1. Page 1 of 6

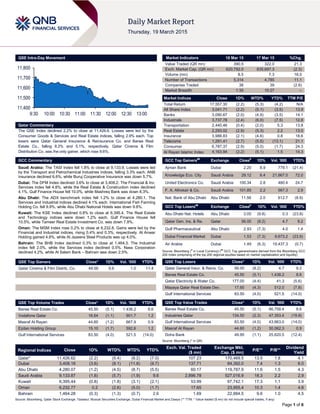

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 2.2% to close at 11,426.6. Losses were led by the

Consumer Goods & Services and Real Estate indices, falling 2.9% each. Top

losers were Qatar General Insurance & Reinsurance Co. and Barwa Real

Estate Co., falling 8.2% and 5.1%, respectively. Qatar Cinema & Film

Distribution Co. was the only gainer, which rose 9.6%.

GCC Commentary

Saudi Arabia: The TASI Index fell 1.8% to close at 9,133.9. Losses were led

by the Transport and Petrochemical Industries indices, falling 3.3% each. ANB

Insurance declined 6.6%, while Buruj Cooperative Insurance was down 5.7%.

Dubai: The DFM Index declined 3.6% to close at 3,408.2. The Financial & Inv.

Services index fell 4.8%, while the Real Estate & Construction index declined

4.1%. Gulf Finance House fell 10.0%, while Mashreq Bank was down 8.3%.

Abu Dhabi: The ADX benchmark index fell 1.2% to close at 4,280.1. The

Services and Industrial indices declined 4.1% each. International Fish Farming

Holding Co. fell 9.9%, while Abu Dhabi National Hotels was down 9.8%.

Kuwait: The KSE Index declined 0.8% to close at 6,395.4. The Real Estate

and Technology indices were down 1.2% each. Gulf Finance House fell

10.5%, while Tameer Real Estate Investment Co. was down 7.8%.

Oman: The MSM Index rose 0.2% to close at 6,232.8. Gains were led by the

Financial and Industrial indices, rising 0.4% and 0.3%, respectively. Al Anwar

Holding gained 4.8%, while Al Jazeera Steel Products was up 4.0%.

Bahrain: The BHB Index declined 0.3% to close at 1,464.3. The Industrial

index fell 2.0%, while the Services index declined 0.5%. Nass Corporation

declined 4.2%, while Al Salam Bank – Bahrain was down 2.5%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distrib. Co. 49.00 9.6 1.0 11.4

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 45.50 (5.1) 1,438.2 8.6

Vodafone Qatar 16.64 (1.1) 901.7 1.2

Masraf Al Rayan 44.60 (1.2) 667.9 0.9

Ezdan Holding Group 15.10 (1.7) 592.6 1.2

Gulf International Services 83.50 (4.0) 521.5 (14.0)

Market Indicators 18 Mar 15 17 Mar 15 %Chg.

Value Traded (QR mn) 390.5 322.0 21.3

Exch. Market Cap. (QR mn) 620,792.0 635,697.3 (2.3)

Volume (mn) 8.5 7.3 16.0

Number of Transactions 5,314 4,785 11.1

Companies Traded 38 39 (2.6)

Market Breadth 1:35 10:27 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 17,557.30 (2.2) (5.3) (4.2) N/A

All Share Index 3,041.71 (2.2) (5.1) (3.5) 13.9

Banks 3,090.67 (2.0) (4.9) (3.5) 14.1

Industrials 3,737.78 (2.4) (6.0) (7.5) 12.8

Transportation 2,440.46 (0.4) (2.0) 5.3 13.8

Real Estate 2,293.02 (2.9) (5.3) 2.2 13.0

Insurance 3,988.83 (2.1) (4.6) 0.8 18.6

Telecoms 1,291.41 (2.7) (5.5) (13.1) 21.1

Consumer 6,787.37 (2.9) (5.0) (1.7) 24.3

Al Rayan Islamic Index 4,163.94 (2.2) (5.1) 1.5 14.3

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ajman Bank Dubai 2.20 8.9 779.1 (21.4)

