1. UNITED STATES BANKRUPTCY COURT

SOUTHERN DISTRICT OF NEW YORK

In re: Chapter 11

1

Flat Out Crazy, LLC, et al. , Case No. 13-22094 (RDD

Debtors. Joint Administration Requested

AFFIDAVIT OF STEVE DELONG IN SUPPORT OF FIRST-DAY PLEADINGS

AND IN ACCORDANCE WITH LOCAL BANKRUPTCY RULE 1007-2

STATE OF ILLINOIS )

) ss.

COUNTY OF COOK )

I, Steve DeLong, being duly sworn, hereby depose and say:

1. I am the Interim Chief Financial Officer (“CFO”) of Flat Out Crazy, LLC

(“FOC”) and of each of the above-captioned affiliated debtors (collectively, the “Debtors”),

debtors and debtors in possession in these bankruptcy cases (the “Cases”). As an officer of the

Debtors, I am generally familiar with their day-to-day operations, businesses and financial

affairs.2

2. Debtor Stir Crazy Café West Nyack, LLC (“Stir Crazy West Nyack”) is a limited

liability company organized under the laws of the state of New York and has been so organized

for more than 180 days prior to the date on which these Cases commenced. Stir Crazy West

1

The Debtors in these cases and the last four digits of their Employer Identification Numbers are: Stir Crazy Café

West Nyack, LLC (5828); Flat Out Crazy, LLC (0160); SCR Operations, LLC (9375); SCR Hospitality, LLC

(4309); SCR Concessions, LLC (6669); Stir Crazy Restaurants, LLC (2289); Stir Crazy Café Oakbrook, LLC

(2976); Stir Crazy Café Northbrook, LLC (7070); Stir Crazy Café Woodfield, LLC (1104); Stir Crazy Café Great

Lakes, LLC (9634); Stir Crazy Café Boca Raton, LLC (9942); Stir Crazy Café Creve Coeur, LLC (0003); Stir Crazy

Café Legacy Village, LLC (8744); Stir Crazy Café Cantera, LLC (4842); and Stir Crazy Operations, LLC (8114).

2

I have been the Interim CFO at FOC since July, 2012. Until January 2013, I was an independent contractor for

Clark Schaefer Consulting (“Clark Schaefer”), who provided my services to the Debtors on a contract basis. During

January, 2013, the Debtors hired me as a full-time employee and terminated the service agreement with Clark

Schaefer.

CINCINNATI/97646.3

2. Nyack operates a Stir Crazy restaurant located at 4422 Palisades Center Drive, West Nyack, NY

10994. Debtor Stir Crazy Restaurants, LLC (“Stir Crazy Restaurants”) is the 100% owner of Stir

Crazy West Nyack. Debtor FOC is the 100% owner of Stir Crazy Restaurants. All of the other

Debtors are 100% owned, either directly or indirectly, by FOC, Stir Crazy Restaurants, or both

FOC and Stir Crazy Restaurants.3

3. On January 25, 2013 (the “Petition Date”), Stir Crazy West Nyack, Stir Crazy

Restaurants, FOC and all of the other Debtors filed voluntary petitions for relief (the “Petitions”)

under chapter 11 of title 11 of the United States Code, 11 U.S.C. §§ 101 et seq. (the “Bankruptcy

Code”) in the United States Bankruptcy Court for the Southern District of New York, White

Plains Division (the “Bankruptcy Court”).

4. In order to minimize disruption to the Debtors’ businesses as a result of the Cases,

maintain and maximize the value of the Debtors’ estates, and establish procedures for the

administration of the Cases, the Debtors have, contemporaneously herewith, requested certain

“first-day” relief by filing various motions and applications with the Bankruptcy Court

(collectively, the “First-Day Pleadings”).

5. I submit this affidavit (this “Affidavit”) (a) in support of (i) the Petitions and

(ii) the First-Day Pleadings; and (b) to assist the Bankruptcy Court and other interested parties in

understanding the circumstances that resulted in the commencement of the Cases. All facts set

forth in this Affidavit are based upon my personal knowledge, my discussions with other

members of the Debtors’ officers and current senior management, my review of relevant

documents, or my opinion based upon experience, knowledge, and information concerning the

operation of the Debtors and the industry in which they operate. While I have made every

3

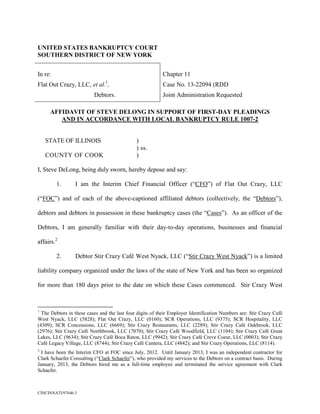

An organization chart depicting the ownership structure of all of the Debtors is attached hereto as Exhibit A.

CINCINNATI/97646.3 2

3. reasonable effort to ensure that the information contained herein is accurate and complete based

upon information that was available at the time of preparation, the subsequent receipt of

information may result in material changes to financial data and other information contained

herein. If called to testify, I would testify competently to the facts set forth in this Affidavit. I

am authorized to submit this Affidavit on behalf of the Debtors.

