Downloaded 303 times

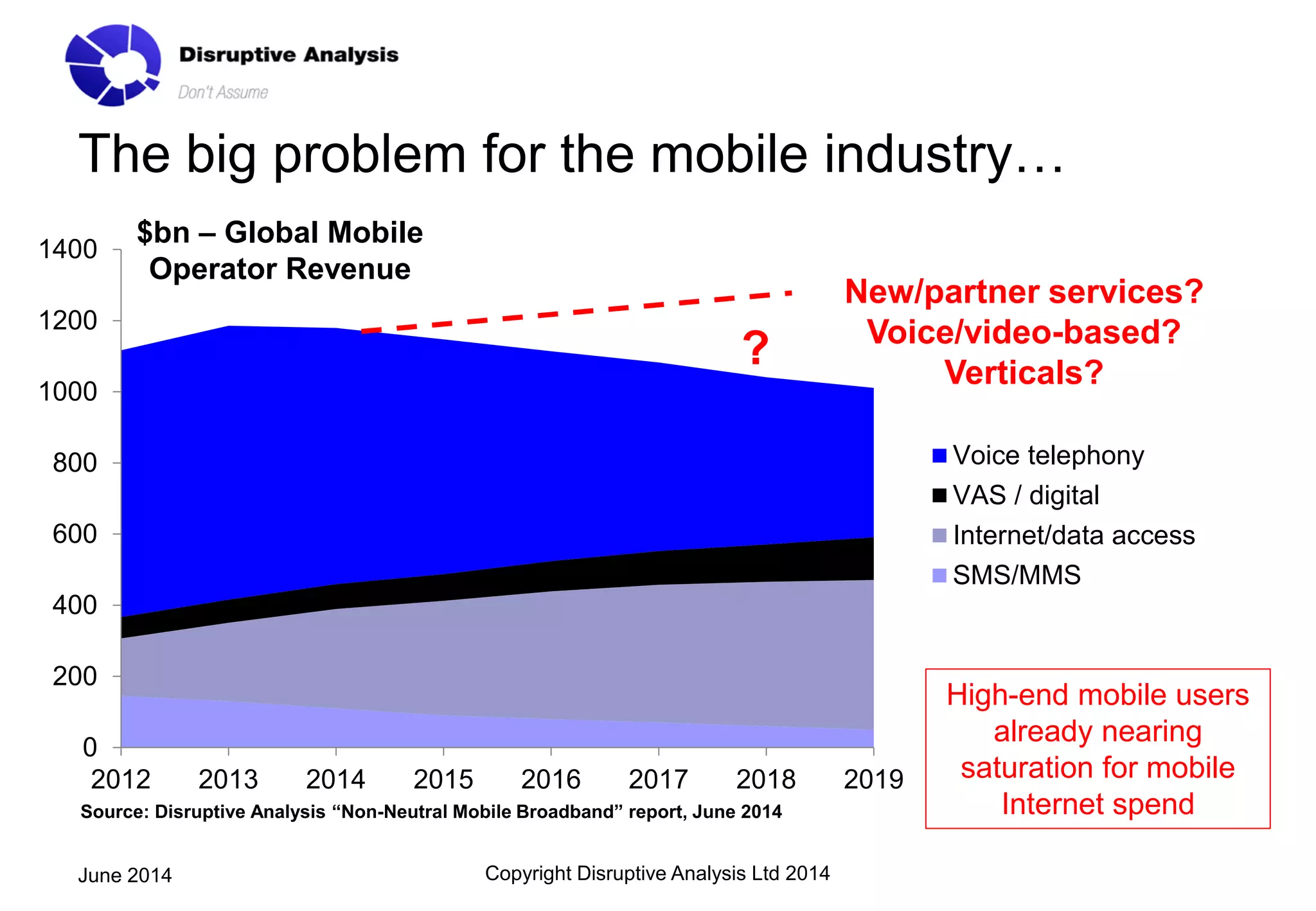

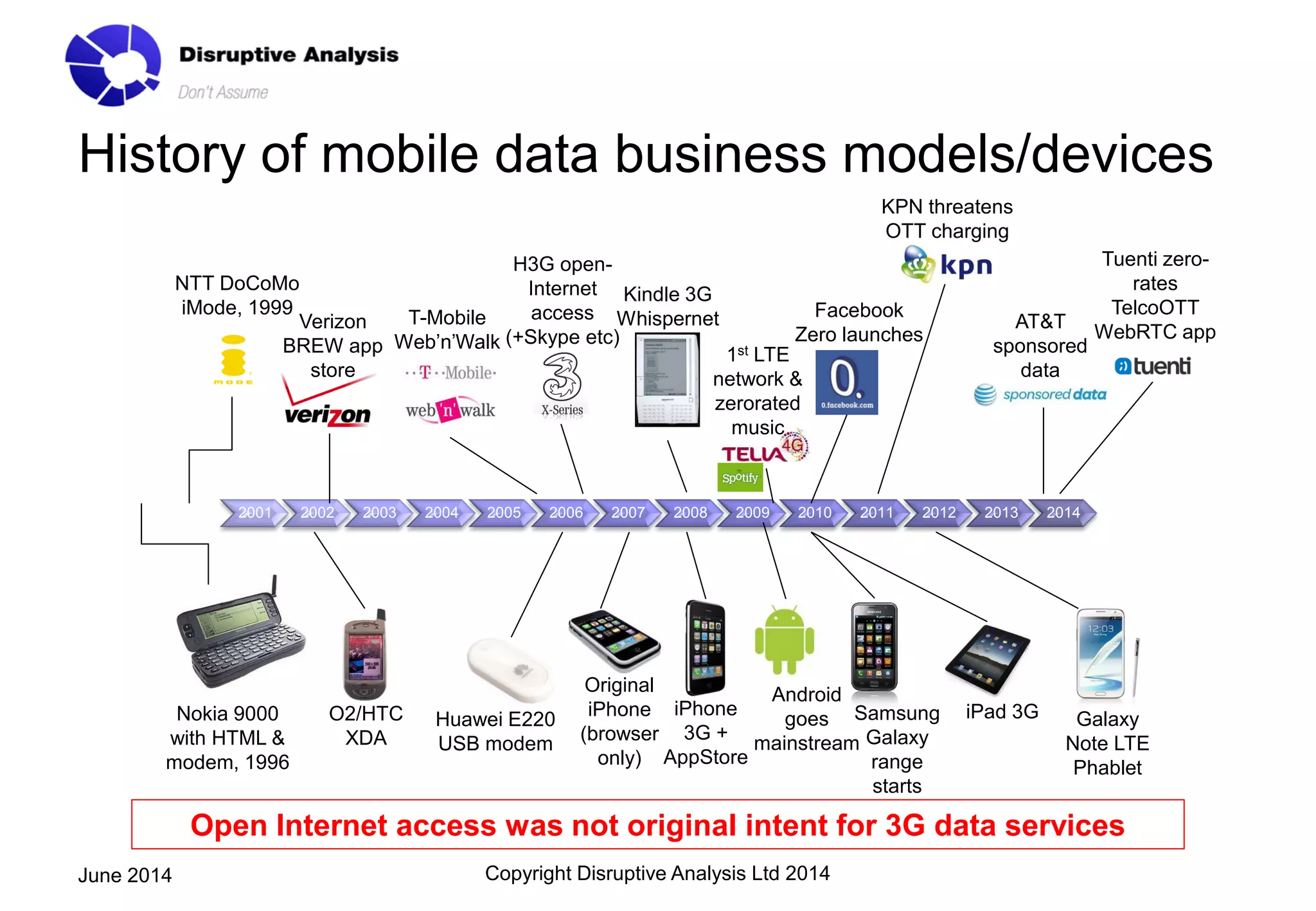

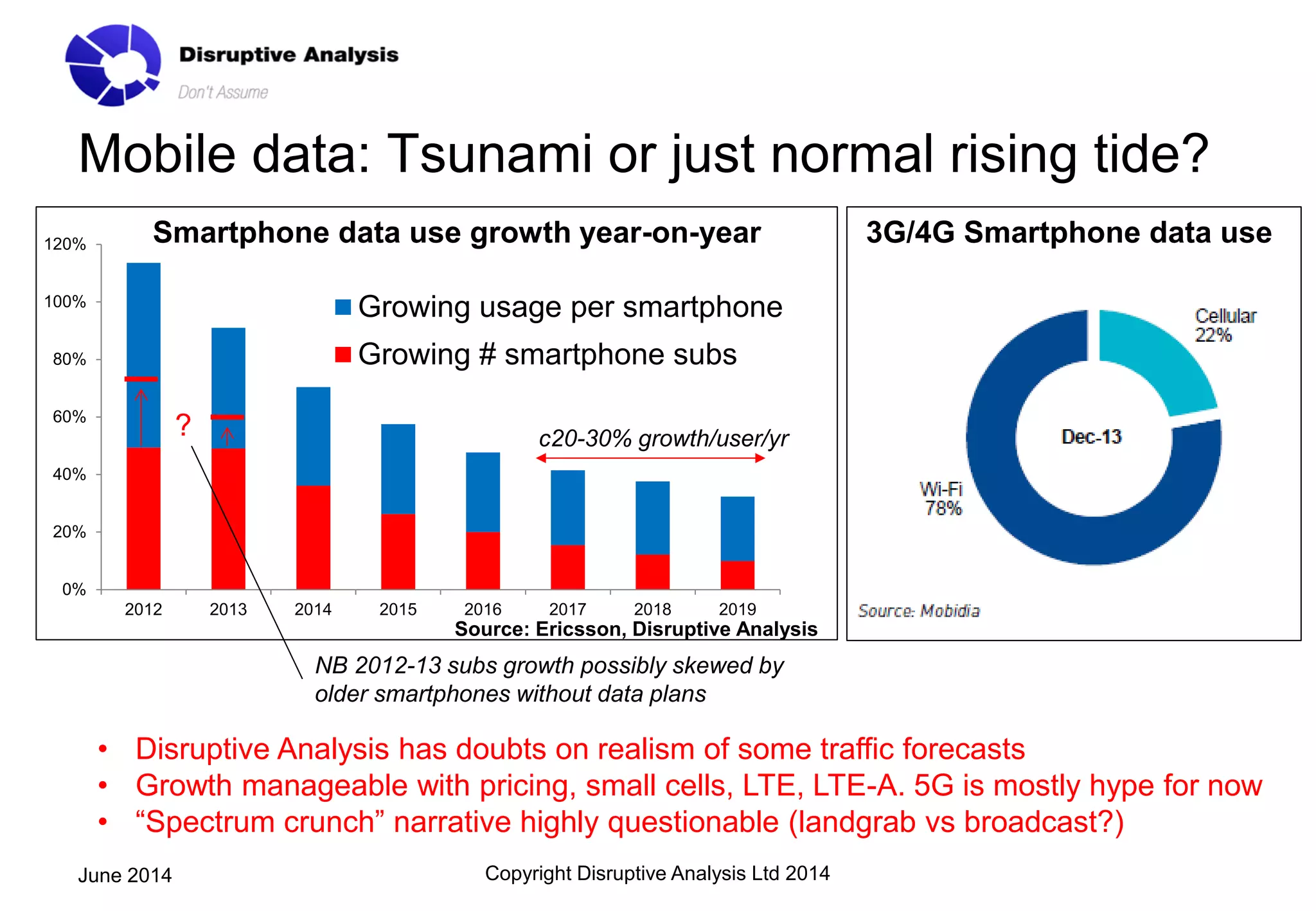

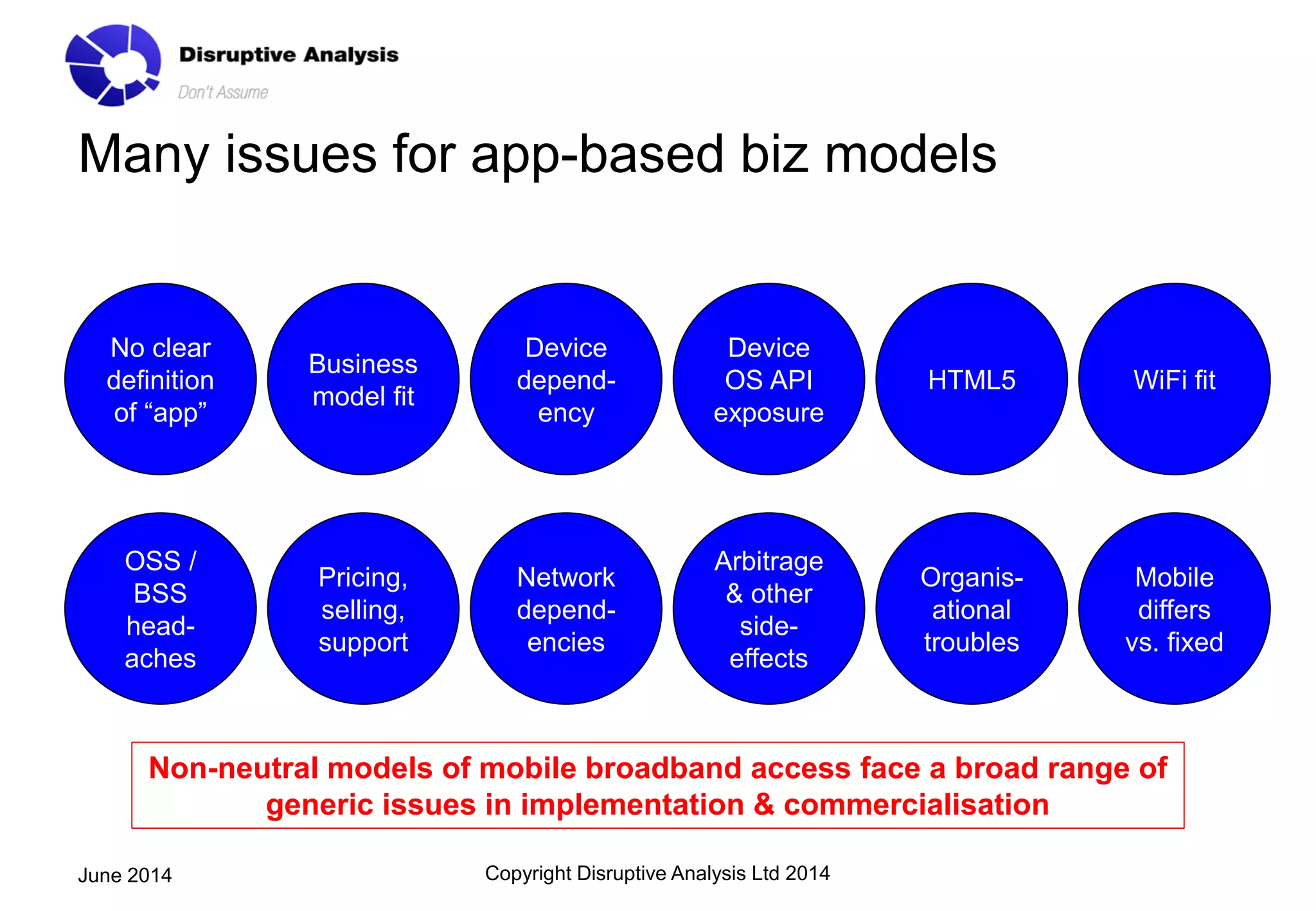

