Uae-NO1 Kala Jadu specialist Expert in Pakistan kala ilam specialist Expert i...

22 May Daily market report

1. Page 1 of 7

QE Intra-Day Movement

Qatar Commentary

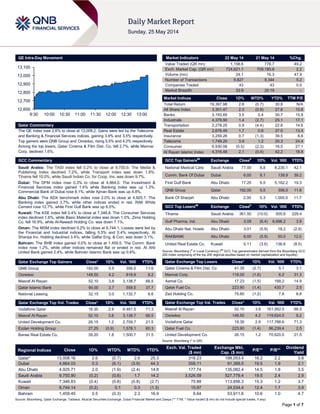

The QE index rose 2.6% to close at 13,008.2. Gains were led by the Telecoms

and Banking & Financial Services indices, gaining 3.9% and 3.5% respectively.

Top gainers were QNB Group and Ooredoo, rising 5.5% and 4.2% respectively.

Among the top losers, Qatar Cinema & Film Dist. Co. fell 2.7%, while Mannai

Corp. declined 1.6%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.2% to close at 9,750.9. The Media &

Publishing Index declined 7.2%, while Transport index was down 1.9%.

Tihama fell 10.0%, while Saudi Indian Co. for Coop. Ins. was down 9.7%.

Dubai: The DFM index rose 0.3% to close at 4,864.0. The Investment &

Financial Services index gained 1.4% while Banking index was up 1.3%.

Commercial Bank of Dubai rose 8.1%, while Ajman Bank was up 4.8%.

Abu Dhabi: The ADX benchmark index rose 2.0% to close at 4,925.7. The

Banking index gained 3.7%, while other indices ended in red. RAK White

Cement rose 12.7%, while First Gulf Bank was up 6.5%.

Kuwait: The KSE index fell 0.4% to close at 7,346.8. The Consumer Services

index declined 1.6%, while Basic Material index was down 1.0%. Zima Holding

Co. fell 16.9%, while Al-Nawadi Holding Co. was down 7.1%.

Oman: The MSM index declined 0.2% to close at 6,744.1. Losses were led by

the Financial and Industrial indices, falling 0.5% and 0.4% respectively. Al

Sharqia Inv. Holding declined 3.4%, while Galfar Eng. & Con. was down 3.1%.

Bahrain: The BHB index gained 0.5% to close at 1,459.5. The Comm. Bank

index rose 1.2%, while other indices remained flat or ended in red. Al Ahli

United Bank gained 2.4%, while Bahrain Islamic Bank was up 0.6%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

QNB Group 192.00 5.5 356.5 11.6

Ooredoo 148.50 4.2 818.9 8.2

Masraf Al Rayan 52.10 3.8 3,138.7 66.5

Qatar Islamic Bank 95.00 3.7 558.5 37.7

National Leasing 32.15 3.0 1,132.7 6.6

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Vodafone Qatar 18.35 2.9 6,481.5 71.3

Masraf Al Rayan 52.10 3.8 3,138.7 66.5

United Development Co. 26.15 1.2 2,709.7 21.5

Ezdan Holding Group 27.25 (0.9) 1,578.1 60.3

Barwa Real Estate Co. 39.20 1.8 1,500.7 31.5

Market Indicators 22 May 14 21 May 14 %Chg.

Value Traded (QR mn) 1,158.6 776.7 49.2

Exch. Market Cap. (QR mn) 724,621.1 709,180.8 2.2

Volume (mn) 24.1 16.3 47.9

Number of Transactions 9,827 9,344 5.2

Companies Traded 43 43 0.0

Market Breadth 33:9 20:19 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,397.98 2.6 (0.7) 30.8 N/A

All Share Index 3,301.47 2.3 (0.9) 27.6 15.8

Banks 3,193.65 3.5 0.4 30.7 15.9

Industrials 4,379.90 1.4 (2.7) 25.1 17.1

Transportation 2,278.25 0.9 (4.4) 22.6 14.6

Real Estate 2,676.49 1.7 0.8 37.0 13.4

Insurance 3,259.26 0.7 (1.3) 39.5 8.6

Telecoms 1,749.20 3.9 1.2 20.3 24.4

Consumer 6,930.06 (0.5) (2.3) 16.5 27.1

Al Rayan Islamic Index 4,316.48 2.1 (0.4) 42.2 18.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

National Medical Care Saudi Arabia 77.00 8.8 8,235.1 42.1

Comm. Bank Of Dubai Dubai 6.00 8.1 138.9 39.2

First Gulf Bank Abu Dhabi 17.25 6.5 5,162.2 19.3

QNB Group Qatar 192.00 5.5 356.5 11.6

Bank Of Sharjah Abu Dhabi 2.00 5.3 1,000.0 11.7

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Tihama Saudi Arabia 361.50 (10.0) 505.8 229.4

