rajasthan Pradesh 2)

c

3) Khushkhera-Bhiwadi-Neemrana (Rajasthan);

4) Bharuch-Dahej (Gujarat);

Gujarat f 5) Igatpuri-Nashik-Sinnar (Maharashtra);

Madhya 6) Pitampura-Dhar-Mhow (Madhya Pradesh)

d Pradesh

4 6 Short listed Industrial Areas:

a) Meerut-Muzaffarpur (Uttar Pradesh)

5 Maharashtra

J.N.Port

b) Faridabad-Palwal (Haryana)

e c) Jaipur-Dausa (Rajasthan);

d) Vadodara-Ankleshwar (Gujarat);

e) Industrial Area with Greenfield Port at

DFC Alignment Alewadi/ Dighi (Maharashtra);

Investment Region (Min.200SQKM)

f) Neemuch-Nayagaon (Madhya Pradesh)

Industrial Area (Min.100SQKM)

9

10. Phase- II (2012-18): indicative list of projects

(to be finalized after consultations)

Haryana

Haryana 7 Investment Regions:

g Dadri

7) Kundli-Sonepat (Haryana);

Uttar 8) One Region in Gujarat (Location yet to be

Rajasthan Pradesh

h decided);

j 9) Ratlam-Nagda (Madhya Pradesh)

i

Industrial Areas:

Gujarat k

g) Rewari-Hissar (Haryana)*;

p Madhya

8 9 Pradesh h) Ajmer-Kishangarh (Rajasthan);

i) Rajsamand-Bhilwara (Rajasthan);

l

m j) Pali-Marwar (Rajasthan)*;

Maharashtra

J.N.Port

k) Palanpur-Sidhpur-Mahesana (Gujarat)*;

n l) Surat-Navsari (Gujarat);

m) Valsad-Umbergaon with Maroli Greenfield

Port (Gujarat);

DFC Alignment n) Pune-Khed (Maharashtra)

Investment Region (Min.200SQKM)

p) Shajapur-Dewas (Madhya Pradesh);

Industrial Area (Min.100SQKM)

10

11. Components of Each Industrial Node

Industrial Infrastructure

New Industrial Clusters/ Parks/ SEZs

Upgradation of existing industrial estates/clusters

Modern Integrated Agro-Processing Zones with allied infrastructure

IT/ITES Hubs and other allied infrastructure

Efficient logistics chain with integrated multi-modal logistic hubs

Physical Infrastructure

Knowledge Cities / Skill Development Centers with integrated approach

Augmentation of Existing Port infrastructure & Greenfield Port Development;

Upgradation/ Modernization of Airports;

Power Generation Plants with transmission facilities;

Feeder Road/Rail connectivity to ports, hinterlands and markets;

Dovetailed integrated townships catering to investor countries

Effective Environment Protection Mechanism

11

12. Implementation Structure – 3 Tier

An Apex Authoritywith concerned Central Ministers and Chief Ministers

of respective DMIC States as Members;

A Corporate Entity, referred as DMIC Development Corporation

(DMICDC), to coordinate Project Development, Finance and

Implementation;

A Project Management Consultant will work under DMICDC for overall

planning, monitoring and financial advisory services

Project specific Special Purpose Vehicles (SPVs) to implement individual

project components viz. Industrial Areas/SEZs, Roads, Power, Ports,

Airports etc

State-level Committee for coordination between DMICDC, Various State

Govt. Entities and Special Purpose Vehicles (SPVs), wherever necessary.

12

13. Implementation Framework

DMIC Steering Authority

(concerned Central Ministers & Chief Ministers as

Members)

DMICDC

(A Corporate Entity with representation from

Central & State Govt. Agencies, FIIs and DFC)

Master Development Plan, Techno-Economic Feasibility

Studies, Business Plans, Projects Prioritization, Bundling &

Unbundling of Projects to Central/Line Ministries & State Govt

State-level Committee

Project Specific Special Purpose Companies

(SPC)

(For both Central & State Govt Projects viz. Ports,

Airports, Roads, Industrial Areas, Power etc)

Approvals & Clearances (FIPB, NSC, MOEF etc), Monitoring & Commissioning of Projects,

Financing Arrangement etc

13

Project-1 Project-2 Project-3 Project-4

14. Financial Structure of the DMICDC

49 % equity contributed by GOI

51 % equity contributed by Financial Institution(s) and other

Infrastructure organizations

Loans facilitated by DMICDC – as a pass-through

arrangements for specific projects

Project Development Funds contributed by GoJ, Fis and GoI.