BACKGROUND AND HISTORY

The Business of the Debtors

6. As of the Petition Date, the Debtors operate 26 restaurants, split among two

Asian-inspired chains: (i) Flat Top Grill (“Flat Top”), which currently has 15 locations; (ii) Stir

Crazy Fresh Asian Grill (“Stir Crazy” and, together with Flat Top, the “Restaurants”), which

currently has 11 locations.4 As of the end of their last payroll period on January 16, 2013, the

Debtors employed approximately 1,200 people, the majority of whom were employees in the

Restaurants or in Director of Operations positions and 14 of whom were located at the Debtors’

corporate headquarters in downtown Chicago. During January, 2013, immediately prior to the

Petition Date, the Debtors closed (a) 3 Stir Crazy restaurants located in Greenwood, Indiana;

Indianapolis, Indiana; and Warrenville, Illinois; (b) 3 Flat Top restaurants located in

Birmingham, Alabama; Rochester Hills, Michigan; and Wauwatosa, Wisconsin; and (c) the sold

SC Asian restaurant located in San Francisco, California.

7. Flat Top is a full-service fast-casual create-your-own stir-fry concept that

combines the comforts of a full-service restaurant with an interactive dining experience. The

first Flat Top opened in Chicago in 1995 with a vision to bring fresh, Asian-style cooking to the

4

The Debtors also operated a single-location Asian fast-casual restaurant (“SC Asian”), which the Debtors closed

immediately prior to the Petition Date.

CINCINNATI/97646.3 3

4. United States. Diners at Flat Top pay a value-oriented price, entitling them to take a trip through

“The Fresh Food Line” to create a unique dish.

8. Stir Crazy is a full-service casual Asian restaurant offering the flavors of Chinese,

Japanese, Thai and Vietnamese food. Like Flat Top, the first Stir Crazy also opened in suburban

Chicago in 1995. Stir Crazy prepares everything from scratch daily. The focal point of each Stir

Crazy is an open-kitchen that allows diners to watch skilled chefs use woks to prepare

ingredients chosen by diners selecting the “Market Bar” menu option. Its menu also offers more

than 50 other dishes ranging from traditional Chinese favorites to innovative specialties from

across Asia.

9. SC Asian was a single-location, full-service fast-casual restaurant where guests

order and pay for Asian cuisine at the counter and then sit down to be served food and drinks by

service staff who take additional orders tableside. SC Asian opened its first and only location in

November 2011 inside Macy’s flagship department store in San Francisco, California.5

10. By 1999, Stir Crazy had grown into a four-restaurant chain, with 3 locations in

suburban Chicago and one location in suburban Detroit. Over the next 5 years, Stir Crazy more

than doubled its number of locations, opening stores in south Florida; suburban Chicago;

suburban St. Louis, Missouri; the outskirts of New York City; and suburban Cleveland, Ohio.

Most of these Restaurants were located in regional malls or lifestyle centers, with the others

located in free-standing buildings.

11. In 2006, The Walnut Group (“Walnut Group”), a private equity firm located in

Cincinnati, Ohio, and certain of its affiliates formed Stir Crazy Partners, LLC, which then

acquired Stir Crazy Restaurants and all of its subsidiaries (the “Stir Crazy Acquisition”). At the

5

As noted above, this location was closed in January 2013.

CINCINNATI/97646.3 4

5. time of the Stir Crazy Acquisition, Stir Crazy operated 9 locations. During 2007 and 2008, Stir

Crazy opened 5 new locations, bringing the total Stir Crazy locations to 14 by the end of 2008.

12. FOC was formed in 2009 to acquire the Flat Top chain and merge it with Stir

Crazy. On August 19, 2009, FOC acquired a 100% interest in Stir Crazy Restaurants and its

subsidiaries from Stir Crazy Partners, LLC. On the same day, FOC also acquired certain assets

and liabilities of Happy Valley Corporation, formerly the owner of Flat Top (collectively, these

transactions are referred to herein as the “Flat Top Acquisition”). At the time of the Flat Top

Acquisition, Flat Top operated 13 Restaurants. Following the Flat Top Acquisition, there were

27 total Restaurants under the control of FOC and its subsidiaries.

Financial Results and Distress

13. Subsequent to the Flat Top Acquisition, the Debtors continued to grow by adding

new Restaurants. At their peak in early 2012, the Debtors operated 37 total Restaurants – 18 Stir

Crazy locations, 18 Flat Top locations and the SC Asian location. During 2012, the Debtors’ net

sales peaked at approximately $59.0 million, representing an increase of approximately $2.4

million over 2011 net sales and approximately $6.7 million over 2010 net sales. Despite the

growth trend in Restaurant sales, the company as a whole was not profitable.

14. The extended lull in the U.S. economy, unsuccessful new Restaurant openings

and unprofitable menu changes led to poorer-than-expected results, particularly in 2011 and

2012. During 2012, the Debtors sustained a preliminary unaudited net loss of approximately

$11.5 million. The Debtors also sustained net losses of approximately $12.2 million in 2011 and

$3.6 million in 2010.

15. The mounting losses have put a significant strain on the Debtors’ cash flow,

which in turn has stressed their relationships with lenders, landlords, vendors and other parties in

CINCINNATI/97646.3 5

6. interest. Over the past several months, the Debtors have explored numerous restructuring

alternatives, including but not limited to, Restaurant performance improvements, capital raises,

asset transactions, closing unprofitable Restaurants, and others. Members of the board of

directors of FOC (the “Board”) and senior management of the Debtors have been in constant

contact regarding these efforts and they have regularly met to develop a business plan that will

help ensure the long-term viability of the Debtors. Pursuant to these efforts, the Board replaced

several members of the Debtors’ senior management team during 2012, bringing in William Van

Epps as CEO and myself to replace the prior CFO who resigned. Mr. Van Epps has more than

40 years of foodservice experience. Mr. Van Epps was previously President, USA, Papa John’s

International, Inc., responsible for the company’s domestic franchise and company restaurant

operations, restaurant development, franchising, marketing, R&D, and quality management.