Gulf Pharma. Ind. Abu Dhabi 3.09 (6.4) 8,698.2 3.9

Abu Dhabi Nat. Hotels Abu Dhabi 3.01 (5.9) 18.2 (2.9)

RAKBANK Abu Dhabi 8.00 (5.9) 50.0 12.0

United Real Estate Co. Kuwait 0.11 (3.6) 136.6 (8.5)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Dist. Co 41.35 (2.7) 5.1 3.1

Mannai Corp. 118.00 (1.6) 6.2 31.3

Aamal Co. 17.23 (1.5) 168.2 14.9

Qatar Fuel Co. 223.90 (1.4) 430.7 2.5

Zad Holding Co. 75.60 (1.2) 7.8 8.8

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 52.10 3.8 161,562.5 66.5

Ooredoo 148.50 4.2 119,624.0 8.2

Vodafone Qatar 18.35 2.9 117,766.6 71.3

Qatar Fuel Co. 223.90 (1.4) 96,239.4 2.5

United Development Co. 26.15 1.2 70,620.0 21.5

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,008.16 2.6 (0.7) 2.6 25.3 318.23 199,053.4 16.2 2.2 3.8

Dubai 4,864.03 0.3 (6.1) (3.9) 44.3 559.11 91,389.5 19.5 1.9 2.1

Abu Dhabi 4,925.71 2.0 (1.9) (2.4) 14.8 177.74 135,082.4 14.5 1.8 3.5

Saudi Arabia 9,750.90 (0.2) (0.6) 1.7 14.2 3,526.59 527,779.4 19.5 2.4 2.9

Kuwait 7,346.83 (0.4) (0.8) (0.8) (2.7) 75.88 113,856.3 15.3 1.2 3.7

Oman 6,744.14 (0.2) 0.1 0.3 (1.3) 15.97 24,534.4 12.4 1.7 3.9

Bahrain 1,459.45 0.5 (0.3) 2.3 16.9 6.64 53,911.8 10.6 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,600

12,700

12,800

12,900

13,000

13,100

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QE index rose 2.6% to close at 13,008.2. The Telecoms and

Banking & Financial Services indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

QNB Group and Ooredoo were the top gainers, rising 5.5% and

4.2% respectively. Among the top losers, Qatar Cinema & Film

Dist. Co. fell 2.7%, while Mannai Corp. declined 1.6%.

Volume of shares traded on Thursday rose by 47.9% to 24.1mn

from 16.3mn on Wednesday. However, as compared to the 30-

day moving average of 28.7mn, volume for the day was 16.1%

lower. Vodafone Qatar and Masraf Al Rayan were the most

active stocks, contributing 26.9% and 13.1% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Emirates

Telecommunications

Corporation (Etisalat)

Fitch UAE LT FCIDR A+ A+ – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, , FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating,

LC – Local Currency, FCIDR - Foreign Currency Issuer Default Rating)

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

United Real Estate Co.

(URC)

Kuwait KD – – 4.5 – 0.6 NA

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/22 US Department of Labor Initial Jobless Claims 17 May 326K 310K 298K