14

15. Project Development Fund (PDF)

Magnitude of Project and the high number of sub-project necessitates

creation of a Project Development Fund:

USD 250 mn to be raised as Project Development Fund

PDF to be used specifically for all Project Development Activities to

reach technical and financial closure

PDF to be a revolving fund – expenditure on Project Development to be

recovered from Project SPVs

15

16. Commitment of DMIC States

Each State Government will notify a nodal agency to

coordinate with DMICDC, State level agencies, and SPVs

Would set up the investment regions/ industrial areas in

each state;

Assist in acquiring the land for setting up of

infrastructure & investment regions/industrial areas

Facilitate the clearances required from the State

Government

16

17. Project Specific SPVs

Implementation of specific components of industrial nodes

Projects to be awarded to operators with relevant clearances through

a transparent bidding process

Project Operators to raise finances, to implement the projects

Independent Board of Directors for each SPV

Debts to be raised domestically and externally e.g. through JDRs

Debts could also be raised by DMICDC and passed on to SPVs

17

18. Soft Infrastructure for DMIC

Initiatives for Skill Enhancement

Skill Development Centers planned for each investment region/

industrial areas

Streamlined Administrative Procedures

Each Node could have one or more Special Economic Zone, whose

Head is empowered by the Act to grant necessary clearances

Each State Government will constitute an empowered authority for

each of the investment region/ industrial area

These authorities to have delegated powers, from State

Governments and other , to take decisions locally

Flow of Goods

Government of India has already announced road map for

introducing a ‘Goods and Service Tax’ by 2010 which would replace

central and state taxes into a unified tax regime

18

19. Overview

Project Development Phase :

Estimated Requirement : USD 250 mn

Suggested Structure : Venture Capital Fund

Project Developer : DMICDC

Recovery of Investment : From successful bidders

Contributors : GoJ, FIs and GoI

19

20. Timelines

Concept Report finalized

Appointment of Consultant for preparation of

DPR: July 2007

Joint Presentation of final concept from Hon’ble

PM (India and Japan): August 2007

Finalization of DPR by GoJ/GoI and the

financing plan : December 2007

Project Launch: January 2008

20

22. Key Issues in Project Implementation

The complexity of implementing the DMIC will require rigorous

detailing of all aspects of the project prior to implementation :

Engineering

Environmental

Social

Financial

Contractual, etc

The size of the project will also require to be implemented in phases.

This will be critical in ensuring its sustainability

Given the involvement of multiple Ministries and multiple state

governments an effective framework for co-ordination is critical

The DMIC Project involves an investment of US$ 90 bn with 60-70

different projects. An a priori strategy for the mobilization of finances

to cover each phase of the project will also be critical

22

23. Four-Tier Implementation Structure

An Apex Authority, Headed by the Prime Minister with concerned

Central Ministers and Chief Ministers of respective DMIC States as

Members;

A Corporate Entity, referred as DMIC Development Corporation

(DMICDC), to coordinate Project Development, Finance and

Implementation;

A Project Management Consultant (Joint Consultant) will work under

DMICDC for overall planning, monitoring and financial advisory services

State-level Coordination Entity for coordination between DMICDC,

Various State Govt. Entities and Special Purpose Vehicles (SPVs);

Project specific Special Purpose Vehicles (SPVs) to implement individual

project components viz. Industrial Areas/SEZs, Roads, Power, Ports,

Airports etc

23

24. Project Development Fund (PDF)

Magnitude and importance of Project necessitates creation of Project

Development Fund:

Cost of Project development would be substantial

Funding would need to be accessed from variety of sources-Central and

State Govt., Indian and Foreign investors, bilateral and multilateral

Institutions

Investments to be recovered from PPP projects

USD 250 mn to be raised as Project Development Fund from Govt of India,

Japan and FIs

The PDF to be used specifically for all Project Development Activities to reach

technical and financial closure

PDF ensures availability of finance to get projects off the ground

24

25. SMEs in India - Definition

Manufacture

(i) a micro enterprise, where the investment in plant and

machinery does not exceed twenty five lakh rupees (US

$ 55K);

