Lithuanian Economy, No. 2 - March 9, 2012

•

1 like•290 views

Lithuanian Economy, No. 2 - March 9, 2012: Growth surprises this year, but we are not out of the woods yet

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (17)

Similar to Lithuanian Economy, No. 2 - March 9, 2012

Similar to Lithuanian Economy, No. 2 - March 9, 2012 (20)

More from Swedbank

More from Swedbank (20)

Recently uploaded

Recently uploaded (20)

Lithuanian Economy, No. 2 - March 9, 2012

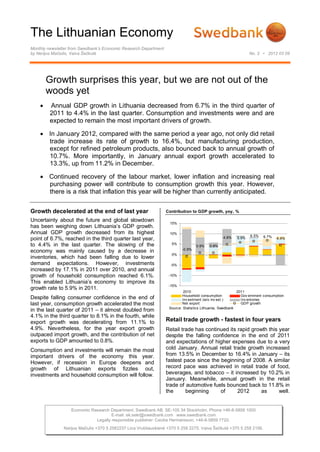

- 1. The Lithuanian Economy Monthly newsletter from Swedbank’s Economic Research Department by Nerijus Mačiulis, Vaiva Šečkutė No. 2 • 2012 03 09 Growth surprises this year, but we are not out of the woods yet Annual GDP growth in Lithuania decreased from 6.7% in the third quarter of 2011 to 4.4% in the last quarter. Consumption and investments were and are expected to remain the most important drivers of growth. In January 2012, compared with the same period a year ago, not only did retail trade increase its rate of growth to 16.4%, but manufacturing production, except for refined petroleum products, also bounced back to annual growth of 10.7%. More importantly, in January annual export growth accelerated to 13.3%, up from 11.2% in December. Continued recovery of the labour market, lower inflation and increasing real purchasing power will contribute to consumption growth this year. However, there is a risk that inflation this year will be higher than currently anticipated. Growth decelerated at the end of last year Contribution to GDP growth, yoy, % Uncertainty about the future and global slowdown 15% has been weighing down Lithuania’s GDP growth. Annual GDP growth decreased from its highest 10% 6.5% 6.7% point of 6.7%, reached in the third quarter last year, 4.8% 5.9% 4.4% to 4.4% in the last quarter. The slowing of the 5% 0.9% 0.8% -0.9% economy was mainly caused by a decrease in 0% inventories, which had been falling due to lower demand expectations. However, investments -5% increased by 17.1% in 2011 over 2010, and annual growth of household consumption reached 6.1%. -10% This enabled Lithuania’s economy to improve its -15% growth rate to 5.9% in 2011. 2010 2011 Household consumption Gov ernment consumption Despite falling consumer confidence in the end of Inv estment (w/o inv est.) Inv entories last year, consumption growth accelerated the most Net export GDP growth Source: Statistics Lithuania, Swedbank in the last quarter of 2011 – it almost doubled from 4.1% in the third quarter to 8.1% in the fourth, while export growth was decelerating from 11.1% to Retail trade growth - fastest in four years 4.9%. Nevertheless, for the year export growth Retail trade has continued its rapid growth this year outpaced import growth, and the contribution of net despite the falling confidence in the end of 2011 exports to GDP amounted to 0.8%. and expectations of higher expenses due to a very Consumption and investments will remain the most cold January. Annual retail trade growth increased important drivers of the economy this year. from 13.5% in December to 16.4% in January – its However, if recession in Europe deepens and fastest pace since the beginning of 2008. A similar growth of Lithuanian exports fizzles out, record pace was achieved in retail trade of food, investments and household consumption will follow. beverages, and tobacco – it increased by 10.2% in January. Meanwhile, annual growth in the retail trade of automotive fuels bounced back to 11.8% in the beginning of 2012 as well. Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000 E-mail: ek.sekr@swedbank.com www.swedbank.com Legally responsible publisher: Cecilia Hermansson, +46-8-5859 7720. Nerijus Mačiulis +370 5 2582237 Lina Vrubliauskienė +370 5 258 2275. Vaiva Šečkutė +370 5 258 2156.