05/22 US Department of Labor Continuing Claims 10 May 2653K 2675K 2666K

05/22 US Bloomberg Bloomberg Economic Expectations May 42.5 – 48

05/22 US Bloomberg Bloomberg Consumer Comfort 18 May 34.1 – 34.9

05/22 US Markit Markit US Manufacturing PMI May 56.2 55.5 55.4

05/22 US Conference Board Leading Index April 0.40% 0.40% 1.00%

05/22 US Kansas City Fed Kansas City Fed Manf. Activity May 10.0 7.0 7.0

05/22 EU Markit Markit Eurozone Manufacturing PMI May 52.5 53.2 53.4

05/22 EU Markit Markit Eurozone Services PMI May 53.5 53.0 53.1

05/22 EU Markit Markit Eurozone Composite PMI May 53.9 53.9 54.0

05/22 France INSEE Manufacturing Confidence May 99.0 100.0 100.0

05/22 France INSEE Business Confidence May 94.0 94.0 94.0

05/22 France Markit Markit France Composite PMI May 49.3 50.5 50.6

05/22 France Markit Markit France Manufacturing PMI May 49.3 51.0 51.2

05/22 France Markit Markit France Services PMI May 49.2 50.4 50.4

05/22 Germany Markit Markit/BME Germany Composite PMI May 56.1 56.0 56.1

05/22 Germany Markit Markit/BME Germany Manu. PMI May 52.9 54.0 54.1

05/22 Germany Markit Markit Germany Services PMI May 56.4 54.5 54.7

05/23 Germany Destatis GDP SA QoQ 1Q2014 0.80% 0.80% 0.80%

05/23 Germany Destatis GDP WDA YoY 1Q2014 2.30% 2.30% 2.30%

05/23 Germany Destatis GDP NSA YoY 1Q2014 2.50% 2.50% 2.50%

05/23 Germany Destatis Private Consumption QoQ 1Q2014 0.70% 0.60% -0.30%

05/23 Germany Destatis Government Spending QoQ 1Q2014 0.40% 0.30% -0.30%

05/23 Germany Destatis Capital Investment QoQ 1Q2014 3.20% 2.10% 0.70%

05/23 Germany Destatis Construction Investment QoQ 1Q2014 3.60% 3.20% 0.20%

05/23 Germany Destatis Domestic Demand QoQ 1Q2014 1.90% 1.40% -0.30%

05/23 Germany Destatis Exports QoQ 1Q2014 0.20% 0.60% 2.50%

05/23 Germany Destatis Imports QoQ 1Q2014 2.20% 1.00% 1.30%

05/22 UK ONS Public Finances (PSNCR) April -10.6B – 15.7B

05/22 UK ONS Central Government NCR April 1.9B – 22.7B

Overall Activity Buy %* Sell %* Net (QR)

Qatari 43.29% 57.14% (160,443,091.51)

Non-Qatari 56.70% 42.86% 160,443,091.51

3. Page 3 of 7

05/22 UK ONS Public Sector Net Borrowing April 9.6B 3.4B 6.1B

05/22 UK ONS GDP QoQ 1Q2014 0.80% 0.80% 0.80%

05/22 UK ONS GDP YoY 1Q2014 3.10% 3.10% 3.10%

05/22 UK ONS Private Consumption QoQ 1Q2014 0.80% 0.60% 0.40%

05/22 UK ONS Government Spending QoQ 1Q2014 0.10% 0.20% 0.00%

05/22 UK ONS Gross Fixed Capital Formation QoQ 1Q2014 0.60% 1.20% 1.90%

05/22 UK ONS Exports QoQ 1Q2014 -1.00% 0.00% 2.80%

05/22 UK ONS Imports QoQ 1Q2014 -1.10% 0.20% -0.40%

05/22 UK ONS Total Business Investment QoQ 1Q2014 2.70% 2.20% 2.40%

05/22 UK ONS Total Business Investment YoY 1Q2014 8.70% – 8.70%

05/22 UK CBI CBI Trends Selling Prices May 4.0 10.0 9.0

05/22 China Markit HSBC China Manufacturing PMI May 49.7 48.3 48.1

05/22 Japan Markit Markit/JMMA Japan Manufacturing PMI May 49.9 – 49.4

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QE to introduce margin trading, short selling – The Qatar

Exchange (QE) is planning to introduce margin trading and

covered short selling in the near future. The QE is currently

interacting with the regulator to evolve rules and regulations to

govern these transactions. The QE's CEO Rashid Al Mansoori

said that the idea is to increase investment opportunities in the

market, diversify the market and help enhance liquidity.

(Peninsula Qatar)

ORDS signs $1bn loan deal to repay existing debt –

Ooredoo (ORDS) has signed a $1bn five-year revolving credit

facility. ORDS will use the new facility to repay a $750mn loan

due in May 2015 and allocate the rest for general business

purposes. Seventeen banks helped to fund the loan, including

QNB Group, Barclays and HSBC. QNB Group is the facility

agent for the lenders and acted as a documentation agent for

the facility and was the general financial advisor to ORDS. (QE,

Gulf-Times.com)

Indosat may buy back $650mn bonds in 2015 – Ooredoo’s

Indonesian unit, Indosat may buy back $650mn in bonds due in

2020 sometime in 2015. Indosat’s CFO, Stefan Carlsson, said

that the company aims to reduce its exposure to the US dollar to

25% from nearly 50% now. Indosat is also targeting single-digit

growth in revenue and capital expenditures of 8-9 trillion rupiah

in 2014. (Reuters)

Qatargas reaffirms its commitment to Europe LNG supplies

– Qatargas' Chief Operating Officer–Commercial & Shipping,

Alaa Abujbara presented his views on the European energy

market, the current and future role of LNG, the influence of new

energy policies and the company's marketing activities across

the continent at a recent conference in Amsterdam. Abujbara

made a clear case for LNG as a major part of the energy mix by

highlighting its advantages over alternative fuel sources like

renewables, nuclear, coal, pipeline gas and liquid fuels. He also

reaffirmed Qatargas' commitment to continue supplying LNG to

Europe. (Gulf-Times.com)