Knowledge Eco. City Saudi Arabia 29.12 6.4 21,667.0 72.0

United Electronics Co. Saudi Arabia 100.34 2.8 480.4 24.7

F. A. Alhokair & Co. Saudi Arabia 101.85 2.2 567.3 2.9

Nat. Bank of Abu Dhabi Abu Dhabi 11.59 2.0 612.7 (8.9)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Abu Dhabi Nat. Hotels Abu Dhabi 3.05 (9.8) 0.3 (23.8)

Qatar Gen. Ins. & Re. Qatar 56.00 (8.2) 4.7 9.2

Gulf Pharmaceutical Abu Dhabi 2.93 (7.3) 4.0 1.4

Dubai Financial Market Dubai 1.53 (7.3) 9,673.2 (23.9)

Air Arabia Dubai 1.49 (6.3) 19,437.3 (0.7)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar General Insur. & Reins. Co. 56.00 (8.2) 4.7 9.2

Barwa Real Estate Co. 45.50 (5.1) 1,438.2 8.6

Qatar Electricity & Water Co. 177.00 (4.4) 41.3 (5.6)

Mazaya Qatar Real Estate Dev. 17.65 (4.3) 512.0 (7.8)

Gulf International Services 83.50 (4.0) 521.5 (14.0)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Barwa Real Estate Co. 45.50 (5.1) 66,758.4 8.6

Industries Qatar 134.50 (2.3) 47,353.4 (19.9)

Gulf International Services 83.50 (4.0) 43,663.0 (14.0)

Masraf Al Rayan 44.60 (1.2) 30,062.3 0.9

Doha Bank 49.95 (1.1) 25,620.5 (12.4)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,426.62 (2.2) (5.4) (8.2) (7.0) 107.23 170,469.5 13.5 1.8 4.1

Dubai 3,408.18 (3.6) (8.1) (11.8) (9.7) 137.71 84,392.0 7.4 1.3 6.0

Abu Dhabi 4,280.07 (1.2) (4.5) (8.7) (5.5) 60.17 119,787.9 11.6 1.5 4.3

Saudi Arabia 9,133.87 (1.8) (5.7) (1.9) 9.6 2,896.78 527,016.9 18.3 2.2 2.9

Kuwait 6,395.44 (0.8) (1.8) (3.1) (2.1) 53.99 97,742.1 17.3 1.1 3.9

Oman 6,232.77 0.2 (2.6) (5.0) (1.7) 17.65 23,955.4 10.3 1.4 4.6

Bahrain 1,464.28 (0.3) (1.3) (0.7) 2.6 1.69 22,884.5 9.6 1.0 4.5

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,400

11,500

11,600

11,700

11,800

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index declined 2.2% to close at 11,426.6. The

Consumer Goods & Ser. and Real Estate indices led the losses.

The index fell on the back of selling pressure from non-Qatari

shareholders despite buying support from Qatari shareholders.

Qatar General Insurance & Reinsurance Co. and Barwa Real

Estate Co. were the top losers, falling 8.2% and 5.1%,

respectively. Qatar Cinema & Film Distribution Co. was the only

gainer, which rose 9.6%.

Volume of shares traded on Wednesday rose by 16.0% to 8.5mn

from 7.3mn on Tuesday. However, as compared to the 30-day

moving average of 14.0mn, volume for the day was 39.1% lower.