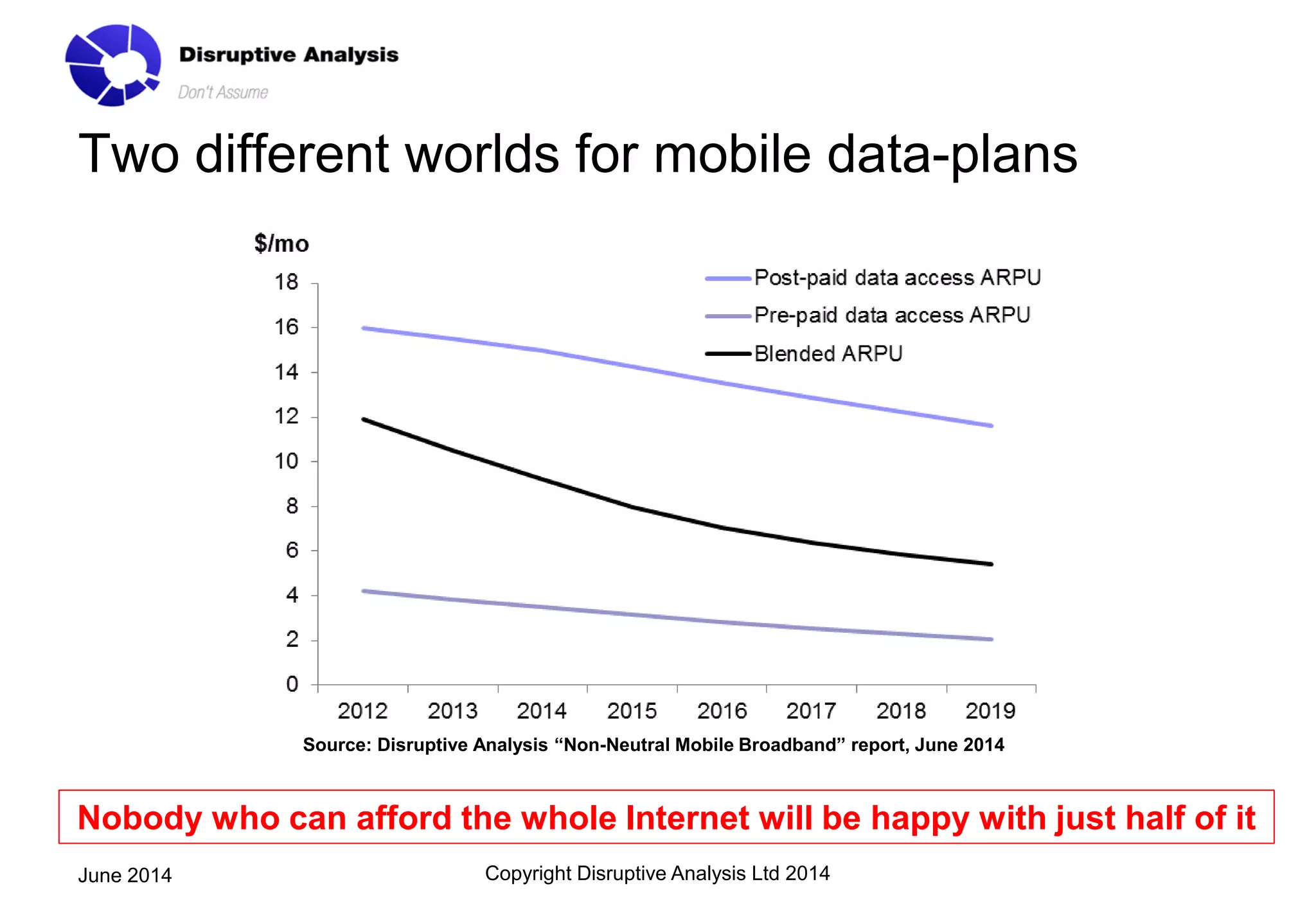

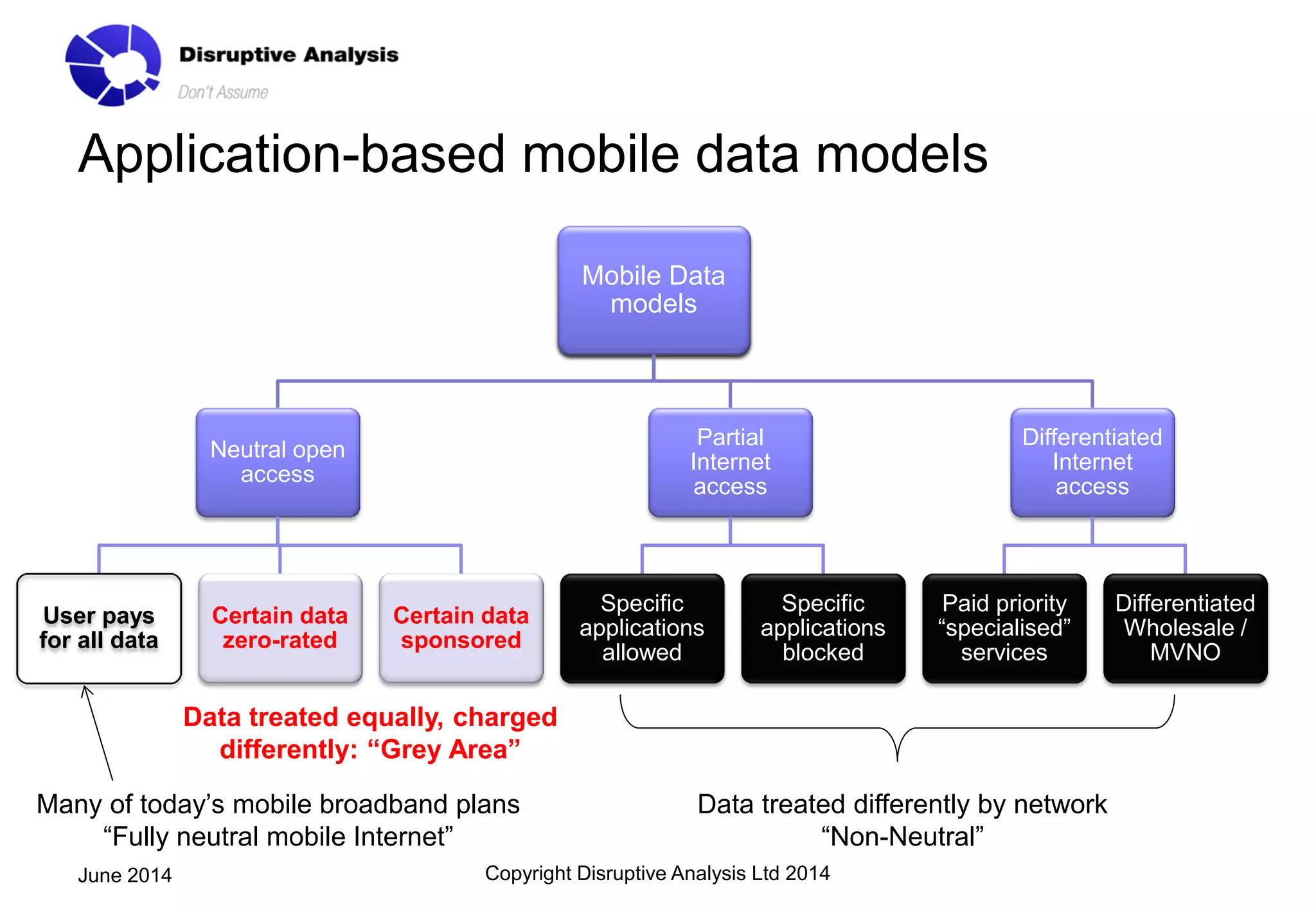

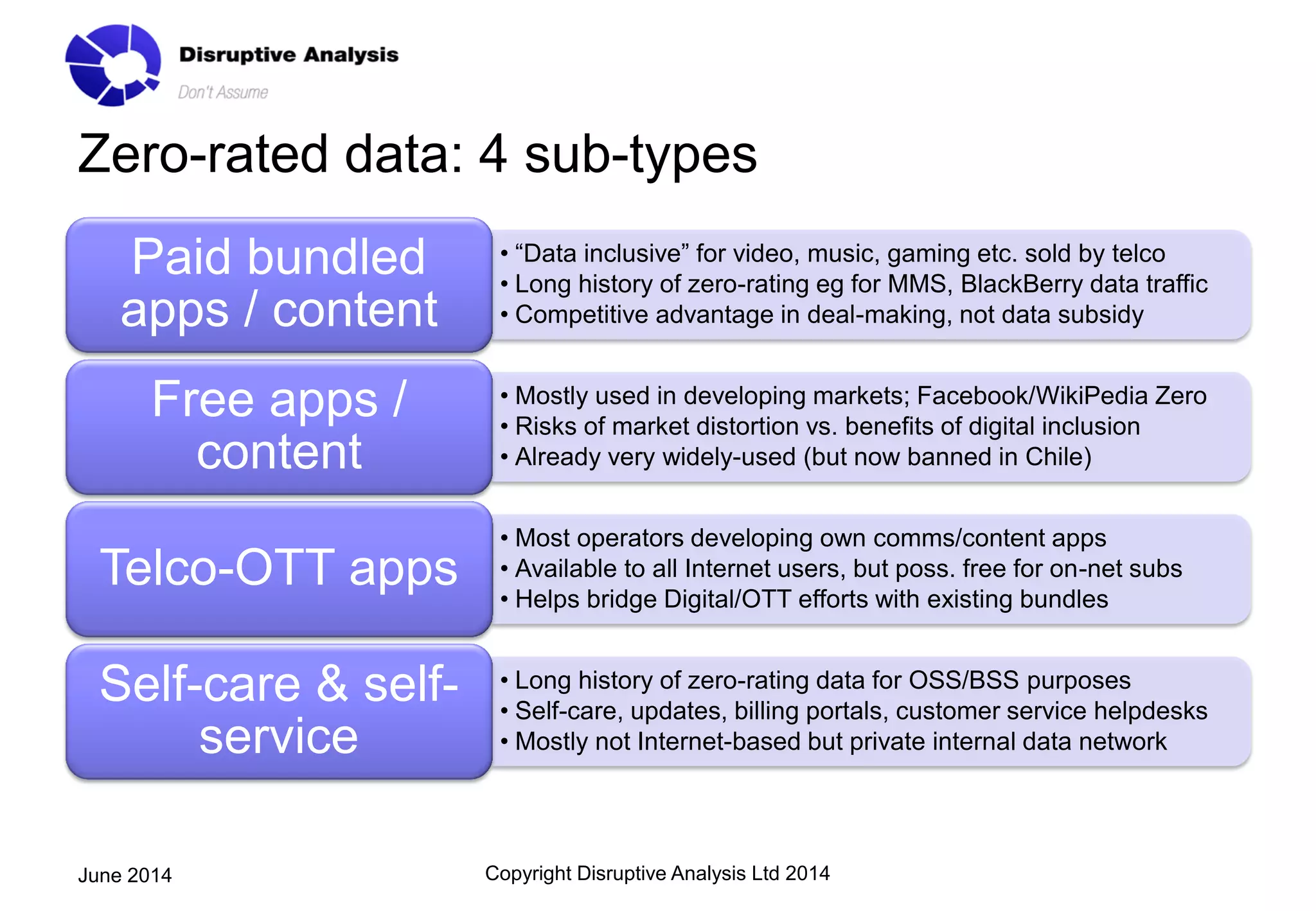

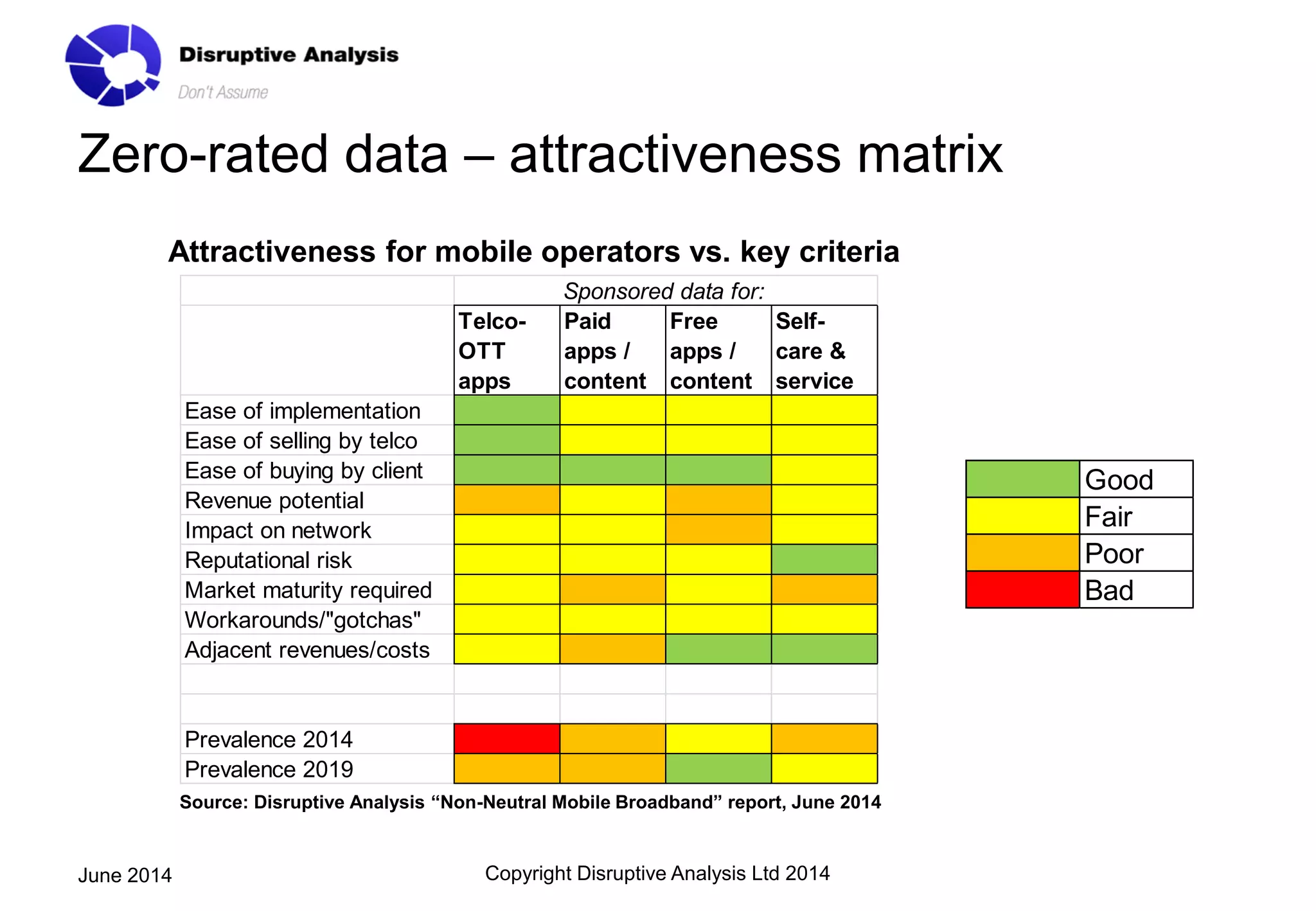