Gasal finishes oxygen, nitrogen pipeline network – Gasal

has completed a major expansion of its oxygen and nitrogen

pipeline network to support the Ras Laffan Industrial City’s

growing requirements for industrial gases. The company is now

preparing to bring additional production capacity on a new land

currently under development. (Gulf-Times.com)

QNB Group to launch campaign to reward customers for

bank transfers – QNB Group (QNBK) will be launching its latest

campaign to reward those customers who use its internet

banking services for their bank transfers. The campaign will run

throughout the summer months and conclude on July 31. The

QNB campaign will be open to all customers who use internet

banking for International Fund Transfers during the campaign’s

running time. This will include all QNB customers who are

making international transfers via SWIFT, Partner Bank

transfers (HDFC India and HBTF Jordan) and Unit to Unit

transfers between different QNB units in other countries made

via QNB’s internet banking. Further, QNB states that in order to

be placed in the raffle draw, customers will have to transfer a

minimum of 1,000 QR in order to be eligible to win a monthly

basic salary as a bonus, a maximum of QR30,000. Each

transfer worth more than QR1,000 will get a chance to enter the

draw. (QNB Group Press Release)

Qatar Cool signs contract for 3rd cooling plant in West Bay

– Qatar District Cooling Company (Qatar Cool) has signed a

contract for constructing its third plant in West Bay. Once

completed in 2016, the plant, which is the fourth one in Qatar,

will provide cooling to residential and commercial towers. The

plant is designed to produce 40,000 tons-cooling, cutting down

energy usage by 40-45% as compared to traditional cooling

systems. Qatar Cool’s Chairman Badr al-Meer underscored the

importance of the company’s expansion to Qatar’s long-term

commitment to sustainable development, since district cooling is

seen as an environment-friendly solution to address the nation’s

cooling requirements. (Gulf-Times.com)

QA’s expansion continues with new route to Turkey – Qatar

Airways (QA) has continued its expansion plans with the launch

of direct flights to its third destination in Turkey. The airline’s

inaugural flight to Istanbul Sabiha Gokcen International Airport

marked its 140th destination from Doha. The four-times-weekly

service to Istanbul Sabiha Gokcen extends the airline’s reach in

Turkey’s largest city. This will be QA’s third route to Turkey, in

addition to dedicated flights to Istanbul Ataturk Airport and

Ankara, which takes the number of flights to Turkey from 14 to

18 frequencies each week. (Gulf-Times.com)

MoI, Airbus unit agree on LTE network partnership – Qatar’s

Ministry of Interior (MoI) and Airbus Defence & Space have

agreed on a partnership to develop a Terrestrial Trunked Radio

(Tetra) Group Communication over Long-Term Evolution (LTE)

service using the MoI’s existing LTE and professional mobile

radio communication networks. The new service will be made

progressively available to the country’s public safety agencies

such as police, fire-fighters, ambulances, emergency services,

etc. The most important benefit will be the seamless

interoperability of users across existing networks of the MoI,

Tetra and LTE, as well as the reuse of all MoI’s assets –

networks, control room dispatching and resource location

applications. (Gulf-Times.com)

4. Page 4 of 7

International

QNB Group: Eurozone’s two-speed recovery is slowly

underway – The Eurozone’s recovery is slowly underway. Data

for the first quarter of 2014 published last week confirmed that

real GDP growth is on an upward trend in Germany and Spain

while France and Italy continue to lag behind. This two-speed

growth performance is mainly driven by the extent to which each

Eurozone country has managed to gain competitiveness in the

last few years by reducing its unit labor costs relative to

Germany. Unless this internal adjustment process continues, the

growth performance in the single currency area will diverge

further, with important implications for the stability of the

Eurozone. What explains this two-speed expansion in the

Eurozone? The answer is competitiveness measured by unit

labor costs – the cost of labor for one unit of production. What

drives growth is the ability of businesses to compete in the

global economy, which largely depends on their labor costs,

particularly in advanced economies. As unit labor costs rise

without a corresponding rise in labor productivity, businesses

lose competitiveness. A sufficiently large loss of competitiveness

can force businesses to reduce their activities or even shut

down. At an economy-wide level, a loss of competitiveness

means lower growth and higher unemployment as both external

and domestic demand for the country’s goods and services

weaken. This is even more evident in countries with a common

currency like the Eurozone where the option to regain

competitiveness by weakening the currency is unavailable.