- 2. The Lithuanian Economy Economic Research Department, Swedbank No. 2 • 2012 03 09 Accompanying the rapid growth of retail trade, increase in efficiency as the manufacturing sector confidence has also bounced back. From has been expanding. December to February, consumer confidence In the last quarter of 2011 industrial production and increased from -30 -23; from January to February, manufacturing (at constant 2005 prices) already retail trade confidence jumped from -27 to -13. exceeded the levels achieved at the end of 2007. For 2012, lower inflation and--for the first time in Industrial production is still 4% and manufacturing three years--increasing real purchasing power will 4.9% below a pre-crisis peak reached in the second contribute to consumption growth. Although quarter of 2008, but the gap is likely to be consumers’ inflation expectations remain elevated, eliminated this year. high unemployment and slower global growth and uncertainty will have lower pressure on Industrial production at constant 2005 prices, m LTL consumption and prices in Lithuania. We forecast average annual inflation to be 2.5% this year, but 14000 there is a significant upside risk related to recent 12000 developments in the commodities market. Future developments in international commodity, oil and 10000 food markets will be the most important driver of 8000 inflation in Lithuania. 6000 Annual change in retail trade, %, and confidence indicators 4000 20 2000 10 0 0 2007 2008 2009 2010 2011 Manuf acturing (w/o ref ined prod.) Ref ined petroleum products -10 Electricity and water Mining and quarry ing -20 Source: Statistics Lithuania -30 For now, industrial producers do not expect foreign -40 demand to shrink and plan to produce more. From December to February, industrial production -50 expectations in regard to exports increased from - 2010 2011 2012 Retail trade conf idence 12 to 16, while production expectations rose from - Consumer conf idence 13 to 7. Retail trade (excl. motor v ehicles), y oy Retail sale of f ood, bev erages and tobacco Automotiv e f uel Annual changes in industrial production, manufacturing and Source: Statistics Lithuania, Swedbank confidence Economic sentiment has been increasing for the 35 last couple of months and reached -6 in February. 30 The most significant bounce back after the end of 25 2011 was observed in the retail trade sector. 20 15 However, positive tendencies have been evident in 10 all sectors. Unemployment expectations have been 5 decreasing this year as well. 0 -5 Industrial production expanded rapidly -10 -15 after contracting at the end of last year -20 -25 Manufacturing, excluding refined petroleum 2010 2011 2012 products, continued increasing its annual pace of Industrial conf idence growth and in January reached 10.7%. This rapid Industry , y oy Production expectations growth pulled total industry from a 2.1% contraction Assesment of stocks Manuf acturing (excl.ref ined prod.), y oy in December to 4.0% growth in January. Other Source: Statistics Lithuania industrial sectors (except for manufacturing) contracted for the second consecutive month in Therefore, manufacturing should be able to sustain January. Mining and quarrying contracted by 6.8%, its growth and regain pre-crisis peaks this year, refined petroleum products by 7.7%, and electricity however, risks related to developments in the global and water supply by 2.3%. The lower production of economy remain. Stagnating reforms in Europe, electricity and water may indicate a continued 2 (4)

