1. A Bi-monthly publication from The Gardner Group August 2012

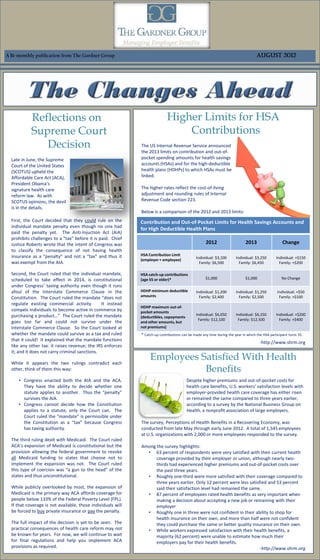

Reflections on Higher Limits for HSA

Supreme Court Contributions

Decision The US Internal Revenue Service announced

the 2013 limits on contribution and out-of-

Late in June, the Supreme pocket spending amounts for health savings

Court of the United States accounts (HSAs) and for the high-deductible

(SCOTUS) upheld the health plans (HDHPs) to which HSAs must be

Affordable Care Act (ACA), linked.

President Obama’s

signature health care The higher rates reflect the cost-of-living

reform law. As with adjustment and rounding rules of Internal

SCOTUS opinions, the devil Revenue Code section 223.

is in the details.

Below is a comparison of the 2012 and 2013 limits:

First, the Court decided that they could rule on the Contribution and Out-of-Pocket Limits for Health Savings Accounts and

individual mandate penalty even though no one had

for High Deductible Health Plans

paid the penalty yet. The Anti-Injuction Act (AIA)

prohibits challenges to a “tax” before it is paid. Chief

Justice Roberts wrote that the intent of Congress was 2012 2013 Change

to classify the consequence of not having health

insurance as a “penalty” and not a “tax” and thus it HSA Contribution Limit

Individual: $3,100 Individual: $3,250 Individual: +$150

(employer + employee)

was exempt from the AIA. Family: $6,500 Family: $6,450 Family: +$200

Second, the Court ruled that the individual mandate, HSA catch-up contributions

scheduled to take effect in 2014, is constitutional (age 55 or older)* $1,000 $1,000 No Change

under Congress’ taxing authority even though it runs

afoul of the Interstate Commerce Clause in the HDHP minimum deductible Individual: $1,200 Individual: $1,250 Individual: +$50

amounts Family: $2,400 Family: $2,500 Family: +$100

Constitution. The Court ruled the mandate “does not

regulate existing commercial activity. It instead

HDHP maximum out-of-

compels individuals to become active in commerce by pocket amounts

purchasing a product…” The Court ruled the mandate Individual: $6,050 Individual: $6,250 Individual: +$200

(deductibles, copayments

Family: $12,100 Family: $12,500 Family: +$400

goes too far and could not survive under the and other amounts, but

Interstate Commerce Clause. So the Court looked at not premiums)

whether the mandate could survive as a tax and ruled * Catch-up contributions can be made any time during the year in which the HSA participant turns 55.

that it could! It explained that the mandate functions

-http://www.shrm.org

like any other tax: it raises revenue; the IRS enforces

it; and it does not carry criminal sanctions.

While it appears the two rulings contradict each

Employees Satisfied With Health

other, think of them this way: Benefits

• Congress enacted both the AIA and the ACA. Despite higher premiums and out-of-pocket costs for

They have the ability to decide whether one health care benefits, U.S. workers’ satisfaction levels with

statute applies to another. Thus the “penalty” employer-provided health care coverage has either risen

survives the AIA. or remained the same compared to three years earlier,

• Congress cannot decide how the Constitution according to a survey by the National Business Group on

applies to a statute, only the Court can. The Health, a nonprofit association of large employers.

Court ruled the “mandate” is permissible under

the Constitution as a “tax” because Congress The survey, Perceptions of Health Benefits in a Recovering Economy, was

has taxing authority. conducted from late May through early June 2012. A total of 1,545 employees

at U.S. organizations with 2,000 or more employees responded to the survey.

The third ruling dealt with Medicaid. The Court ruled

ACA’s expansion of Medicaid is constitutional but the Among the survey highlights:

provision allowing the federal government to revoke • 63 percent of respondents were very satisfied with their current health

all Medicaid funding to states that choose not to coverage provided by their employer or union, although nearly two-

implement the expansion was not. The Court ruled thirds had experienced higher premiums and out-of-pocket costs over

this type of coercion was “a gun to the head” of the the past three years.

states and thus unconstitutional. • Roughly one-third were more satisfied with their coverage compared to

three years earlier. Only 12 percent were less satisfied and 53 percent

While publicly overlooked by most, the expansion of said their satisfaction level had remained the same.

Medicaid is the primary way ACA affords coverage for • 87 percent of employees rated health benefits as very important when

people below 133% of the Federal Poverty Level (FPL). making a decision about accepting a new job or remaining with their

If that coverage is not available, those individuals will employer

be forced to buy private insurance or pay the penalty. • Roughly one in three were not confident in their ability to shop for

health insurance on their own, and more than half were not confident

The full impact of the decision is yet to be seen. The they could purchase the same or better quality insurance on their own.

practical consequences of health care reform may not • While workers expressed satisfaction with their health benefits, a

be known for years. For now, we will continue to wait majority (62 percent) were unable to estimate how much their

for final regulations and help you implement ACA employers pay for their health benefits.

provisions as required. -http://www.shrm.org

2. August 2012

Let Us Take Your Group to the Ball Game!