Overall, the Eurozone recovery remains fragile and predicated

on continued adjustment in unit labor costs. What is worrisome

is the continued divergence in growth performance between

Germany and Spain on the one hand and France and Italy on

the other, reflecting the necessary adjustment in unit labor costs

still needed in the latter two economies. Without such

adjustment, the economic recovery could unravel, calling into

question the stability of Eurozone once again (QNB Group)

Markit PMI: US factory data upbeat, Eurozone business

stays strong – Manufacturing growth in the US picked up to a

three-month high in May 2014, while private business activity in

the Eurozone grew at just under its fastest pace in three years.

In Asia, factory activity in Japan cooled slightly in May 2014, but

at a slower pace than in April 2014. Financial data firm Markit

said its preliminary or flash US Manufacturing Purchasing

Managers Index (PMI) rose to 56.2 in May 2014 from 55.4 in

April 2014, while factory output growth hit its fastest pace since

February 2011, rising to 59.6 from 58.2. In Europe, an

unexpected pickup in the service industry was offset by

lackluster factory activity, but was enough to show some traction

in the Eurozone's fragile recovery. Markit's Composite PMI for

the single currency bloc, edged down to 53.9 from a near three-

year high of 54.0 in April 2014, matching the consensus forecast

in a Reuters poll. Meanwhile, the Markit-JMMA flash Japan

Manufacturing PMI rose to a seasonally adjusted 49.9 in May

2014 from April's 49.4. (Reuters)

US new home sales rise in April, but momentum lacking – A

Commerce Department report showed that the sales of new US

single-family homes rose by 6.4% to a seasonally adjusted

annual rate of 433,000 units in April, however economists said

that the market was still not gaining steam. The rise ended two

straight months of declines and beat market expectations, but

sales remained in line with their sluggish first-quarter average. A

run-up in mortgage rates and home prices over the last year has

weighed on the market. Sales have also been hampered by a

shortage of properties and the brutally cold winter. The slump

has caught the attention of the Federal Reserve, which is

scaling back the amount of money it is pumping into the

economy through monthly bond purchases. (Bloomberg)

IFO: German business confidence index down to 110.4 in

May – The IFO Institute’s Business Climate Index for Germany

fell to 110.4 in May from 111.2 in the previous month. According

to the median of 38 estimates in a Bloomberg survey,

economists had predicted a drop to 110.9. The IFO report

showed that the index for current conditions fell to 114.8 from

115.3 in the earlier month. A gauge of expectations slid to 106.2,

the lowest reading since October. Germany is key to the

recovery in the 18-nation euro area, which is struggling to pick

up pace amid near-record unemployment and subdued pricing

power. The German economic growth was driven exclusively by

domestic demand in the first three months of the year, and the

Bundesbank has said the expansion will cool this quarter.

(Bloomberg)

Spain, Greece debt ratings improve – Spain’s credit ranking

was raised by Standard & Poor’s (S&P), while Fitch Ratings

increased Greece’s grade, as the economic outlook improve for

these countries that were at the heart of Europe’s sovereign

debt crisis. S&P lifted Spain’s long-term rating one level to BBB,

the second-lowest investment grade. Fitch boosted Greece’s

long-term rank one step to B, which is five steps below

investment grade. Markets have already given their verdict on

the turnaround in nations that threatened to break apart the euro

bloc in the early 2010s. Spain’s borrowing costs have fallen to

record lows amid a rally that has also brought investors back to

Greece, Ireland and Portugal. Greece is poised to return to

growth after six years of contraction. (Bloomberg)

Russian minister confident about no EU sanctions on

exports – Russian Economy Minister Alexei Ulyukayev said he

was confident that the European Union would refrain from

imposing sanctions that could hit Russia’s major exports. Next

week, EU leaders are expected to discuss a series of steps they

could take against Russia if there are disruptions to Ukraine's

presidential election this week. The measures, including

restrictions ranging from luxury goods imports to an oil & gas

ban, envisage three scenarios – low-intensity, medium-intensity

and high-intensity sanctions. (Reuters)

Brazil current account deficit widens – According to data

released by Brazil’s central bank, the country posted a current

account deficit of $8.291bn in April, above the median forecast

for $6.7bn and the $6.2bn gap recorded in March 2014. This

was due to a jump in the repatriation of profits and dividends by

foreign companies. Foreign companies repatriated $3.291bn, up

sharply from the $2.542bn sent abroad in April of 2013.