Prior to joining Papa John’s, Van Epps served for two years as President of the International

Division of Yorkshire Global Restaurants (Long John Silver’s and A&W Restaurants); six years

with AFC Enterprises, including President of its International Division (Churchs, Popeye’s,

Cinnabon and Seattle Coffee Co.) and seven years with PepsiCo International (Pizza Hut). I am

a certified public accountant in the state of Ohio and I have more than 30 years of financial

management experience in industry with both public and private companies. I began my career

in the Dayton, Ohio offices of Deloitte. Until January 2013, I was an independent contractor of

the Debtors through the firm of Clark Schaefer Consulting, who provided my services to the

Debtors on a contract basis. During January, 2013, the Debtors hired me as a full-time employee

and terminated the service agreement with Clark Schaefer.

16. Additionally, as described below, among their First-Day Pleadings, the Debtors

are seeking to retain William H. Henrich and Mark Samson from the advisory firm of Getzler

CINCINNATI/97646.3 6

7. Henrich & Associates LLC (“Getzler Henrich”) as their Co-Chief Restructuring Officers in the

Cases. Messrs. Henrich and Samson and Getzler Henrich have been working with the Debtors

since December to provide advice and analysis in connection with a restructuring.

17. The Debtors believe that they have the right management team to fix the

businesses, provide necessary leadership to guide them through the Cases, and emerge from the

Cases as stronger entities with a viable long-term future.

The Debtors’ Capital Structure: Long-Term Debt

18. Debtor FOC, as Borrower (the “Borrower”), and U.S. Bank National Association

(“U.S. Bank”), as Lender, are parties to that certain Loan Agreement dated as of April 21, 2010

(as amended from time to time, the “Senior Prepetition Loan Agreement”), pursuant to which

FOC entered into a 3-year revolving credit facility (the “Senior Prepetition Facility”) with the

ability to borrow funds and issue letters of credit in an aggregate amount of up to $3 million.

The loan is evidenced by that certain Revolving Credit Note in the face amount of $3,000,000

dated as of April 21, 2010 (the “Senior Prepetition Note”). The Senior Prepetition Loan

Agreement, the Senior Prepetition Note, and all agreements and documents entered into and/or

executed in connection therewith (including, without limitation, a Guaranty, a Security

Agreement by the Borrower, a Security Agreement by the Guarantors, and a Patent, Trademark

and License Security Agreement), each dated as of April 21, 2010, are referred to herein as the

“Senior Prepetition Loan Documents.”

19. The Borrower’s obligations under the Senior Prepetition Facility (the “Senior

Prepetition Obligations”) are guaranteed by each of the other Debtors (the “Prepetition

Guarantors”) and are secured by first priority senior liens on and security interests in

substantially all of the assets of the Debtors (the “Prepetition Senior Collateral”), subject to

CINCINNATI/97646.3 7

8. certain exceptions.6 The Pre-Petition Senior Collateral does not include certain specified

equipment (the “Vogen Equipment”) that is the subject of separate financing provided by Vogen

Funding, L.P. (“Vogen”) (an affiliate of CapX Partners) pursuant to that certain Master Lease

Agreement dated as of December 14, 2007 and various subsequent lease supplements

(collectively, the “Vogen Equipment Financing Agreement”).

20. The Debtors and U.S. Bank have amended the Senior Prepetition Loan

Documents from time to time. The Third Amendment to the Senior Prepetition Loan Agreement

(the “Third Amendment”), executed on June 28, 2011, increased the maximum borrowings under

the facility to $6 million and removed many financial covenants, leaving only a fixed charge

coverage ratio and a maximum consolidated total leverage ratio. Pursuant to the Third

Amendment, the maturity date of the Senior Prepetition Facility was also extended to June 28,

2014.

21. Payments on the Senior Prepetition Facility are interest only, due monthly in

arrears, and based on LIBOR plus 2.00% plus the applicable LIBOR margin. As of January 18,

2013, the outstanding principal amount of loans under the Senior Prepetition Facility totaled

approximately $5.9 million. As discussed below, on January 18, 2013 U.S. Bank sold and

assigned all of its rights, title, and interest with respect to the Senior Prepetition Facility (the

“HillStreet Assignment”) to the Debtors’ second lien lender, The HillStreet Fund IV, L.P.

(“HillStreet”), and HillStreet agreed to reduce the principal amount of the Senior Prepetition

Facility.

6

Nothing contained herein is intended to admit, or waive any right to contest, the validity, enforceability, perfection

or other attributes concerning any liens, claims, interests or rights of any party. The Debtors and their estates

reserve the right to contest the validity, enforceability, perfection and any other attributes of any such liens, claims,

interests or rights..

CINCINNATI/97646.3 8

9. 22. The Debtors also have outstanding under the Senior Prepetition Facility an

Irrevocable, Unconditional Standby Letter of Credit No. SLCLSTL07512 (the “Letter of Credit”)

which was issued by U.S. Bank in favor of 315 W. North Ave., L.P., one of the Debtors’

landlords, which, to the best of the Debtors’ knowledge, was undrawn as of the Petition Date.

The Letter of Credit was originally issued in the amount of $75,000 (the “L/C Amount”).

According to its terms, the L/C Amount would automatically decrease in increments of $25,000

on each of January 1, 2012, April 1, 2012, and June 30, 2012. On June 28, 2012, two days

before the L/C Amount (which was then in the reduced amount of $25,000 due to prior

automatic reductions) was scheduled to reduce to zero dollars, the Letter of Credit was amended

to provide: (1) the expiration date was extended from June 30, 2012 to June 30, 2013, and (2) the

then available L/C Amount was increased by $20,000 to a new balance of $45,000. The

amendment did not alter the automatic reduction schedule and, thus, on June 30, 2012, the L/C

Amount was automatically reduced to $20,000.