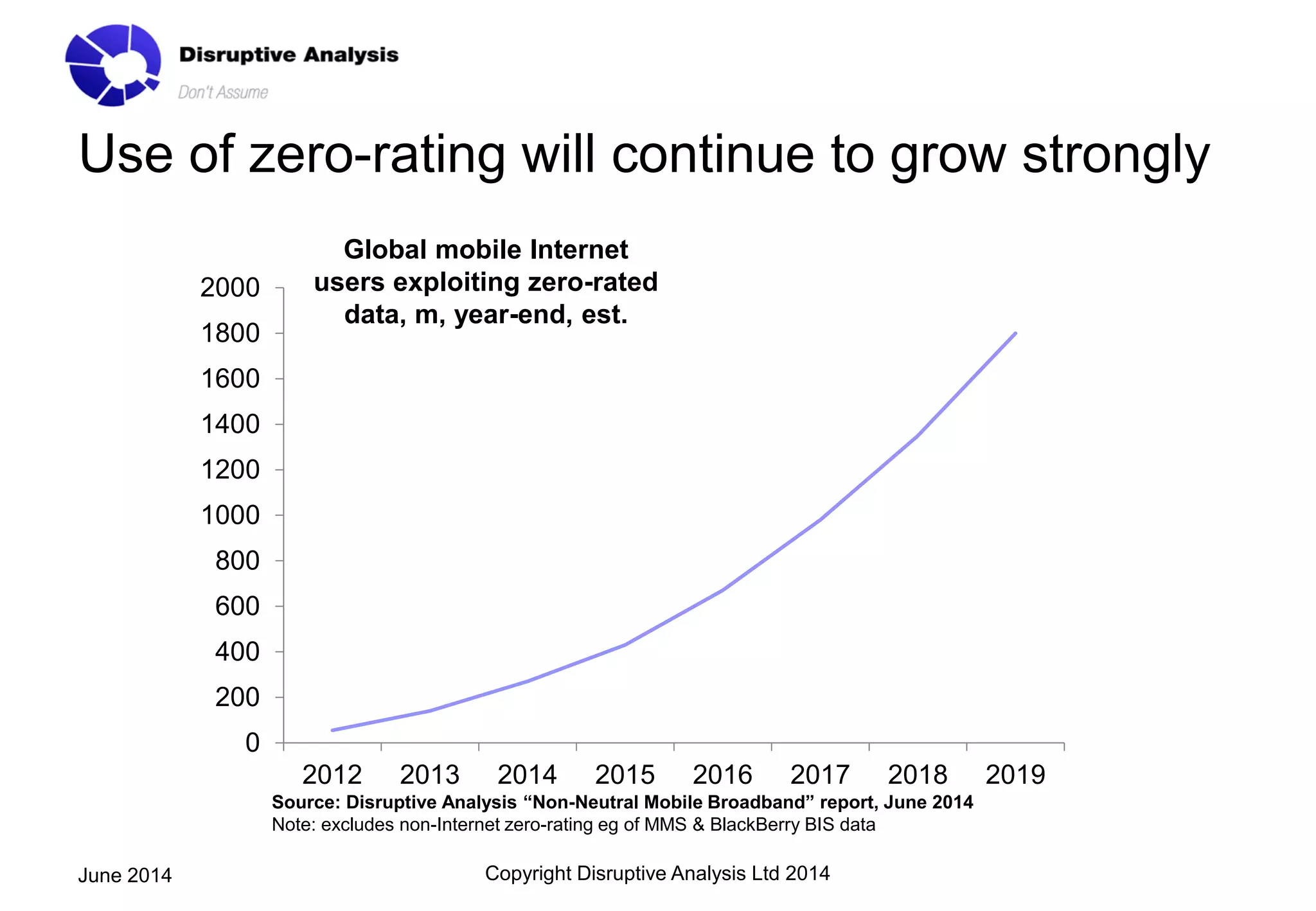

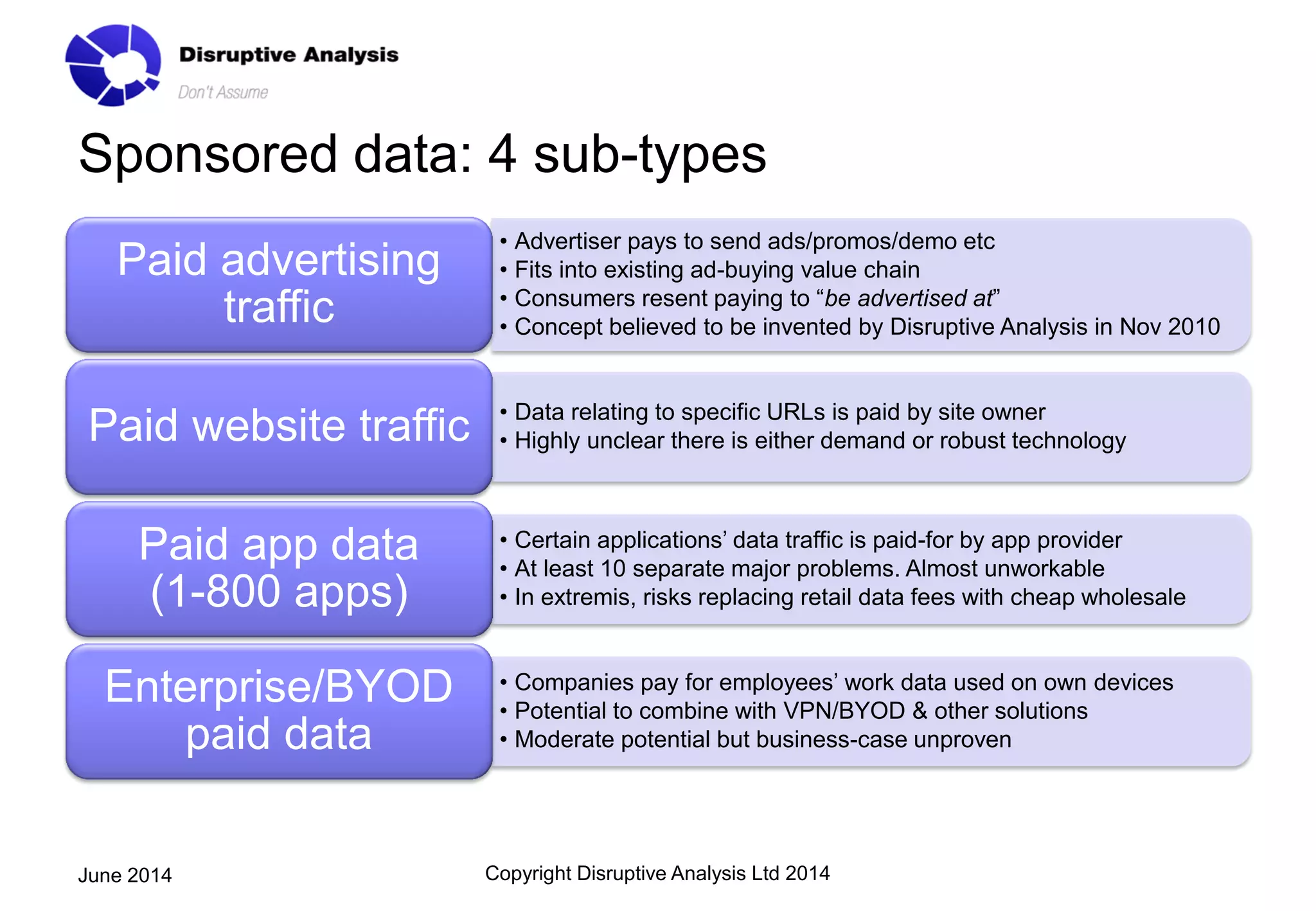

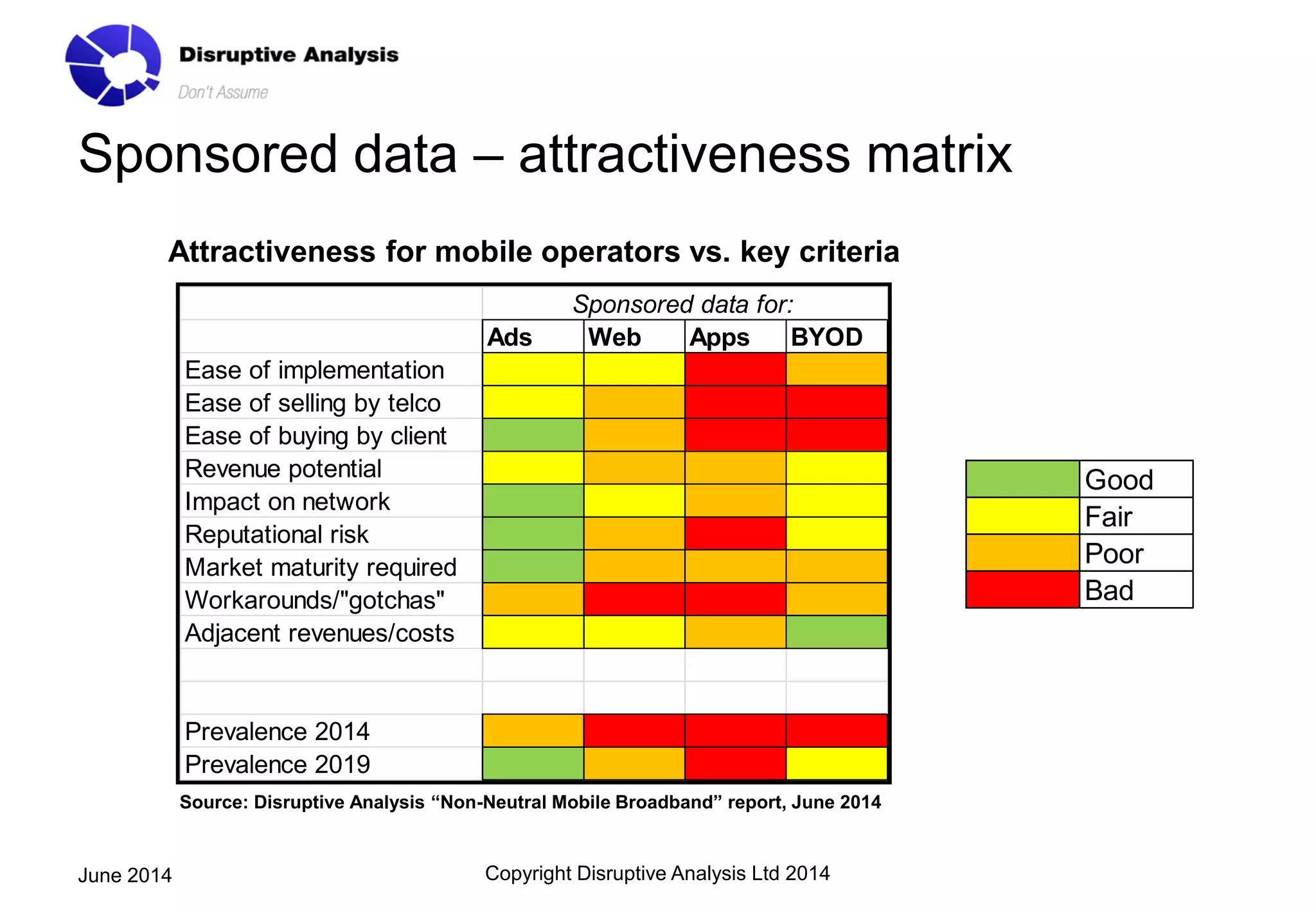

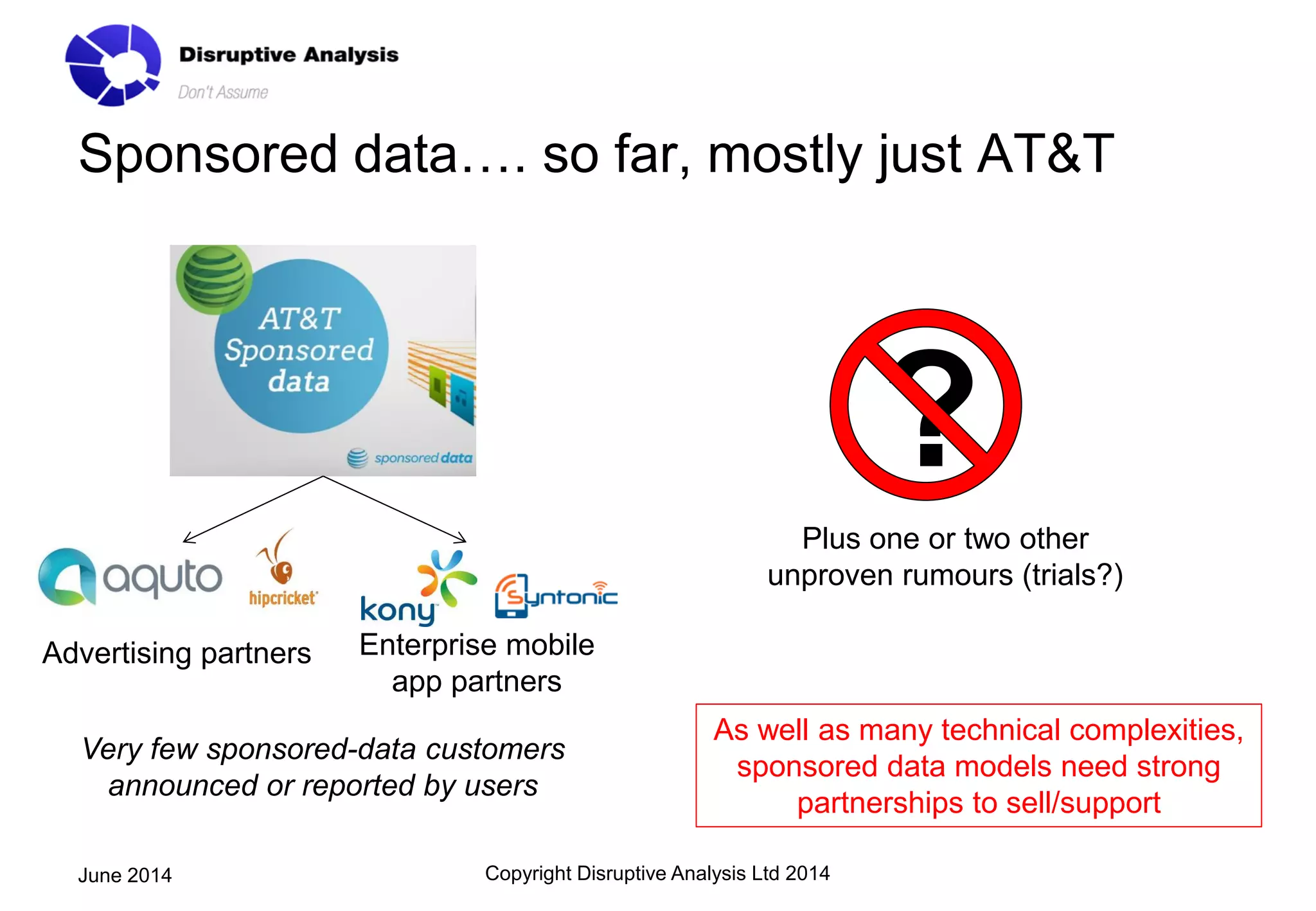

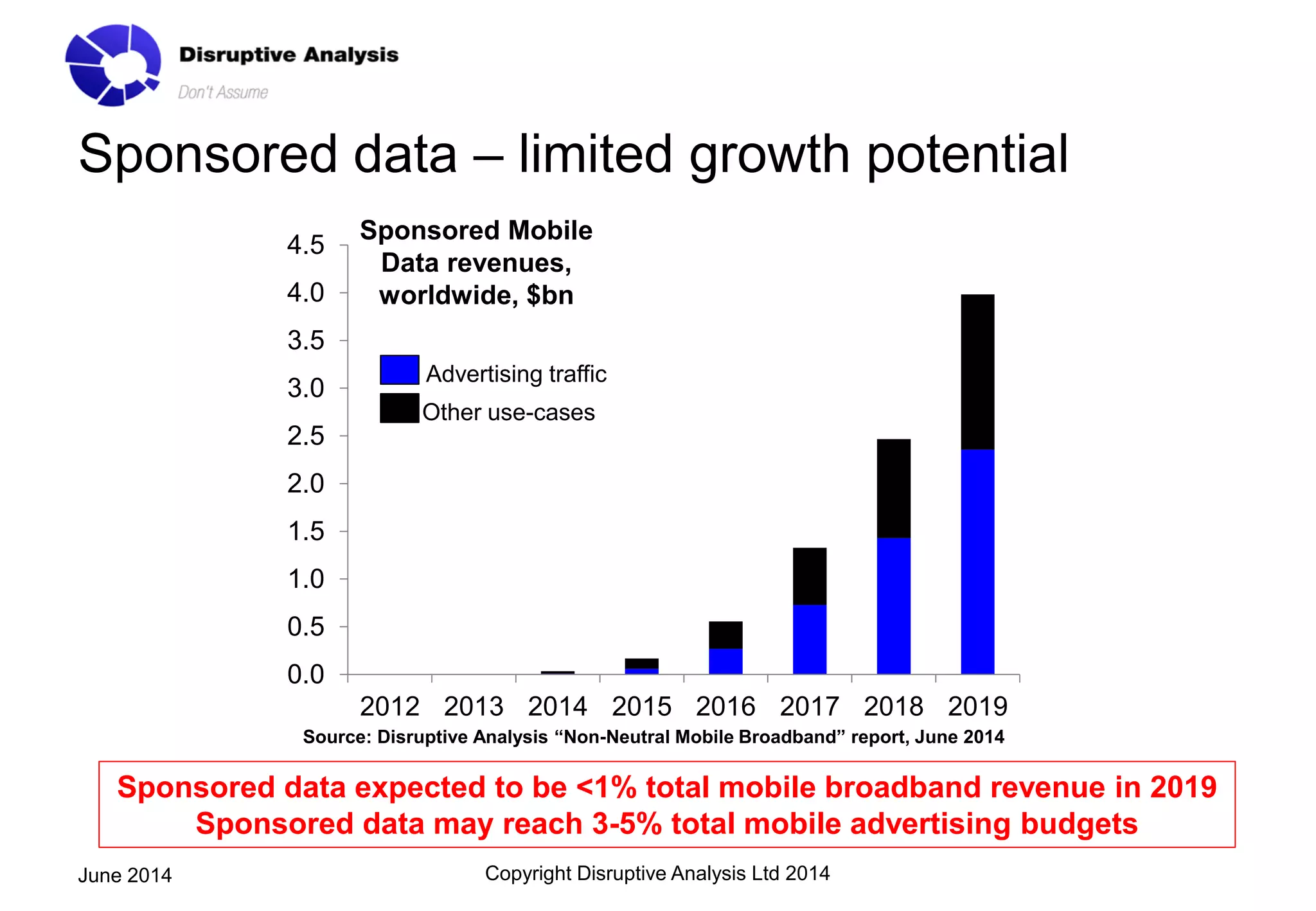