Brazilians continue to spend heavily abroad as the local

currency, real, has strengthened in recent months. Spending

abroad was $1.797bn in April, up nearly 20% YoY. Despite the

larger deficit in April, the current account gap as percentage of

GDP remained stable at 3.65%. (Reuters)

Regional

Carillion named preferred bidder for £400mn Mideast deals

– British support services & construction firm Carillion has been

named as the preferred bidder for a number of contracts in the

Middle East worth more than £400mn. The company has been

selected with its joint venture business Al-Futtaim–Carillion for

contracts in the UAE to build two new luxury hotels worth around

£300mn. It has also been awarded a number of construction

projects worth more than £100mn in Dubai and Saudi Arabia in

sectors like healthcare, retail, leisure and residential real estate.

(GulfBase.com)

5. Page 5 of 7

Moody's forms global Islamic Finance Group – Moody's

Investors Service has formed a dedicated global Islamic Finance

Group (IFG) to meet the growing demand for Islamic finance

credit ratings and research. Moody's IFG will deliver

independent analysis for Shari’ah-compliant products, financial

institutions and Takaful insurers in order to support an improved

understanding of the credit risks and market trends in this

rapidly expanding sector. IFG will be chaired by Dubai-based

Khalid Howladar, recently-appointed Global Head of Islamic

Finance, and will draw expertise from Moody's sovereign,

banking, corporate, insurance and structured finance analytical

teams worldwide. (GulfBase.com)

Dar Al Arkan to price 5-year Sukuk – Saudi-based Dar Al

Arkan Real Estate Development Company is planning to price a

benchmark-sized, dollar-denominated Sukuk of five years

duration this week. The developer has chosen eight banks in

total to arrange it and the potential Sukuk that may follow.

(GulfBase.com)

DAAR completes third tranche of SR1.5bn Islamic Sukuk

Program – Dar Al Arkan Real Estate Development Company

(DAAR) has completed the third tranche of its international

Islamic Sukuk program, raising SR1.5bn. The issuance received

significant interest from international market participants with the

order book exceeding SR3.75bn (2.3 times the amount issued).

The Sukuk was issued at a profit rate of 6.5% per annum, which

matures on May 28, 2019. Alkhair Capital, Al Rayan Investment,

Al Hilal bank, Barwa Bank, Deutsche Bank, Emirates NBD,

Goldman Sachs and Qinvest acted as the joint book runners to

manage the issuance of the Sukuk. (Tadawul)

NasJet appoints new CEO – NasJet, a part of the National Air

Services Group (NAS Holding) has appointed Saad Alazwari as

its new CEO. The Saudi-based private jet company manages

and supports 66 fixed-wing aircraft with a fleet value of $2bn.

(Bloomberg)

S&P: Banks’ exposure to UAE realty market set to rise –

Standard & Poor’s (S&P) said that the exposure of banks to the

booming real estate sector in the UAE has remained at high

levels, which is likely to increase in coming years. Loans to the

real estate sector represented about 30% of the total loans and

122% of the total equity in 2013. That is still below the peak in

2008, when the sector’s total exposure was almost 150% of

banks’ equity. (GulfBase.com)

S&P affirms Sharjah’s credit rating on per capita growth –

Standard & Poor’s Ratings Services (S&P) has affirmed A/A-1

long and short-term foreign and local currency sovereign credit

ratings of the Emirate of Sharjah. The outlook is stable. The

affirmation primarily reflects the solid growth in Sharjah’s GDP

per capita. Sharjah is the third-largest member of the UAE in

terms of population, GDP and geographic area. The Emirate has

approximately 10% of the UAE’s total population and accounted

for about 5% of the UAE’s GDP for 2013. (GulfBase.com)

Apax sells stake in Travelex to UAE investors – London-

based Apax Partners has agreed to sell its majority stake in

Travelex Holdings Ltd. to a group of investors based in the UAE.

Bavaguthu Raghuram Shetty, an Indian-born entrepreneur and

entities linked to Saeed Bin Butti Al Qubaisi’s Abu Dhabi-based

Centurion Investments will buy Apax’s stake in the chain of retail

currency exchanges. (Bloomberg)

Emaar hires banks for mall unit share sale – According to

sources, Emaar Properties has hired HSBC Holdings and

Emirates NBD as bookrunners for the IPO of its retail arm, with

Rothschild as the financial adviser. The National Bank of Abu

Dhabi (NBAD) and EFG Hermes Holding Company will also be

the bookrunners on the sale of 25-30% stake in the malls unit on

the Dubai Financial Market (DFM). The company seeks to raise

about $2bn through the sale planned for September 2014.