Barwa Real Estate Co. and Vodafone Qatar were the most

active stocks, contributing 16.9% and 10.6% to the total volume

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Doha Bank

(DHBK)

Capital

Intelligence

Qatar

FSR/LT FCR/ST

FCR/SR

A/A/A2/2 A/A/A2/2 – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

03/18 US MBA MBA Mortgage Applications 13-Mar -3.90% – -1.30%

03/18 EU Eurostat Trade Balance NSA January 7.9B 15.0B 24.3B

03/18 EU Eurostat Construction Output MoM January 1.90% – 0.20%

03/18 EU Eurostat Construction Output YoY January 3.00% – -2.70%

03/18 UK ONS Claimant Count Rate February 2.40% 2.40% 2.50%

03/18 UK ONS Jobless Claims Change February -31.0K -30.0K -39.4K

03/18 UK ONS Average Weekly Earnings 3M/YoY January 1.80% 2.20% 2.10%

03/18 UK ONS Weekly Earnings ex Bonus 3M/YoY January 1.60% 1.80% 1.70%

03/18 UK ONS ILO Unemployment Rate 3Mths January 5.70% 5.60% 5.70%

03/18 UK ONS Employment Change 3M/3M January 143K 130K 103K

03/18 Italy ISTAT Trade Balance Total January 219M – 5,741M

03/18 Italy ISTAT Trade Balance EU January 452M – 491M

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Fitch upgrades QNBK credit ratings – QNB Group (QNBK)

has consolidated both its position as the leading Financial

Institution in the MENA Region and its region leading credit

rating performance following the news by Fitch Ratings that the

Group’s Long Term Rating has been upgraded to AA- from the

previous A+ with an immediate effect. The move by

internationally renowned Fitch Ratings follows their recent report

on the positive outlook of The State of Qatar and in particular,

the “healthy condition” of the banking Sector. They concluded

that local banks were highly capitalised and that asset quality

was solid. Commitment from the Government to the sector was

a key underlying factor in the reflected cumulative upgrade of

Bank Ratings supported by sovereign wealth funds and the on-

going strong revenues from hydrocarbon production. (QNB

Group Press Release)

CBQK gets nod for QR3.6bn capital raise – The Commercial

Bank of Qatar (CBQK) has received its shareholders’ approval

to raise capital by QR3.6bn. This will be a combination of

additional Tier 1 and Tier 2 capital. CBQK’s shareholders at the

extraordinary general meeting (EGM) also approved increasing

the bank’s capital by 10% to QR3.26bn from QR2.96bn by

issuing bonus shares on the basis of one new share for every 10

existing shares. At the ordinary general assembly held prior to

the EGM, the shareholders had approved the issuance of local

and global certificates of deposits amounting up to $2bn.

Further, the shareholders approved the board of directors’

recommendation to distribute a cash dividend of 35% of the

nominal share value, which translates into QR3.5 per share. The

shareholders also gave the nod for two amendments in the

Articles of Association that will allow non-Qatari investors to own

up to 49% of the company’s share capital, as well as changing

the company name from “The Commercial Bank of Qatar

(Q.S.C.)” to “Commercial Bank (Q.S.C.)”. (Gulf-Times.com,

Peninsula Qatar)

QNNS shareholders approve dividend, higher foreign

ownership – Milaha’s (QNNS) shareholders in the ordinary

general assembly meeting approved the board’s

recommendation to increase the company’s foreign ownership

limit up to 49% and to distribute a cash dividend equivalent to

55% of the nominal share value. Dividend distribution will

commence starting March 24, 2015, through QNB Group

Overall Activity Buy %* Sell %* Net (QR)

Qatari 76.57% 58.86% 69,136,840.47

Non-Qatari 23.44% 41.14% (69,136,840.47)

3. Page 3 of 6

branches. The AGM also elected the new board for 2015-17.

Milaha’s Chairman, Sheikh Ali Jassim bin Mohamad al-Thani

said that the company will adopt a wait-and-see approach on

acquisitions in the light of the volatility in the energy markets.