Enter to win 20 Jacksonville Suns tickets for any remaining home games by simply “Liking” us on

Facebook or “Following” us on LinkedIn between August 1st and August 8th. Follow the links below

to get to our Facebook and LinkedIn Pages. The winner will be announced on August 9th. Good Luck!

www.facebook.com/managingemployeebenefits

www.linkedin.com/company/the-gardner-group---managing-employee-benefits

Outcomes-Based Medical Loss Ratio Rebates

Wellness Incentives The Patient Protection and Affordable Care Act of 2010 includes many

provisions that are continuously being uncovered and defined. One such

provision, the Medical Loss Ratio (MLR) provision, requires health insurers who

A coalition of health care

spend more than a specified percentage of premium dollars on categories of

organizations has produced

spending other than “clinical services and activities designed to improve the

new guidance for the use of

quality of healthcare” (claim payments and medical management costs) to

outcomes-based incentives

rebate a portion of the premium dollars collected to enrollees. The minimum

in employer-sponsored

medical loss ratio is 80% for the small group market and 85% for the large

wellness programs.

group market. This requirement first applied to health insurers for calendar

Outcomes-based incentives year 2011 and, to the extent rebates are required, they will be paid before

provide employees with a August 1, 2012.

financial reward for meeting a specific health target—or a

penalty may be imposed for failure to meet a health The MLR is not calculated at the individual plan or employee level, but based

standard—rather than simply providing an incentive to on the collective experience of all plans in a certain, legally-defined grouping.

participate in the program. Outcomes-based incentives are Employer plans are grouped together based generally on the legal entity that

expected to become more common in the workplace as a issued the coverage (insurance company or HMO), the state where the policy is

result of provisions in the Patient Protection and Affordable issued and the appropriate market segment (large group, small group,

Care Act that encourage their use. individual insurance). It is possible that an employer can have more than one

plan within these groupings.

The new guidance includes the following 10 suggestions for

employers using outcome-based incentives: So, what are employers required to do when they receive the rebate

1. Consider using the four biometric target categories of check?

weight, cholesterol, blood pressure and tobacco use.

First, employers must determine who paid the premiums for the health

2. Factor in potential financial and time burdens for insurance policy. If employees made premium contributions, the employer

employees when determining the specific standard you must determine what portion of the rebate is attributable to participant

are asking them to meet. contributions. The portion of the rebate attributable to participant

3. Consider whether the incentive design is likely to place contributions is usually based on the share or percentage of premiums paid by

a greater economic burden on one race, ethnic group employees.

or other category of employees.

Second, the employer must decide how to use the participant’s share of the

4. Consider incentive designs that are reasonable goals

rebate. There are basically three (3) ways outlined by the Department of

(preferably individualized to the employee) rather than

Labor:

ideal targets applied rigidly to all employees.

5. Offer (as required by law) a reasonable alternative • The rebate can be paid to the participants

standard to employees for whom it would be under a fair and equitable allocation method.

unreasonably difficult to achieve a health standard due For example, an employee with family coverage,

to a medical condition, or who have a medical reason who paid a larger share of premiums, would

that makes it inadvisable for them to do so within the get a larger share of the rebate. The employer

allotted time. can also conclude that only current

participants are allowed to share in the

6. For employees with a medical condition that makes it

rebate. Each employee that

unreasonably difficult to achieve the health standard,

receives a share of the

or medically inadvisable to do so, consider deferring to

rebate will recognize

the views of the employee’s health care provider for

additional taxable

setting and achieving a reasonable alternative standard

income.

or providing a waiver.

7. Consider providing all employees with options for • The employer can apply the entire rebate toward future participant

attaining the incentive, rather than only offering an premium payments (i.e. give a “premium holiday”).

alternative standard to those with a medical

circumstance. • The employer could use the rebate to provide enhanced benefits for

participants.

8. Avoid using a reward or penalty that is so large it

discourages health plan enrollment, denies coverage, The DOL suggests that the second and third options should be used only if

or creates too heavy a financial penalty on individuals distributing payments to employees is not cost effective – for example, if the

who do not satisfy an initial wellness standard. payments are de minimis or if they would give rise to tax consequences to the

9. Consider an incentive design that rewards for progress employee. To avoid having to establish a trust to hold the rebate, the

toward the standard targets, instead of just rewarding employer should distribute the premium credit or enact the benefit

employees who meet the goal. enhancement within three months after receipt of the rebate.

10. Consider strategies that help employees integrate The Minimum Loss Ratio (MLR) mandate contained in PPACA has created a

healthy behaviors into their personal value framework myriad of compliance requirements for health insurers, health plans and

by promoting individual choice, so they are more likely employers. Until the Individual Mandate becomes effective in 2014, the

to sustain healthy behavior changes over time. calculation and distribution of rebate checks is potentially the most costly of

Click here for access to the full article. the PPACA requirements to date. The Gardner Group recognizes the challenges

faced in complying with PPACA and is monitoring legislation, interim rules and

- By Stephen Miller, CEBS operational best practices to provide direction through these legislative

- www.shrm.org nuances.