(ii) a small enterprise, where the investment in plant and

machinery is more than twenty five lakh rupees (US$ 55K)

but does not exceed five crore rupees (US$ 1.1M); or

(iii)a medium enterprise, where the investment in plant and

machinery is more than five crore rupees (US$ 1.1M)but

does not exceed ten crore rupees(US$ 2.2M);

25

26. SMEs in India - Definition

Services

(i) a micro enterprise, where the investment in plant and

machinery does not exceed ten lakh rupees (US $ 22K);

(ii) a small enterprise, where the investment in plant and

machinery is more than twenty lakh rupees (US$ 55K) but

does not exceed two crore rupees (US$ 444K); or

(iii)a medium enterprise, where the investment in plant and

machinery is more than two crore rupees (US$ 444K)but

does not exceed five crore rupees(US$ 1.1M);

26

27. SME Sector produces wide range of products :

Simple consumer goods to highly precision and sophisticated end-

products

leather articles, More sophisticated items

plastics and rubber goods, manufactured by SME

fabrics and sector now include

ready-made garments, television sets,

cosmetics, electronic desk calculators,

utensils, sheet metal microwave components,

components, air conditioning equipment,

soaps and detergents, electric motors,

processed food and auto-parts,

vegetables, drugs and pharmaceuticals.

wooden and steel furniture

and so on.

27

28. SME Sector in India

Key growth engine of the Indian economy

Constitutes 95% of all industrial units in the

country

Contributes more than 40% to domestic

industrial output

Generates 45% of industrial employment

Constitutes about 50% of total manufactured

exports (Direct and Indirect)

Produces diverse range of products (more than

8,000 – consumer items, capital goods and

intermediates)

28

29. SME Sector – Significance in Indian context

SMEs are generally less capital-intensive and more labour-intensive.

Are best suited for countries like India, China and most of the developing

world having abundant supply of low-cost manpower and bountiful natural

resources.

Provide large scale employment, ensure equitable distribution of income

and facilitate effective mobilization of resources of capital and skills, which

would otherwise remain unutilized, particularly in rural and backward areas.

India has already established a niche in SME Development Strategy and

providing excellent support in product development, R&D, financial

instruments, Infra-structure, marketing and export development

Consequently, India is fast emerging as a global hub for labour-intensive

knowledge-oriented business.

29

30. SMEs – The Most Vibrant & Potential Growth Segment

A recent World Bank Report states: “There is now

widespread recognition within India that vibrant

SMEs are potentially a key engine of economic

growth, job creation and greater economic

prosperity”.

10th Plan Document of Govt. of India states:

“Growth as planned will come from a sharp step-up

in industrial and services growth, spurred by SMEs”.

30

31. SME Profile

SSI units : 12.3 million

Employment generated in SSIs : 29.5 million

Production : US $ 100 billion

Exports : US $ 27 billion

SSIs account

Industrial Production : 40%

Exports : 35% (50% of Direct & Indirect)

GDP Share : 7%

31

32. SME Profile

Ownership pattern :

Proprietorships : 78%

Partnerships : 16%

Corporate & Others : 6%

Industrial Units : 96%

Service Enterprises : 3%

Ancillary Units : 1%

32

33. Challenges of SMEs

Access to finance for SME Projects

Lack of adequate working capital

Quality industrial infrastructure (inclusive of Power)

Marketing of products

Technology up gradation and improvement in

quality of products

Delayed payments to SMEs

Sickness and NPA management

33

34. India: Quick facts

• India continues to be the best place to start a business, says a global services

location index by AT Kearney.

• India's foreign exchange reserves stand at US$ 180 billion.

• India has displaced US as the second-most favoured destination for foreign

direct investment (FDI) in the world after China according to an AT Kearney's

FDI Confidence Index

• Poised at a phenomenal growth of 500 per cent, the Indian insurance industry

is expected to reach US$ 60 billion in the next four years.

• Total premium of the general insurance industry grew 16.48 per cent in 2005-

06 to US$ 4.4 billion from US$ 3.78 billion a year earlier.

• India adds about five million telephone subscribers every month. The total

number of subscribers is expected to reach 250 million by the end of 2007.

• The Indian IT-ITeS industry has recorded revenues of US$ 23.6 billion in FY

2005-06.