However, he said the company remains focused on exploring

opportunities for organic and inorganic growth to enable it to

become a global player. (Gulf-Times.com, Peninsula Qatar)

CI affirms DHBK’s ratings on ‘Stable’ Outlook – The

international credit rating agency Capital Intelligence (CI) has

affirmed Doha Bank’s (DHBK) Financial Strength Rating (FSR)

at ‘A’, on ‘Stable’ Outlook, reflecting the Bank’s specialist

franchise in Qatar and the business potential of its new

operation in India, as well as its sound profitability. Improved

loan asset quality metrics and the prospect of an upcoming AT1

issue also support the FSR. The FSR is constrained by tight

liquidity and increased dependence on interbank funds, low

internal capital generation and the risk associated with execution

of the bank’s new strategy. Based on the strength of the Qatari

government balance sheet and the Qatar Investment Authority’s

(QIA) significant shareholding in the bank, the Support Rating is

affirmed at ‘2’. The Bank’s Long and Short-Term Foreign

Currency Ratings (FCR) are affirmed at ‘A’ and ‘A2’,

respectively, reflecting the Bank’s intrinsic financial condition,

and ongoing government support for all Qatari banks. The

Outlook on the FCRs reverts to ‘Stable’, to reflect the pressure

on the FSR, as well as the downside risks to operating

conditions due to the decline in Qatar’s oil revenues and the rise

in interest rates. (CI)

QSE urges private firms to reap advantages of market

listing – The Qatar Stock Exchange’s (QSE) CEO Rashid Bin

Ali Al Mansoori has urged private and family-owned companies,

which constitute more than 80% of the country’s fast growing

non-hydrocarbon sector, to go for initial public offerings (IPOs)

and get listed to reap various advantages. He said there are

many advantages that benefit those companies’ future, which

include continuity, organizational efficiencies, diversification of

funding options and an optimal financial status. He said that

IPOs in the Middle East have kept a low profile in recent years

and volume has been reduced significantly in most GCC

markets. (Gulf-Times.com, QSE)

QCSD deposits QNCD, AHCS bonus shares – The Qatar

Central Securities Depository (QCSD) has announced the

addition of bonus shares to the accounts of shareholders of

Qatar National Cement Company (QNCD) and Aamal Company

(AHCS). With this addition, the new capital of QNCD and AHCS

stands at QR540.11mn and QR6.3bn that is distributed across

54.0mn and 630mn shares, respectively. The companies’

shareholders may trade these shares from March 19, 2015.

(QSE)

Tourism injects $7.6bn into Qatari economy in 2014 – The

tourism sector injected $7.6bn into Qatari GDP in 2014,

representing 8.3% share in the country’s non-hydrocarbon

economy in 2014. According to IFP Info, Qatar received 2.8mn

visitors in 2014, up 8.2% over 2013, generating 61,000 jobs in

the tourism sector. As per the figures released by the Qatar

Tourism Authority (QTA), about 40% of tourists came from other

GCC countries, 15% from Europe and 28% from Asia and

Oceania. Hotel occupancy rates increased to an average of 73%

in 2014, with five-star properties holding the lion’s share, and

hoteliers are expecting those numbers to rise further in 2015.

Qatar’s healthy growth in the hotel and tourism sector was

underlined by the award of more than $2.5bn in contracts in

2014. (Gulf-Times.com)

Qatar to showcase $8.8bn tourism projects at ATM – Qatar

will be showcasing projects worth $8.8bn at the Arabian Travel

Market (ATM) 2015 roadshow. The ATM 2015 roadshow, which

arrived in Qatar on March 18, 2015 will be meeting with key

industry players and will highlight the country’s healthy growth in

the hotel and tourism sector. Qatar will be represented at the

event by the Qatar Tourism Authority, Qatar Airways, Al Rayyan

Hospitality, and Katara Hospitality at the dedicated Qatar stand.

Projects including Doha Festival City, Doha Convention Centre,

Rayyan Mall, Doha Zoo, Lusail Museum, Katara Towers, and

the FIFA World Cup football stadiums will be exhibited at the

event. (Bloomberg)

International

Fed opens door wider for rate hike but downgrades

economic outlook – The US Federal Reserve moved a step

closer to hiking rates for the first time since 2006, but

downgraded its economic growth and inflation projections,

signaling it is in no rush to push borrowing costs to more normal

levels. The US central bank removed a reference to being

"patient" on rates from its policy statement, opening the door

wider for a hike in the next couple of months while sounding a

cautious note on the health of the economic recovery. Fed

officials also slashed their median estimate for the federal funds

rate – the key overnight lending rate – to 0.625% for the end of

2015 from the 1.125% estimate in December. The cut to the so-

called "dot plot," together with other economic concerns cited by

the Fed, sent a more dovish message than investors were

expecting, and pushed market bets on the central bank's rate

"lift-off" from mid-year to the fall. (Reuters)