23. Concurrently with entering into the Senior Prepetition Facility with U.S. Bank,

the Borrower entered into a certain Loan and Security Agreement dated as of April 21, 2010 with

HillStreet (the “Junior Prepetition Loan Agreement”), pursuant to which the Borrower obtained a

$5 million seven-year term loan (the “Junior Prepetition Term Loan”) maturing on April 21,

2017. The loan is evidenced by a promissory note in the face amount of $5,000,000 dated as of

April 21, 2010 (the “Junior Prepetition Note”). The Junior Prepetition Loan Agreement, the

Junior Prepetition Note, and all agreements and documents entered into and/or executed in

connection therewith are referred to herein as the “Junior Prepetition Loan Documents.”

24. The Borrower’s obligations under the Junior Prepetition Term Loan (the “Junior

Prepetition Obligations”) are guaranteed by each of the Prepetition Guarantors and are secured

CINCINNATI/97646.3 9

10. by second priority liens on and security interests in substantially all of the assets of the Debtors

(the “Prepetition Junior Collateral” and together with the Prepetition Senior Collateral, the

“Prepetition Collateral”), subject to certain exceptions. The Pre-Petition Junior Collateral does

not include the Vogen Equipment.

25. The Junior Prepetition Term Loan accrues interest at 16%, of which 12% is

payable monthly, in arrears, and 4% is deferred and payable on the maturity date of the loan. The

principal of the Junior Prepetition Term Loan is payable in full on April 21, 2017. Amendment

No. 1 to the Junior Prepetition Term Loan was executed concurrently with the Third Amendment

to the Senior Prepetition Loan Agreement on June 28, 2011. Amendment No. 1 was issued to

match the new covenants on the Senior Prepetition Facility. The Junior Prepetition Term Loan

was amended two other times, on February 21, 2012 in connection with the Debtors’ entry into

the First Bridge Loan (as defined below) and on August 31, 2012 in connection with the

Debtors’ entry into the Second Bridge Loan (as defined below). The Junior Prepetition Term

Loan is contractually subordinated to the Senior Prepetition Facility. There are various

subordination agreements among the Debtors, U.S. Bank and HillStreet that govern the relative

rights and interests of the parties.

26. The interest rate on the Junior Prepetition Term Loan was amended by a

forbearance agreement entered into in September 2012, which expired on January 15, 2013. An

extra 3% was added to the annual interest rate by this agreement. Also, additional interest of

0.5% per month was added. As of the Petition Date, the outstanding balance of the Junior

Prepetition Term Loan, including principal and accrued interest was approximately $6 million.

27. In order to address cash shortfalls, on February 21, 2012, the Debtors borrowed

$1.36 million on a junior, unsecured basis from a group of lenders (the “First Bridge Lenders”),

CINCINNATI/97646.3 10

11. pursuant to a Bridge Loan Agreement (the “First Bridge Loan”). The First Bridge Loan was

evidenced by a series of 15.0% promissory notes executed by FOC in favor of the First Bridge

Lenders. The First Bridge Loan was fully drawn. These notes became due and payable upon

demand six months after the date of their execution. The First Bridge Lenders are primarily

investors in Walnut Group.

28. On August 31, 2012, again in order to attempt to stem cash shortfalls, the Debtors

borrowed $1.705 million on a junior, unsecured basis from a group of lenders (the “Second

Bridge Lenders”), pursuant to a Bridge Loan Agreement dated August 31, 2012 and an Amended

and Restated Bridge Loan Agreement dated August 31, 2012 (collectively, the “Second Bridge

Loan” and, together with the First Bridge Loan, the “Bridge Loans”). The Second Bridge Loan

was evidenced by a series of 15.0% promissory notes executed by FOC in favor of the Second

Bridge Lenders. The Second Bridge Loan was fully drawn. The Second Bridge Lenders are

primarily investors in Walnut Group, and there is substantial overlap between the members of

the First Bridge Lenders and the Second Bridge Lenders. These notes are due and payable upon

demand any time after December 31, 2013. As of the Petition Date, the total principal amount of

the Bridge Loans was $3.065 million.

29. The Bridge Loans are contractually subordinated in priority to the Senior

Prepetition Facility and the Junior Prepetition Term Loan.

30. As a result of continuing operating losses, the Debtors have been unable to remain

in compliance with the financial covenants arising under substantially all of their debt

agreements. The Debtors’ are in default of the Senior Prepetition Loan Documents and the

Junior Prepetition Loan Documents. Since fiscal 2011, a total of approximately $10.9 million of

long-term debt was subject to accelerated maturity as a result of covenant defaults. As a result,

CINCINNATI/97646.3 11

12. the total amount of the long-term debt has been classified as a current liability in the Debtors’

consolidated balance sheets as long-term debt in default since the consolidated balance sheet

dated December 28, 2011. Despite the covenant defaults, the Debtors have continued to make

scheduled payments of interest on the Senior Prepetition Facility. The Debtors stopped making

interest payments on the Junior Prepetition Term Loan on or about July 1, 2012.

31. On January 18, 2013, U.S. Bank sold and assigned all of its right and interest in

the Senior Prepetition Facility and the related loan documents to HillStreet (the “Assignment”).