34

35. India: Quick facts

• India has one of the largest road networks in the world, aggregating 3.34

million kilometers. It comprises 66,590 km of National Highways,

1,28,000 km of State Highways, 4,70,000 km of Major District Roads and

about 26,50,000 km of other District and Rural Roads.

• Indian roads carry about 70 per cent of the freight and 85 per cent of the

passenger traffic.

• India is the Sixth largest crude consumer in the world.

• Estimated to be a US$ 350 billion industry, the Indian retail sector is

growing at a three-year CAGR of 46.64 per cent.

• The travel and tourism sector in India is expected to generate a total

demand of US$ 53,544.5 million of economic activity in 2006, accounting

for nearly 5.3 per cent of GDP and 5.4 per cent of total employment.

• International Iron and Steel Institute (IISI) has ranked India as the

seventh largest steel producer in the world with an overall production of

about 40 million tonnes in 2006.

35

36. India: Quick facts

• India exports US$ 6 billion worth of garments.

• India's gems and Jewellery sector contributed to about 15 per cent of India's

total merchandise exports during 2005-06.

• India is the largest consumer of gold jewellery in the world and accounts for

about 20 per cent of world consumption.

• India is the largest diamond cutting and polishing centre in the world.

• India is the second largest producer of rice and wheat in the world; one of the

largest producers of sugar, sugarcane, peanuts, jute, tea and an assortment of

spices.

• The Indian pharmaceutical industry, consistently growing at 9.5 per cent in the

last 5 years, could zip at 13.6 per cent between 2006 and 2010 and reach a

market size of US$ 9.48 billion by 2010 from its present level of about US$ 5.7

billion.

• Healthcare delivery is one of the largest service-sector industries in India. The

country will spend US$ 45.76 billion on healthcare in the next five years.

36

37. Sectoral FDI Policies

Sectors FDI Policy

Transportation Civil Aviations Services: upto 49% under

automatic route

Road: upto 100% under Automatic route

Shipping / Inland Water Transport: upto 74% under

automatic route

Retail Note permitted except Single Branded product

retailing ( upto 51% under FIPB route)

Insurance upto 26% under automatic route

Finance, Banks:upto 74% under automatic route

Economic NBFC: upto 100% under automatic route with

organization

capitalization norms

37

38. Sectoral FDI Policies

Sectors FDI Policy

Public sector Reserved: Railways Transport, Arms, Atomic Energy,

Defense Aircrafts & Warships, Atomic menial & some

such mineral – No FDI, Tech transfers and vendors

possible

Service Upto 100% under Automatic route for most services.

Some services have entry conditions. Refer FDI

Manual in CD

IT Upto 100% under Automatic route

Manufacturing Upto 100% under Automatic route

Electricity, gas, Upto 100% under Automatic route except Atomic

Energy

water, other utilities

38

39. Sectoral FDI Policies

Sectors FDI Policy

Real estate, FDI up to 100% under automatic route in

Construction townships, housing, built-up infrastructure and

construction-development projects (which would

include, but not be restricted to, housing, commercial

premises, hotels, resorts, hospitals, educational

institutions, recreational facilities, city and regional

level infrastructure)

entry conditions of minimum capitalization and area

-Reference Press Note 2, 2005 at dipp.gov.in

No speculative activities

39

40. Opportunities

Fashion Technology

Information Technology

Design Technology

Health Technology

Bio Technology

Infrastructure sectors

40

41. Fashion Technology - Opportunities

Glamour & Limelight

Creative

High Value Addition

Coverage (Extensive)

Clothes

Dresses

Garments

Textile

41

43. Information Technology : Opportunities

Media

Entertainment

Contents,

Animation,

Games,

Gaming

43

44. Design Technology : Opportunities

Interiors - (Furniture & Furnishing – homes, work places, community, hospitals,

schools, shopping places, recreation, sports)

Exteriors - (Architectural)

Industrial products

Textiles

Electrical appliances

White goods

Leather products

Engineering products

Machinery

Dies and tools

Watches

Jewellery

Hospital equipments

Medical instruments

Electronics and Communication Products and Equipments

44

45. Health Technology : Opportunities

Personal Health Care

Preventive Health Care

Physiotherapy

Monitoring (sensors)

Community Health

Vaccines

Public Health

Surveillance of Health Status (AIDS, Bird Flu etc)

Medical Imaging Technology such as X-ray, Cat scanning,

Computed Tomography Scan (CTs), Magnetic Resource

Images (MRIs), Sonograms etc.