MBA: US mortgage applications fall in latest week – An

industry group said applications for home mortgages in the US

fell last week as both purchase and refinancing applications

decreased. The Mortgage Bankers Association (MBA) said its

seasonally adjusted index of mortgage application activity, fell

3.9% in the week ended March 13, 2015. The MBA's seasonally

adjusted index of refinancing applications fell 5.2%, while the

gauge of loan requests for home purchases, a leading indicator

of home sales, fell 1.5%. The refinance share of the total

mortgage activity fell to 59% of applications, the lowest level

since October 2014, from 60% the week before. (Reuters)

Britain raises growth forecasts for FY2015 and FY2016;

earnings growth slows in January – Britain raised its official

growth forecasts slightly as Finance Minister George Osborne

announced the annual budget. Osborne said growth for FY2015

was forecast at 2.5%, up from 2.4% made earlier in December.

Growth in FY2016 is now expected to reach 2.3% compared

with 2.2% in the December forecasts made by Britain's Office for

Budget Responsibility (OBR). Osborne said OBR believed

growth would hold at 2.3% in FY2017 and FY2018 before rising

to 2.4% in FY2019. The Bank of England has predicted Britain's

economy will grow 2.9% in FY2015 and in FY2016, helped by

the plunge in oil prices that is expected to boost consumption.

Osborne said the OBR also forecast the unemployment rate to

fall to 5.3% in FY2015, down from 5.7% in the three months to

January. Meanwhile, official data showed the pace of growth in

British workers' pay slowed in January, hit by fewer bonus

payments, while the percentage of employed people rose to an

all-time high. The Office for National Statistics said Britain's

unemployment rate was stable at 5.7%, matching its lowest level

in almost seven years. Inflation stood at 0.3% in January pushed

down by plunging oil prices. (Reuters)

OECD urges more reforms despite improving growth

prospects – The Organisation for Economic Cooperation &

Development (OECD) said governments cannot rely solely on

4. Page 4 of 6

low inflation and easy monetary policy to consolidate recovery

and boost employment, even though growth prospects are

improving in the world's largest economies. OECD said growth

remained too low to repair and activate labor markets, noting

that abnormally low inflation and interest rates create a growing

risk of financial instability with risk-taking and leverage driven by

liquidity rather than fundamentals. Central banks would continue

to drive recovery, but the OECD warned against an exclusive

reliance on monetary policy. In its overview of the world

economy, OECD confirmed its forecast of 3.1% GDP growth for

the US economy in 2015 and 3.0% in 2016. OECD raised its

Eurozone growth forecast to 1.4% in 2015 and 2.0% in 2016,

thanks to an acceleration of activity in the zone's largest

economy, Germany. Japan's growth is forecast at 1.0% in 2015

and 1.4% in 2016, up 0.2 points and 0.4% respectively. For

India, the OECD boosted its forecast significantly to 7.7%

growth in 2015, 1.3 percentage points higher than its previous

estimate, while it trimmed its forecast for China by 0.1 points to

7.0% in 2015. (Reuters)

China says to make flexible use of monetary policy tools –

The Chinese cabinet said the country will pursue an active fiscal

policy and make flexible use of its monetary policy tools to keep

its economy growing at a reasonable speed. In its latest attempt

to relieve concerns about China's cooling economy, the State

Council said it would increase targeted adjustments to its

policies to support the labor market. China's policymakers have

characterized their recent moves, which include two interest rate

cuts and one reduction in the reserve requirement ratio over four

months, as "targeted" adjustments that do not represent a shift

to looser policy. The central bank argues that the rate cuts keep

real interest rates stable and do not mark a switch to an easing

stance, even though that view is disputed by economists. To

stabilize China's economy, the cabinet said the state would

provide more public goods and services, pay closer attention to

water conservation projects, the refurbishment of shanty towns

and the construction of railways in central and west China.