Also on January 18, 2013, immediately upon closing of the Assignment, HillStreet and FOC

entered into that certain Sixth Amendment to Loan Agreement (the “Sixth Amendment”) by

which, among other things, HillStreet agreed to reduce the maximum principal amount of loans

under the Senior Prepetition Loan Agreement to $1,250,000 and HillStreet committed to extend

additional loans under the Senior Prepetition Facility up to $250,000. Thus, as of the Petition

Date, HillStreet holds all of the secured debt of the Debtors which totaled approximately $6.25

million in principal amount, after the agreed upon principal reduction under the Sixth

Amendment.

The Debtors’ Capital Structure: Equity

32. FOC is a Delaware limited liability company that is privately held by investors

holding common and preferred equity securities in several classes. None of the equity securities

of any of the Debtors is publicly traded.

33. FOC facilitated its merger with Flat Top and provided working capital for growth

with the issuance of Series C Participating Preferred Membership Units (“Preferred Units”).

During Fiscal 2009, FOC issued 385,044 shares of Preferred Units for proceeds of approximately

$3.9 million. The Preferred Units were offered with a 7% distribution rate and additional

CINCINNATI/97646.3 12

13. warrants. The warrants may be exercised at the earlier of one (1) year from the date of issuance

or ten (10) days prior to an Initial Public Offering at an exercise price of $0.01 per share. As of

the Petition Date, the warrants have not been exercised.

34. Series A Preferred Units were issued to Happy Valley Corporation and Series A

Common Units were issued to the shareholders of Happy Valley Corporation in exchange for

substantially all of the assets and liabilities that became FOC. In 2010, certain Happy Valley

Corporation shareholders exchanged their interest in Happy Valley Corporation for a direct

interest in FOC by exchanging stock in Happy Valley Corporation for 302,214 shares of Series A

Preferred Units and 302,214 shares of Series A Common Units, held by Happy Valley

Corporation. As of the Petition Date, 801,166 Series A Preferred Units and 801,166 Series A

Common Units were issued and outstanding, respectively. The Series A Common Units do not

have a par value.

35. Series B Preferred Units and Series B Common Units were issued to Stir Crazy

Partners, LLC in exchange for a 100% interest in Stir Crazy Restaurants, LLC. As of the Petition

Date, 1,599,239 Series B Preferred Units and 1,599,239 Series B Common Units were issued and

outstanding, respectively. The Series B Common Units do not have a par value.

36. Common Units entitle the holder to vote equal to its Percentage Interest held.

Series A and B Common Units have an Interest in Profits only, whereas the Series C Common

Units have an interest in Capital and Profits. The Common Units do not have a stated value. As

of the Petition Date, there were 2,400,405 Common Units outstanding, excluding Series C

common warrants.

37. Additionally, in connection with the Junior Prepetition Term Loan, FOC issued

293,000 Series D Preferred Unit detachable warrants to HillStreet. The warrants entitle

CINCINNATI/97646.3 13

14. HillStreet to purchase Series D Preferred Units equal to 5% of FOC at an exercise price of

$0.0001 per unit. The warrants have a ten-year expiration. The warrants are exercisable at any

time during the ten year period. The warrants have a put option in year 7, or upon sale or merger

that entitle HillStreet to redeem the warrants for cash for an amount as defined in the Junior

Prepetition Loan Documents.

Trade Debt

38. The Debtors’ trade debt consists of, among other things, amounts owed to

maintenance vendors who repair and maintain HVAC, grease traps, range hoods, and

refrigeration units in the Restaurants, food suppliers, utilities, and suppliers of uniforms, plates,

silverware, napkins and other nonperishables used in the Debtors’ Restaurants. The majority of

the Debtors’ vendors are paid on negotiated terms, which have historically ranged from 30 to 60

days from the date of delivery. Currently, many of the Debtors’ vendors have stated terms of 30

days or less or COD, but the Debtors have stretched many vendors well-beyond 30 days because

of their cash situation. As of the Petition Date, the Debtors estimate that approximately $5

million is outstanding to their vendors, much of which relates to goods and services provided to

the Debtors in the 20 days prior to the Petition Date.

Lease Obligations

39. All of the Restaurants are located on leased properties. The Debtors estimate that

they will have spent approximately $6.0 million on real property lease expenses during the 2012

fiscal year and that as of the Petition Date, their aggregate total outstanding real property lease

obligations are nearly $1.5 million. The Debtors are in default under many of their leases due to

late or non-payment and certain landlords have commenced remedial action to enforce the leases.

CINCINNATI/97646.3 14

15. None of these landlord actions has resulted in the termination of leases under which the Debtors

are operating Restaurants as of the Petition Date.

40. In the ordinary course of business, the Debtors also finance the majority of the

equipment in their Restaurants in accordance with the terms of the Vogen Equipment Financing

Agreement with Vogen. As of the Petition Date, the aggregate total amount outstanding under

the Vogen Equipment Financing Agreement was approximately $3.9 million. The Debtors have

undertaken an analysis of the Vogen Equipment Financing Agreement and have reached a

preliminary conclusion that the obligations are in the nature of a secured financing and not in the

nature of a true lease. The Debtors reserve their rights with respect to this issue.

Restructuring Efforts and Events Leading to Bankruptcy

41. In the weeks and months leading up to the Petition Date, due to poor operating

results and to improve cash flow, the Debtors closed 7 Stir Crazy locations and 3 Flat Top

locations.7 As of the Petition Date, the Debtors operated 27 total Restaurants.

42. Most of the Flat Top restaurants are located in and around Chicago, with several

located elsewhere in Illinois, Indiana, Michigan, and Wisconsin. In the weeks leading up to the

Petition Date, the Debtors closed 3 Flat Top restaurants located in Alabama, Michigan, and

Wisconsin due to poor operating results.