- 3. The Lithuanian Economy Economic Research Department, Swedbank No. 2 • 2012 03 09 renewed tension in financial markets and expensive Unemployed can purchase those two times oil can significantly dampen the recovery. cheaper. While, over this period, registered long- term unemployment did decrease a bit, registered Better producer expectations also suggest that youth unemployment rose from 6.8% to 7.3%. export growth should keep pace in the short run. In January the nominal growth of exports increased to The issue of the long-term unemployed should be 13.3%, from 11.2% in December. Growth of exports addressed by improving retraining programs. Such of goods produced in Lithuania in January slowed programs would respond better to real market down marginally to 8.2%, from 8.9% in December. needs if there were more cooperation between the For the third month in a row, exports were Lithuanian Labour Market Exchange, currently increasing faster than imports; this trend was responsible for programs to retrain the unemployed, probably influenced by businesses slashing their and business, which could contribute by indicating inventories. Growth of export of goods and services its labour market needs and adapting retraining is expected to lose pace later this year – we programs to the latest trends. forecast 4% real growth for 2012, compared with However, youth unemployment sometimes can be 13.7% growth in 2011. exaggerated, as the activity rate in the age group of Labour market recovers slowly 15-24- year old is only about 30% and, therefore, the absolute number of unemployed young people The total unemployment rate fell by 3.2 percentage is not as big as it may seem – 32,000 according to points to 13.9% in the last quarter of 2011, the latest data from the Lithuanian Labour Market compared with the same period in 2010. However, Exchange. Of these, 59.3% do not have any long-term unemployment declined by only 1.4 qualifications, which means that the number of percentage points, to 7.1%, and youth qualified youth not able to find jobs is about 13,000. unemployment by 0.4 percentage point, to 32% in Nevertheless, this problem has to be addressed in that period. country with such high emigration rates, and Unemployment rate, wage growth dwindling labour force, as Lithuania. Therefore, the education system should be changed to make it 40% more responsive to labour market needs and to 35.9% 37.1% 35% 35.5% 34.1% 33.6% prepare specialists who would be better able to 32.4% 31.7% 32.0% adapt in the labour market.2 30% 25% A 1.5% decrease in net real wages in 2011 20% 18.1% 18.3% 17.8% suggests that the household consumption increase 17.1% 17.2% 15.6% 14.8% 13.9% 15% came at the expense of lower savings. This year, 7.4% 7.5% 8.5% 8.7% 8.0% 8.0% 7.1% however, household consumption growth should 10% 6.1% decelerate even though real net wage growth 5% should be positive and real wage bill growth 0% increases. This is due to more cautious behaviour -5% of households this year. -10% 2010 2011 Data at the beginning of the year on recovering Unemploy ment Youth unemploy ment business and consumer confidence, as well as Long-term unemploy ment Gross nominal wage Net real wage manufacturing and retail trade, suggest that Source: Statistics Lithuania Lithuania’s economy is nowhere near a recession From the third quarter of 2011 to the last quarter the or stagnation. However, the uncertainty and risks job vacancy rate decreased from 1.1% to 0.6%. related to the developments in the euro zone However, this fall may be a temporary effect of economy remain and should be observed very decreased confidence at the end of last year. closely. No further significant improvement in the labour market was seen in the beginning of 2012. Vaiva Šečkutė According to the Lithuanian Labour Market Nerijus Mačiulis Exchange, registered unemployment1 increased from 11.0% on January 1 to 11.6% on February 1. However, this might have been a consequence of increased price of business certificates from 2012. 2 Read more about possible measures to address youth unemployment and the labour market in Swedbank 1 The ratio of registered unemployed to total f Analysis No. 2. “To promote growth, Lithuania’s labour working-age population market needs more efficiency and flexibility” 3 (4)

- 4. The Lithuanian Economy Economic Research Department, Swedbank No. 2 • 2012 03 09 Swedbank Economic Research Department Swedbank’s monthly newsletter The Lithuanian Economy is published as a service to our SE-105 34 Stockholm customers. We believe that we have used reliable sources and methods in the preparation Phone +46-8-5859 1028 of the analyses reported in this publication. However, we cannot guarantee the accuracy or ek.sekr@swedbank.com completeness of the report and cannot be held responsible for any error or omission in the www.swedbank.com underlying material or its use. Readers are encouraged to base any (investment) decisions on other material as well. Neither Swedbank nor its employees may be held responsible for Legally responsible publisher losses or damages, direct or indirect, owing to any errors or omissions in Swedbank’s Cecilia Hermansson, +46-8-5859 7720. monthly newsletter The Lithuanian Economy. Nerijus Mačiulis, +370 5 2582237. Lina Vrubliauskienė +370 5 258 2275. Vaiva Šečkutė, +370 5 258 2156. 4 (4)