Similarly, superfluous paperwork for ports and trade would also

be abolished to make it easier for companies to do business.

(Reuters)

Regional

Zamil AC wins SR348mn contract for Dar Al-Hijrah project –

Zamil Central Air Conditioners Company (Zamil AC) – a wholly-

owned subsidiary of Zamil Industrial Investment Company – has

been awarded a new contract valued at SR348mn by Al Fouzan

Trading & General Construction Company. The contract is to

supply custom chiller systems for the Saudi Real Estate

Development Company’s Dar Al-Hijrah project, owned by the

Public Investment Fund in Madinah located in the western

region of Saudi Arabia. The agreement is to supply chillers and

provide maintenance and support services for 15 years. The

company will start supplying heating, ventilating and air

conditioning (HVAC) units by 4Q2015 and will conclude the

supply in 2Q2016. (Tadawul)

SCC increases capital to SR11.8bn through shareholders

loans – Sadara Basic Services Company, an indirectly-owned

subsidiary of Sadara Chemical Company (SCC) announced that

SCC amended its Articles of Association (AoA) to reflect an

increase in capital. With this, SCC increased its capital by 21.3%

from SR9.7bn (969.96mn shares) to SR11.8bn (1.176bn

shares). The capital was increased through raising loans from

shareholders to offset the losses resulting from the increase in

operating activities. Shareholders retained their original

ownership in SCC following the increase, with Performance

Chemicals Holding owning 65% and Dow Saudi Arabia holding

35% of all shares. (Tadawul)

KSA healthcare sector to expand 9% in five years –

According to a research report titled, ‘Saudi Arabian Healthcare

Outlook 2020’, the healthcare sector in Saudi Arabia is

anticipated to expand at a CAGR of around 9% during the 2015-

2020. KSA has proven its leadership in the regional healthcare

sector, fuelled by increased government spending in healthcare,

steady rise in population, increase in per capita income and

growing healthcare projects. As per the study, liberalized

investment rules and compulsory healthcare insurance policies

would help the Saudi Arabian healthcare market to grow in the

coming years. Furthermore, thriving healthcare services during

Hajj sessions is another major factor that is driving this industry

in Kingdom. (GulfBase.com)

APC OGM approves 7.5% cash dividend for 4Q2014 –

Advanced Petrochemical Company (APC) announced that its

ordinary general meeting (OGM) has approved all the items on

agenda including payment of cash dividend for 4Q2014 at 7.5%

of capital, or SR0.75 per share, totaling SR123mn. Shareholders

of record on March 17, 2015 are entitled to this dividend which

will be paid on April 1, 2015. Accordingly, the dividends paid for

FY2014 reach SR3 per share, totaling SR492mn. (Tadawul)

SCC OGM approves SR6 dividend per share – Saudi Cement

Company (SCC) announced that its ordinary general assembly

meeting (OGM) has approved the proposal to distribute cash

dividends representing 60% of the nominal share value (SR6

per share), amounting to SR918mn. Out of this, interim

dividends for 1H2014 have already been distributed at the rate

of SR3.5 per share, representing 35% of the nominal share

value with a total amount of SR535.5mn. Entitlement to interim

dividends for the 2H2014 shall be to those shareholders who are

registered with the Tadawul at the close of trading on the day of

OGM. The dividend will be distributed on March 26, 2015.

(Tadawul)

Extra appoints new CEO – United Electronics Company

(Extra) has appointed Abdulhameed Abdulaziz Al Ohali as the

company’s new Chief Executive Officer (CEO), following the

resignation of Karim Al Dahabi who left for personal reasons.