43. Stir Crazy restaurants are located in Florida, Illinois, Michigan, Missouri, New

York, Ohio, and Wisconsin. In the weeks leading up to the Petition Date, the Debtors closed 3

Stir Crazy sites located in Illinois and Indiana due to poor operating results. During 2012, the

Debtors closed 4 other Stir Crazy restaurants located in Georgia, Minnesota, and Texas.

7

The 7 closed Stir Crazy restaurants were located in Atlanta, Georgia; Greenwood, Indiana; Indianapolis, Indiana;

Warrenville, Illinois; Bloomington, Minnesota; The Woodlands, Texas; and Southlake, Texas. The 3 closed Flat

Top restaurants were located in Birmingham, Alabama; Rochester Hills, Michigan; and Wauwatosa, Wisconsin.

CINCINNATI/97646.3 15

16. 44. Throughout 2012, the Debtors engaged in various efforts to restructure their

operations and debt, as well as pursue a variety of sale and financing transactions. In that regard,

the Debtors hired various brokers and investment bankers to pursue these transactions. None of

these efforts resulted in a transaction. Among the investment bankers retained by the Debtors in

2012 was J.H. Chapman Group, LLC (“Chapman”), a Chicago based investment banking firm.

Chapman has substantial restaurant and foodservice expertise and has made substantial efforts to

identify a potential buyer for the Flat Top restaurant business. As described in greater detail

below, the Debtors intend to seek approval of the Bankruptcy Court to conduct a sale process

and auction for the Flat Top restaurant business and related assets.

45. In the fourth quarter of 2012, the Debtors hired Squire Sanders (US) LLP as their

restructuring attorneys and Getzler Henrich as their financial advisors. As described in greater

detail below, both firms are highly-qualified advisors of distressed entities, who possess

restructuring skills and experience that is appropriate and needed during the Cases. Since early

December 2012, the Debtors attorneys and financial advisors have been generally advising the

Debtors in connection with their distressed situation; negotiating with lenders, other creditors

and parties in interest; developing budgets and financial projections necessary to obtain

additional financing; preparing the filings necessary to commence the Cases; and performing

other tasks at the Debtors’ request.

46. The Debtors are facing a severe liquidity shortfall and were not able to obtain

debtor in possession financing on reasonable terms prior the Petition Date. The inability of the

Debtors to obtain DIP financing prior to the Petition Date is due in large part to the actions of

HillStreet. As described above, HillStreet is the holder of the first and second lien debt to the

Debtors. HillStreet, who provided second lien financing to the Debtors in April, 2010, acquired

CINCINNATI/97646.3 16

17. the first lien debt from U.S. Bank pursuant to the HillStreet Assignment on January 18, 2013 and

immediately entered into a loan amendment under which the principal amount of the first lien

debt was reduced from approximately $6 million to $1.25 million.

47. In connection with the Debtors’ acknowledgment of the HillStreet Assignment,

which was required by U.S. Bank as a condition to closing, HillStreet provided specific oral

assurances to the Debtors on January 17, 2013 that it would agree (1) to write down the principal

amount of the first lien debt to $1.25 million, (2) to advance an additional $250,000 to the

Debtors pre-petition and (3) to provide adequate debtor in possession financing for a consensual

chapter 11 filing on certain terms specifically discussed by the parties. On the basis of such

assurances, the Debtors ceased their efforts to seek alternative financing and focused all of their

attention and resources on documenting debtor in possession financing with HillStreet.

48. Unfortunately, while HillStreet agreed to write down the first lien debt and fund

the additional pre-petition loan, HillStreet failed to live up to its assurances on providing debtor

in possession financing on the agreed terms. For example, after committing to provide $1.75

million in financing ($250,000 pre-petition and $1.5 million in debtor in possession financing),

HillStreet reneged and demanded a loan amount reduction of $600,000. Similarly, after

committing to provide financing both before and after the completion of a section 363 sale

process, HillStreet reneged and refused to provide any financing post-sale.

49. Despite herculean efforts over the course of the last week by the Debtors to

overcome numerous new and unreasonable conditions to financing imposed by HillStreet, the

Debtors have not been able to reach an agreement with HillStreet on reasonable terms that would

allow the Debtors to operate in chapter 11 and pursue its reorganization. The timing of

CINCINNATI/97646.3 17

18. HillStreet’s actions8, coupled with the severe liquidity crisis facing the Debtors, has necessitated

that the Debtors commence these Cases without debtor in possession financing. However, the

Debtors are able to operate for the initial five week period of the Cases on use of cash collateral

and without new financing.

50. The Debtors require relief in the form of a “breathing spell” from their obligations

to creditors and an opportunity to reorganize. Accordingly, the Debtors filed the Cases on the

Petition Date in an attempt to achieve such relief. Another reason for filing the Cases was to

facilitate the sale of certain assets to potential purchasers whom the Debtors expect will require

the protections of the Bankruptcy Code in order to enter into transactions with the Debtors.

Additionally, the Debtors view the Cases as an opportunity to achieve a capital structure that will

be more easily supported by the Debtors’ now-smaller enterprise. These are the primary reasons

that the Debtors commenced the Cases.

FACTS IN SUPPORT OF FIRST-DAY PLEADINGS

51. Concurrently with the filing of the Petitions initiating the Case, the Debtors also

filed a number of First-Day Pleadings. The Debtors anticipate that the Bankruptcy Court will

conduct a hearing soon after the commencement of the Case (the “First-Day Hearing”) at which

the Court will hear and consider the First-Day Pleadings. The Debtor also anticipates that the

Bankruptcy Court may consider the remainder of the First-Day Pleadings at a later time. Those

8

Until mid-December 2012, HillStreet continually had a designated director on the board of Debtor Flat Out Crazy,

LLC and, thus, has had intimate knowledge of and involvement with virtually all the Debtors’ restructuring efforts.