Surgical & Physiotherapy

45

46. Health Technology : Opportunities (contd.)

Personal Health Care

Preventive Health Care

Physiotherapy

Monitoring (sensors)

Community Health

Vaccines

Public Health

Surveillance of Health Status (AIDS, Bird Flu etc)

Medical Imaging Technology such as X-ray, Cat scanning,

Computed Tomography Scan (CTs), Magnetic Resource

Images (MRIs), Sonograms etc.

Surgical & Physiotherapy

46

47. Health Technology : Opportunities (contd.)

Health Information Management

Medical Laboratory Technology

Beauty Care and Wellness

Nursing

Pharmacy Technology

Medical Research Laboratory

Yoga & Naturopathy

Herbal Therapies

Environmental Health

Food Supplements

Food, Inspection and Testing etc.

Medical Waste Management

Hospital Supplies & Staffing Services

47

48. Bio Technology : Opportunities Opportunities

knowledge sector

US $ 365 billion

in 2020.

The biotech industry continues to grow at almost the same rate that it

did in last year. The industry recorded 36.55 percent growth compared

to the previous year’s revised figure of US $ 788 million. In 2003-04,

there were just four companies with revenues in excess of US $ 22

million.

An Ernst and Young study has named India as one of the five

emerging biotech leaders in the Asia Pacific besides Singapore,

Taiwan, Japan and Korea, with mainland China catching up quickly.

The study ranked India third in the region based on the number of

biotech companies (96) in the country, after Australia (228) and China,

including Hong Kong (136).

The above-expected growth will facilitate SMEs to enter into this field

by setting up contract Research Organisations (CROs) and in other

areas to meet the demand of US $ 3.1 billion market of Indian

Pharmaceutical Industry.

With the industry zooming part the US $ 1 billion mark, registering

revenues of US $ 1.07 billion, the sector has achieved a significant

milestone.

48

49. Power

(Estimated investment: USD 60 billion)

Over 67000 MW capacity to be added in the 11th

plan period (2007-08 to 2011-2012)

9 UMPPs to be implemented during the 11th and

12th plans

Transmission capacity augmentation through JVs

for new generation

49

50. Roads

(Estimated investment: USD 49 billion)

NHDP-II: 4569 km, NHDP-VII: $38000 mn.

$103800 mn. State Roads programme are in

NHDP-III: 10000 km addtion

$155200 mn.

NHDP-IV: 20000 km

$66100 mn.

NHDP-V: 6500 km

$98100 mn.

NHDP-VI: 1000 km

$39700 mn.

50

51. Railways

(Estimated investment USD 67 billion)

Dedicated Freight Corridors with PPP sub-projects

envisaging more than USD 7 billion investment for the North

South, East West Corridors alone

Container operations

Rail side warehousing

Logistics Parks

Development of Rail links to Ports

Dedicated rail links for evacuation of specific industrial items

Modernization of Railway Stations

Development of new routes

51

52. Airports

(estimated investment USD 9 billion)

Metro Airport development

through PPP

Greenfield Airports

Concept of Merchant

Airports being examined by

Government

City side development in

24 Non-metro Airports

Provision of Services

within airports

52

53. Ports:

(Estimated investment USD 11 billion)

National Maritime Development All new berths on PPP basis

Programme Gradual transition of old berths

387 port projects to PPP

Compound Annual Rate of Growth

during different Time span

12

10 10.78

ercentage

9.5 9.97

8

6 6.74

5.51

4

P

2

0

1951-2004 1992-2004 2001-2004 2003-2004 2004-2005

54 Years Post Liberalized Last 3 Years Prev ious Year Projected Grow th

Era

Pe riod

53

54. Telecom

Untapped rural potential

with low rural tele-density

of 1.9% which must

increase to 10% by 2012

Almost a million broadband

connections added in

2006-2007. With low

penetration scope for

further increase

Current tele-density 15%

54

55. Urban Infrastructure

Mass Rapid Transit Systems at Mumbai at a capital cost of

about USD 2.5 billion, Hyderabad and Kolkata at about USD 1

billion each, Ahmedabad at about USD 950 million and other

cities

55