However, Al Dahabi will continue to act as a strategic adviser for

the company. (GulfBase.com)

Savola unlikely to achieve quarterly target, expects 50%

shortfall – Savola Group announced that it will not be able to

achieve its forecasted net income of SR360mn in 1Q2015 and

the shortfall is expected to be around 50%. The revised

expected net income (before capital gain) for 1Q2015 is

SR178mn. The reasons for the expected shortfall are: lower

than forecasted sales in the retail sector during January and

February 2015, and the widening of deficit between planned and

actual income of the foods sector due to the impact of

devaluation of the local currencies in some countries, where

Savola operates, in addition to some operational difficulties.

(Tadawul)

JODI: Saudi crude exports reach highest level in 11 months

– According to the Joint Organisations Data Initiative (JODI),

crude oil exports from Saudi Arabia rose 7.8% in January 2015

to reach the highest level in 11 months. The Kingdom shipped

7.47mn barrels per day (bpd) of oil in January as compared to

6.93mn bpd in December 2014. KSA produced 9.68mn bpd of

crude in January, up 0.5% or 50,000 bpd, from December. The

growth in exports coincided with a 7.6% slide in the Brent crude

price, signaling that cheaper oil may be stimulating demand

amid a global surplus. (Bloomberg)

Du AGM approves AED0.2 dividend per share – Emirates

Integrated Telecommunications Company (Du) announced that

5. Page 5 of 6

its annual general meeting (AGM) has approved the proposed

distribution of AED0.2 per share cash dividend. (DFM)

UP seeks shareholders’ nod on cash, stock dividend –

Union Properties (UP) has invited its shareholders to consider

and approve the board of directors’ recommendation for

distributing 3% cash dividend and 5% bonus shares for the year

ended December 31, 2014. Shareholders will also consider

approving BoD recommendation not to allocate the 2014 net

profit to any other reserve, other than to statutory reserve.

(DFM)

EIBank AGM approves AED5mn dividend – Emirates

Investment Bank (EIBank) announced that its AGM has

approved the board’s recommendation to distribute scrip

dividend at 7.692% of the paid-up capital, amounting to

AED5mn. (DFM)

Mubadala Petroleum to explore Morocco offshore –

Mubadala Petroleum has agreed with the Moroccan government

to evaluate the hydrocarbon potential of a large area off the

Mediterranean coast of Morocco. The company obtained an

exclusive license to carry out a detailed geological survey of the

offshore area, which comprises 3,433 square kilometers.

Mubadala Petroleum will provide the survey results to the

Moroccan government, but the company did not elaborate on

the timetable and the prospects for finding oil or gas. (Reuters)

RWE to consider 10% stake sale to Abu Dhabi investors –

According to sources, German utility firm RWE is considering

selling a 10% stake to Abu Dhabi investors as it contends with

sliding prices and surging debt. Abu Dhabi’s Sheikh Mansour bin

Zayed Al Nahyan is among the investors who may participate in

the investment, which would be valued at about €1.5bn based

on RWE’s current market price. (Reuters)

NAPC AGM approves 13 baizas dividend per share –

National Aluminium Products Company (NAPC) announced that

its AGM has approved a total cash dividend of 13 baizas per

share, representing 13% of the value of each share. (MSM)

Dhofar Insurance AGM approves 9.5% cash dividend –

Dhofar Insurance Company announced that its AGM has

approved the proposed distribution of cash dividend to

shareholders equivalent to 9.5% of the company’s capital for the

year ended December 31, 2014. (MSM)

OEIHC gets extension on AED71.48mn government soft

loan – Oman & Emirates Investment Holding Company (OEIHC)

has received Abu Dhabi Investment Company’s approval

regarding the extension of a government soft loan, which was

due on October 29, 2014 up to November 1, 2025. The

outstanding loan amount of AED71.48mn will be repayable in six

annual equal installments commencing from November 1, 2020.