The HillStreet Director resigned on or about December 17, 2012. Subsequently, on January 12, 2013, HillStreet

designated its principal, Christian Meininger, as the replacement HillStreet Director. Mr. Meininger was the

primary HillStreet representative negotiating with the Debtors concerning providing debtor in possession financing.

While he was a director, Mr. Meininger specifically provided the assurances of HillStreet that are described above at

a meeting on January 17, 2013 and on which the Debtors relied. Later on January 17, 2013, Mr. Meininger resigned

from the Board presumably because of the conflict represented by HillStreet’s agreement to provide debtor in

possession financing.

CINCINNATI/97646.3 18

19. First-Day Pleadings that the Debtor anticipates will be heard at the First-Day Hearing are

described below.9

52. The relief sought in the First-Day Pleadings is intended to: (a) allow the Debtors

to minimize disruption to its business to the extent necessary and appropriate to maximize the

value of the Debtors’ estates and (b) minimize potential adverse consequences that might

otherwise result from the commencement of the Case. More specifically, the First-Day

Pleadings seek relief allowing the Debtors to (i) obtain post-petition financing; (ii) facilitate a

possible sale of the Flat Top restaurants to an outside party; (iii) rebuild the trust of vendors,

landlords and other creditors in order to allow the Debtors to operate their businesses with as

little interruption as possible; and (iv) begin certain procedures that will provide for the efficient

administration of the Cases.

53. I have reviewed each of the First-Day Pleadings, including the exhibits thereto,

and I believe that the relief sought in each of the First-Day Pleadings is tailored to meet the goals

described above and, ultimately, will be integral to the Debtors’ collective ability to preserve and

maximize the value of their estates.

54. I also believe that it is critical for the First-Day Pleadings to be heard as soon as

possible. If the First-Day Pleadings are not heard on an expedited basis, the Debtors may be

unable to fulfill their obligations to its creditors, regulators, the Non-Debtor Subsidiaries, and

other constituents. Under such circumstances, I believe that the Debtor will not be able to

operate. Such a stoppage could negatively impact the Debtor and the Non-Debtor Subsidiaries,

specifically including the Bank, which could create widespread injury to the Debtor’s estate, its

creditors and the Non-Debtor Subsidiaries. Accordingly, the expedited review of the First-Day

9

Capitalized terms used in the descriptions of the First-Day Pleadings and not otherwise defined herein have the

meanings given in the applicable First-Day Pleadings.

CINCINNATI/97646.3 19

20. Pleadings is important to the continuing viability of the Debtor and the Non-Debtor Subsidiaries

and therefore I believe it to be in the best interests of all interested parties.

55. Several of the First-Day Pleadings request authority to pay certain prepetition

claims of the Debtors. Rule 6003 of the Federal Rules of Bankruptcy Procedure (the

“Bankruptcy Rules”) provides that, “[e]xcept to the extent that relief is necessary to avoid

immediate and irreparable harm, the court shall not, within 21 days after filing of the petition,

issue an order…” authorizing the payment of prepetition claims. In respect of this rule, the

Debtors have narrowly-tailored all First-Day Pleadings so that they are only seeking to pay

prepetition claims in instances where the failure to pay such claims would result in immediate

and irreparable harm.

Use of Cash Collateral and Case Administration Motions

a. Use of Cash Collateral

56. The Debtors filed a motion seeking authority to use cash collateral under

section 363(b) of the Bankruptcy Code (the “Cash Collateral Motion”) for a period of five weeks

through the week ending March 3, 2013 (the “Interim Period”). Absent granting the Debtors use

of cash collateral on the terms provided herein, the Debtors are unable to operate their businesses

and likely have no other reasonable alternative but to liquidate. It is beyond dispute that the best

way to maximize the value of the Debtors’ estates for the benefit of all stakeholders is to

continue to operate their restaurants on a “business as usual” basis. If the Debtors are not

permitted to continue to operate in chapter 11, there would be a resulting loss of employment for

the Debtors’ approximately 1,200 employees and the likely inability to provide any meaningful

recovery to their creditors.10

10

The Debtors’ assets consist principally of equipment (most of which is leased), real estate leases, food and other

inventory. If the Debtors are forced to liquidate, the value of their assets is estimated to be less than $750,000.

CINCINNATI/97646.3 20

21. 57. Based on the Debtors’ cash collateral budget (a copy of which is attached to the

Debtors’ Cash Collateral Motion), the Debtors will have sufficient cash available from ordinary

operations to conduct their business and pay their operating expenses for five weeks. During this

period the Debtors have a reasonable expectation of signing an asset purchase agreement with a

stalking horse bidder to acquire the Flat Top Grill restaurant assets11 and obtaining debtor in

possession financing in an amount and on terms sufficient to complete a section 363 auction

process, subject to the approval of the Court, and a reorganization of the remaining business.

Pursuing this plan will maximize the value of the Debtors’ estates.

58. As stated above, the Debtors were unable to obtain debtor in possession financing

prior to the Petition Date due the actions of HillStreet, who after agreeing to provide such

financing reneged on such agreement just days before the intended commencement of the Cases.

The Debtors’ cash collateral budget demonstrates their ability to operate without any financing

during the first five weeks of the Cases. During this period, the Debtors expect that they will

have generated cash receipts totaling approximately $5.0 million and will pay expenses in the

amount of approximately $5.0 million. Additional details of the cash budget are contained in the

Cash Collateral Motion.