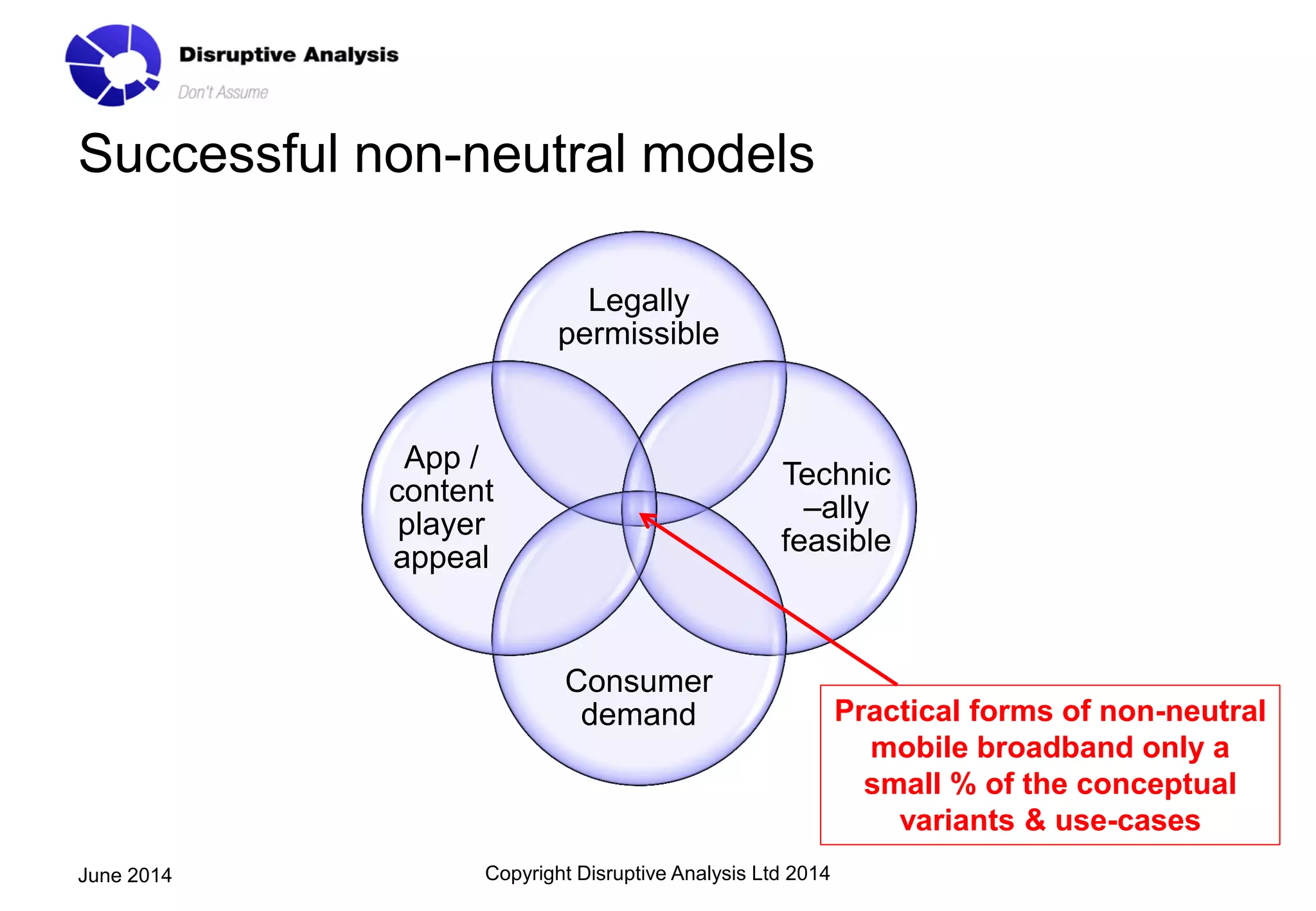

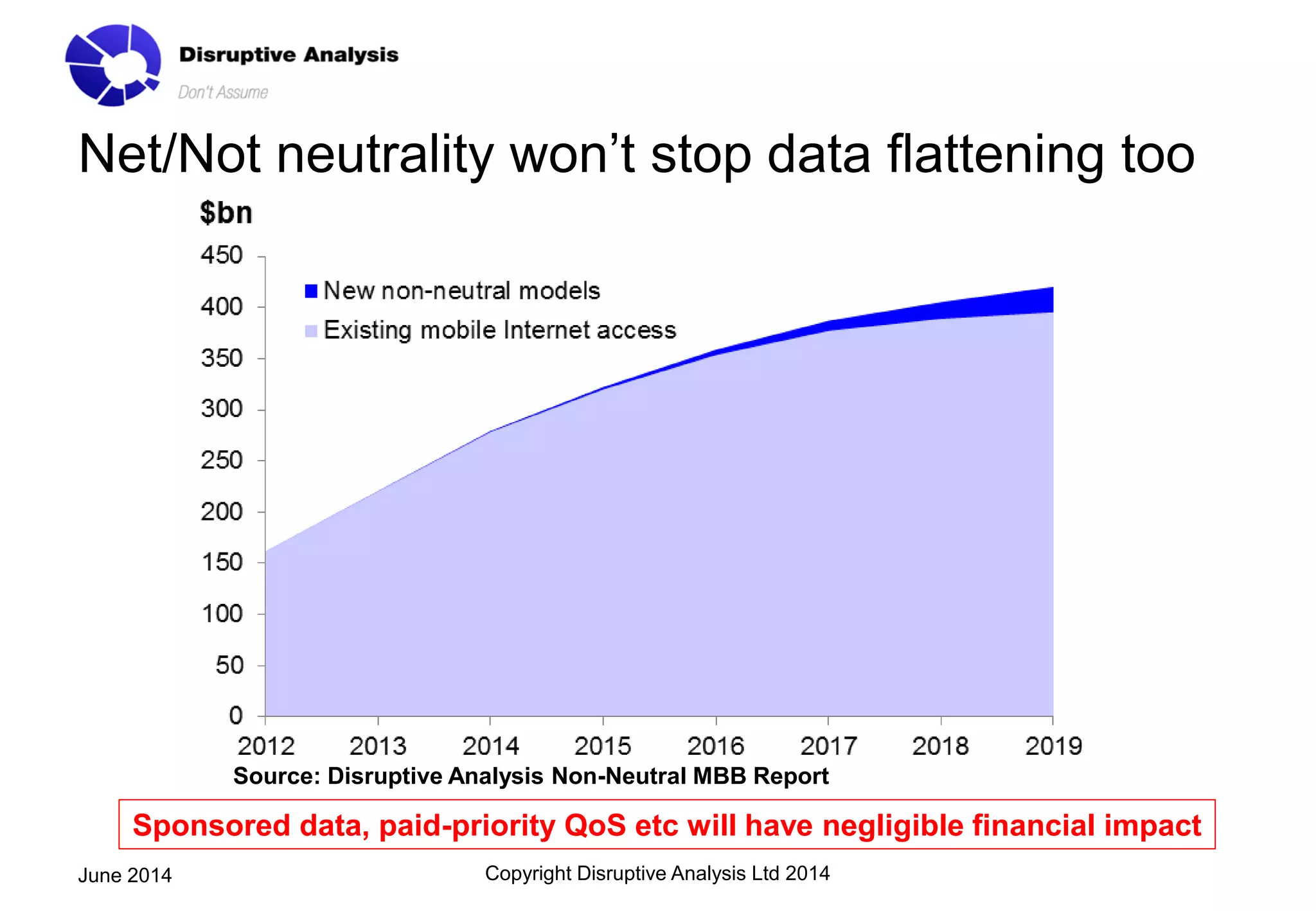

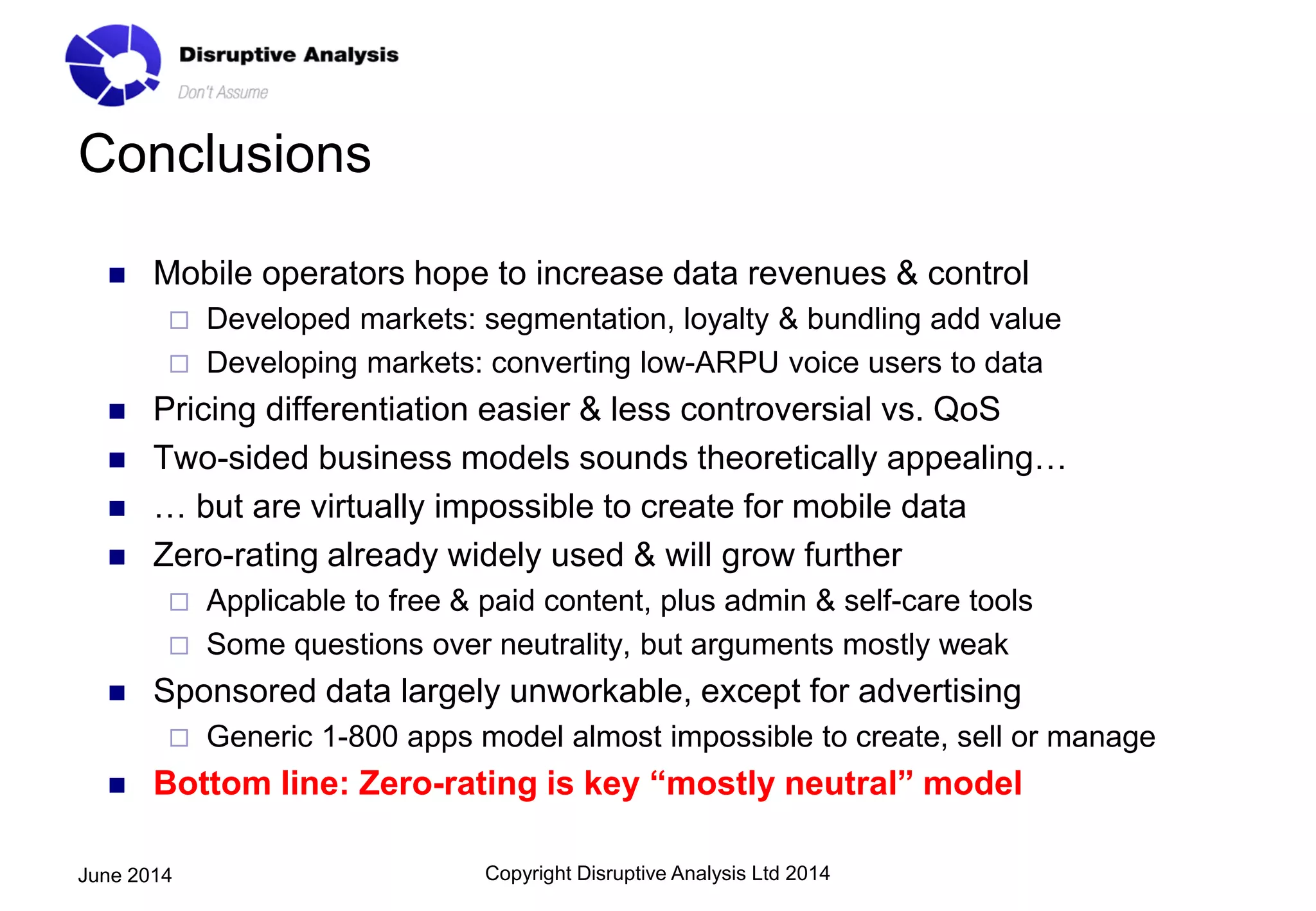

The document discusses mobile broadband business models, focusing on sponsored data and zero-rated charging as strategies for mobile operators to grow revenues and control market segments. It highlights the challenges and prospects of implementing non-neutral broadband models, indicating that while zero-rating is already prevalent and expected to increase, sponsored data faces significant hurdles in execution. Ultimately, the analysis concludes that zero-rating is a key strategy, with limited potential for sponsored data to impact overall revenue.

![Automating ISP Networks Using Ansible and IPAM as a Source of Truth [SoT]](https://cdn.slidesharecdn.com/ss_thumbnails/automatingispnetworksusingansibleandipamasasourceoftruthsot-v25-1-251124105117-d7d4ca24-thumbnail.jpg?width=640&height=640&fit=bounds)