(MSM)

Omani bank’s lending growth slows slightly in January –

According to data from the Central Bank of Oman, lending

growth of banks in January 2015 edged down to 11.1% YoY

from 11.3% YoY achieved in December 2014. Meanwhile, M2

money supply growth accelerated to 14.1% YoY in January from

12.0% YoY in December. (Reuters)

BNH shareholders approve 20% cash dividend – Bahrain

National Holding (BNH) announced that its annual ordinary

general assembly has approved cash dividend of 20% of the

paid up capital, amounting to BHD2.1mn. (Bahrain Bourse)

KHCB, Tamkeen sign deal to back SME’s – Khaleeji

Commercial Bank (KHCB) has signed a new agreement with

Tamkeen to further expand the low financing options available to

small and medium-sized enterprises (SME’s) in Bahrain through

Tamkeen’s finance scheme. (Bahrain Bourse)

Batelco shareholders approve 25% cash dividend – Bahrain

Telecommunications Company (Batelco) announced that its

annual general meeting (AGM) and extraordinary general

meeting (EGM) approved the proposed agenda including the

distribution of cash dividend of 25% from the paid-up capital (of

which 10 fils per share was already distributed as interim

dividend for the year 2014). Accordingly, Batelco share shall

trade ex-dividend starting from March 19, 2015. (Bahrain

Bourse)

BFMC shareholders approve 20% cash dividend – Bahrain

Flour Mills Company (BFMC) announced that its annual general

meeting (AGM) and extraordinary general meeting (EGM)

approved the proposed agenda including the distribution of 20%

cash dividend from the paid up capital i.e. 20 fils per share.

(Bahrain Bourse)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Ahmed Al-Khoudary

Head of Research Senior Research Analyst Head of Sales Trading – Institutional

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6548

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa

Sahbi Kasraoui QNB Financial Services SPC

Manager – HNWI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Feb-11 Feb-12 Feb-13 Feb-14 Feb-15

QSE Index S&P Pan Arab S&P GCC

(1.8%)

(2.2%)

(0.8%)

(0.3%)

0.2%

(1.2%)

(3.6%)(4.2%)

(3.6%)

(3.0%)

(2.4%)

(1.8%)

(1.2%)

(0.6%)

0.0%

0.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,167.58 1.6 0.8 (1.5) MSCI World Index 1,754.10 1.0 2.0 2.6

Silver/Ounce 15.95 2.4 1.8 1.6 DJ Industrial 18,076.19 1.3 1.8 1.4

Crude Oil (Brent)/Barrel (FM

Future)

55.91 4.5 2.3 (2.5) S&P 500 2,099.50 1.2 2.2 2.0

Crude Oil (WTI)/Barrel (FM

Future)

44.66 2.8 (0.4) (16.2) NASDAQ 100 4,982.83 0.9 2.3 5.2

Natural Gas (Henry

Hub)/MMBtu

2.77 (0.8) 2.8 (7.6) STOXX 600 398.65 0.9 2.1 2.5

LPG Propane (Arab Gulf)/Ton 51.13 (1.4) (3.1) 4.3 DAX 11,922.77 0.1 1.7 6.5

LPG Butane (Arab Gulf)/Ton 57.75 (2.1) (4.3) (8.0) FTSE 100 6,945.20 1.5 3.1 0.1

Euro 1.09 2.5 3.5 (10.2) CAC 40 5,033.42 0.6 2.0 3.7

Yen 120.11 (1.0) (1.1) 0.3 Nikkei 19,544.48 0.9 1.8 10.6

GBP 1.50 1.6 1.6 (3.8) MSCI EM 956.73 0.8 1.8 0.0

CHF 1.02 2.8 2.7 1.6 SHANGHAI SE Composite 3,577.30 2.5 6.6 10.2

AUD 0.78 2.1 1.8 (4.9) HANG SENG 24,120.08 1.0 1.4 2.1

USD Index 98.55 (1.0) (1.8) 9.2 BSE SENSEX 28,622.12 (0.3) 1.2 5.0

RUB 59.45 (3.3) (4.5) (2.1) Bovespa 51,526.19 2.8 5.5 (16.5)

BRL 0.31 0.9 1.2 (17.5) RTS 841.05 2.2 0.9 6.4

164.2

133.7

122.9