(GulfBase.com)

DMC to build world’s first LNG-powered harbor tug –

Drydocks World and Dubai Maritime City (DMC) has signed a

MoU with Wartsila and Dubai Carbon Centre of Excellence for

building the world’s first LNG powered harbor tug. The project

named ‘Elemarateyah’ is part of the Dubai Maritime Green

Initiative. DMC will collaborate with Wartsila for design,

equipment and related support services for the tug’s

construction. (GulfBase.com)

Nakheel to build mall on Jebel Ali waterfront; floats tender

for Deira Islands project – Dubai-based developer Nakheel

has invited contractors to bid for the main contract to build a

community retail center within the Badrah area near the Jebel

Ali waterfront. The scope of work includes construction of 15

retail units and 10 food & beverage outlets as well as a ground

floor supermarket. The site will have a total area of 21,055

square meters with a built-up area of 6,889 square meters.

Meanwhile, Nakheel has floated a tender for its Deira Islands

tourism development. All four Deira Islands will feature hotels,

resorts and residential, commercial and retail units. The tender

calls for road works for two of the islands A and B, which are

approximately 860 hectares in total. Bids need to come in by

June 17, 2014. (Bloomberg) (GulfBase.com)

Jumeirah to enter Mauritius with luxury project – Dubai-

based Jumeirah Group has signed a management agreement to

operate a luxury resort in Mauritius. The hotel is currently under

development and expected to open in 2018. It will be set on 68.5

hectares of land and be located approximately 50 kilometers

from Sir Seewoosagur Ramgoolam International Airport. The

property will include all-day dining and specialty restaurants,

lounge and poolside bars, meeting and events space, spa

facilities, a swimming pool, health club, children’s facilities and a

teen club. (GulfBase.com)

DSC: Dubai’s inflation remains steady at 3% – According to

the data from the Dubai Statistics Centre (DSC), Dubai’s

inflation remains steady at 3% in April 2014. Housing and

services have been the main sources of inflationary pressure in

Dubai, with the housing component of the consumer price index

(CPI) rising around 5% YoY in April. Education costs rose at a

similar pace in April, but inflation in healthcare, transport,

communications and hospitality sectors were stable. CPI

remained unchanged at 3% on an annual basis for April, but the

index rose 0.1% as compared to March. Higher housing,

communications and education costs were offset by lower food

prices, miscellaneous goods and services and marginally lower

transport costs last month. (GulfBase.com)

Biggest ever vessel arrives at DP World’s SPCT – DP World

operated Saigon Premier Container Terminal (SPCT) in Vietnam

has received the biggest ever vessel, NYK-owned Northern

Genius. With a nominal TEU (twenty foot equivalent container

unit) capacity of 4,300 and DWT of 54,000, Northern Genius

sailed up the 54kms new Soai Rap River channel following its

opening in 2014. (GulfBase.com)

Etisalat scraps buyout offer to Maroc Telecom minority

shareholders – Emirates Telecommunications Corporation

(Etisalat) said that it has scrapped its offer to buy the remaining

shares in Maroc Telecom. Etisalat’s spokesman confirmed that

the company has now abandoned its provisional offer submitted

earlier this week to the Moroccan authorities for approval.

(Reuters)

6. Page 6 of 7

ADUPC approves 13 projects in Abu Dhabi – Abu Dhabi

Urban Planning Council (ADUPC) has approved 13

development projects covering over 4mn square meters in

1Q2014. Five of these approved projects were master plans,

with the remaining eight being detailed project plans. One of the

biggest project was for Aldar Properties’ Al Raha Beach East

Master Plan. (GulfBase.com)

ADCB partners with ADF for cash management solution –

Abu Dhabi Commercial Bank (ADCB) has partnered with Abu

Dhabi Finance (ADF) to provide premium cash management

solution. Under the agreement, ADF will capitalize on ADCB's

experience to enhance its cash management system and will

employ ADCB's ProCash service, a cash management platform.

This agreement will help to streamline ADF's wide range of

electronic banking services. (GulfBase.com)

Etisalat lists $7bn GMTN on ISE – Etisalat has completed the

listing of its $7bn global medium term note (GMTN) program on

the Irish Stock Exchange (ISE). The listed bond program is

being rated by three credit rating agencies with the following

ratings: Moody’s rating – Aa3, Standards & Poor’s rating – AA-

and Fitch’s rating – A+. (ADX)

NBF launches structured trade commodity finance – The

National Bank of Fujairah (NBF) has launched its structured

trade commodity financing (STCF) facility, a specialized solution

for the cross-border commodity trading requirements of various

companies across the UAE. With STCF, the bank will work with

clients to structure comprehensive, short-to-medium term

financing arrangements to support their commodity trading

activity. STCF transactions are structured around a company’s

supply chain, from the purchase to sale and export of

commodities and materials, and constitute a full suite of trade

financing and foreign exchange hedging tools. (Bloomberg)

Wataniya Telecom adopts ORDS brand – Kuwait-based

National Mobile Telecommunications Company (Wataniya) has

fully adopted the new global brand, Ooredoo (ORDS). ORDS in

Kuwait will introduce a revamped portfolio of its new services

which includes Kuwait’s first comprehensive e-commerce range

of services, whereby ORDS customers will be able to access

and buy online exclusive offers on the latest electronic products.

Currently, ORDS holds a 92.1% stake in Wataniya.

OMR7.5mn aquarium in Oman to be ready by 2016 –

Petroleum Development Oman (PDO) announced that an

aquarium worth OMR7.5mn at Seeb harbor is expected to be

completed in late 2015 or early 2016. The project will include an

educational center and will be spread over across 17,000

square meters. (GulfBase.com)

CKG Holding plans $150mn cocoa factory in Oman – Ivory

Coast-based CKG Holding is planning to open a cocoa factory in

Oman in 2015 amid growing chocolate demand in the Middle

East and India. The $150mn factory in Salalah will have capacity

to process 50,000 metric tons of cocoa beans a year with

opening planned for the end of 2015. It will be a joint venture of

Oman and CKG under the name of Chocolatry of Oman.

(Bloomberg)

Al Mazaya awards BHD2.2mn contract to KMC Bahrain – Al

Mazaya Holding Company has awarded a BHD2.2mn

construction contract to KMC Bahrain. The contract is for the

building of Mazaya Logistics' industrial warehousing facility

spread over 27,605 square meters in Bahrain Investment Wharf.

The project is to be delivered within six months. KMC Bahrain

was one of five contractors that bid for the tender. The contract

entails construction of 42 industrial units having areas ranging

between 250 and 500 square meters, totaling 15,250 square

meters. All concrete, iron, and electro-mechanical works are

also a part of the scope of work. The total value of the project is

BHD7.8mn. KMC is the contracting and project management

services subsidiary of Kuwait Finance House. (GulfBase.com)

Garmco appoints new CFO – Bahrain-based Gulf Aluminum

Rolling Mill Company (Garmco) has appointed Hilmar Leimbach

as the new Chief Financial Officer (CFO). Leimbach has

experience of 22 years across functions like finance, accounts

and audit. (GulfBase.com)

Roberto Cavalli in sale talks with Investcorp – Roberto

Cavalli is in negotiations to sell majority stake in its eponymous

Italian fashion brand to Bahrain-based private equity firm,

Investcorp. The transaction is expected to be valued at €450mn

including debt. This price would equate to more than 15 times

earnings before interest, taxes, depreciation and amortization.

(Bloomberg)

7. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

(0.2%)

2.6%

(0.4%)

0.5%

(0.2%)

2.0%

0.3%

(1.0%)

0.0%

1.0%

2.0%

3.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,292.56 (0.1) (0.1) 7.2 DJ Industrial 16,606.27 0.4 0.7 0.2

Silver/Ounce 19.46 (0.2) 0.5 (0.0) S&P 500 1,900.53 0.4 1.2 2.8

Crude Oil (Brent)/Barrel (FM

Future)

110.54 0.2 0.7 (0.2) NASDAQ 100 4,185.81 0.8 2.3 0.2

Natural Gas (Henry

Hub)/MMBtu

4.38 (1.8) (1.0) 0.9 STOXX 600 341.76 0.2 0.8 4.1

LPG Propane (Arab Gulf)/Ton 105.63 1.1 3.3 (16.3) DAX 9,768.01 0.5 1.4 2.3

LPG Butane (Arab Gulf)/Ton 118.00 0.2 2.9 (13.6) FTSE 100 6,815.75 (0.1) (0.6) 1.0

Euro 1.36 (0.2) (0.5) (0.8) CAC 40 4,493.15 0.3 0.8 4.6

Yen 101.97 0.2 0.5 (3.2) Nikkei 14,462.17 0.9 2.6 (11.2)

GBP 1.68 (0.2) 0.1 1.7 MSCI EM 1,042.92 0.2 1.1 4.0

CHF 1.12 (0.2) (0.4) (0.3) SHANGHAI SE Composite 2,034.57 0.7 0.4 (3.8)

AUD 0.92 0.1 (1.4) 3.5 HANG SENG 22,965.86 0.1 1.1 (1.5)

USD Index 80.39 0.2 0.4 0.4 BSE SENSEX 24,693.35 1.3 2.4 16.6

RUB 34.16 (0.5) (1.7) 3.9 Bovespa 52,626.41 (0.3) (2.5) 2.2

BRL 0.45 (0.4) (0.4) 6.3 RTS 1,326.58 1.0 5.1 (8.1)

186.9

152.8

139.6