59. Ample cause exists to authorize the Debtors to use cash collateral in accordance

with their cash collateral budget and on the terms requested herein. The Debtors will provide

adequate protection to HillStreet by granting HillStreet replacement liens on all of the Debtors’

11

On January 19, 2013, the Debtors signed a non-binding letter of intent with a potential buyer for the Flat Top Grill

restaurant assets for a purchase price that exceeds the amount of the Debtor’s secured obligations to HillStreet. The

buyer is fully engaged in conducting due diligence and the parties expect to begin negotiating the terms of an asset

purchase agreement shortly with the expectation that an agreement can be reached within a few weeks. The

agreement would provide for the buyer to serve as a stalking horse in a customary, albeit expedited, section 363 sale

process. The Debtors intend to file a motion for authority to conduct such a sale process on or about January 31,

2013 and intend to establish a timeline for sale procedures that will accommodate the anticipated timing by which

the Debtors hope to execute an agreement with the buyer to serve as a stalking horse, subject to the approval of the

Court.

CINCINNATI/97646.3 21

22. property against which HillStreet has a valid, perfected, enforceable lien and security interest as

of the Petition Date. Moreover, the Debtors do not expect the value of their assets or the

business to decline in value during the period in which the Debtors are authorized to use cash

collateral. The Debtors submit that HillStreet will not be prejudiced by the relief requested

herein. To the contrary, as the Debtors’ senior secured creditor, HillStreet will benefit the most

from the Debtors’ efforts to maintain and enhance the value of their assets. This is even more so

once the Debtors are able to reach an agreement on an asset purchase agreement for the sale of

the Flat Top Grill assets.

60. In sum, the Debtors believe that, with the opportunity to continue their business

operating normally in chapter 11, they will be able to obtain adequate financing to complete a

section 363 auction process and a reorganization of the remaining business. Without this

opportunity, which hinges on the Court’s authorization to use cash collateral, the Debtors will be

unable to maximize the value of their assets and provide recoveries to their stakeholders.

b. Expedited Hearings on the First-Day Pleadings

61. Given the importance of the relief sought in the First-Day Pleadings to the

Debtors’ ability to preserve the value of their estates as they seek to reorganize, the Debtors have

filed a motion seeking entry of an order scheduling an expedited hearing on the First-Day

Pleadings.

c. Joint Administration

62. There are fifteen affiliated Debtors in the Cases. To ease the administrative

burden on the Debtors and their professionals and to prevent unnecessary duplication of work

related to matters that apply to the Debtors collectively, the Debtors have requested that the

Bankruptcy Court enter an order authorizing and directing (a) the consolidation and joint

administration of the Cases for procedural purposes only pursuant to Bankruptcy Rule 1015(b);

CINCINNATI/97646.3 22

23. (b) the use of single case docket and Bankruptcy Rule 2002 notice list in the Cases; (c) the use of

a consolidated case caption; and (d) that the Debtors be allowed to file Monthly Operating

Reports on a consolidated basis. I believe that joint administration will greatly benefit the

Debtors, the Bankruptcy Court, the Office of the Clerk, the U.S. Trustee and all other interested

parties in the Cases. Joint administration will simplify all aspects of the administration of the

Cases and result in substantial cost savings to the Debtors and other parties in interest.

d. Continuance of Gift Card Program

63. Prior to the Petition Date, the Debtors sold, in the ordinary course of business,

pre-paid gift cards (the “Gift Cards”) for use at any of the Restaurants. The Gift Cards are an

important tool used by the Debtors to generate revenue and build customer loyalty. When

customers purchased the Gift Cards, they had every expectation that the Gift Cards would be

redeemable. Customers typically redeem approximately $10,000 worth of Gift Cards each week.

To avoid alienating existing customers and irreparably damaging the Debtors’ reputation in the

competitive restaurant market, it is essential that the Debtors be authorized to continue to honor

Gift Cards, including those sold before the Petition Date, without interruption. Accordingly, the

Debtors have filed a motion seeking authority to continue their Gift Card program in the ordinary

course of business.

e. Wages and Benefits

64. In aggregate, the Debtors employed approximately 1,200 people as of the end of

their last payroll period on January 16, 2013 (the “Employees”), all of whom are non-union

employees. The Employees assist in critical aspects of running the business. At the Debtors’

restaurants, the Employees include chefs and other food preparers, servers, bartenders, hosts and

hostesses, dishwashers and store managers. The Employees also include area managers and

executives and staff located at the Debtors’ corporate headquarters in Chicago. The Employees’

CINCINNATI/97646.3 23

24. knowledge, expertise, and experience are essential to maintaining the Debtors’ businesses as a

going concern during these Cases.

65. Employees are the lifeblood of any restaurant business and the Debtors’

Employees in the field perform a variety of critical tasks, including preparing and serving food,

interacting with customers, ordering food and supplies, cleaning dishes and the restaurant

premises, supervising other employees and other tasks. In addition, the Debtors employ a

headquarters staff of approximately 14 persons who provide corporate functions such as

accounting and finance, marketing, human resources and other tasks. The Employees’ skills and

their knowledge and understanding of the Debtors’ operations are essential to the effective

operation and restructuring of the Debtors’ businesses. Without the continued services of the

Employees, an effective restructuring of the Debtors will not be possible.

66. The Debtors have filed a motion seeking authority, on an expedited basis, to pay

certain prepetition wages, benefits, reimbursement amounts, payroll taxes, and related costs and

to transfer certain amounts related to the same (the “Wage and Benefit Motion”). If prepetition

wage, compensation, benefit and reimbursement amounts are not received by the Employees in

the ordinary course, they will suffer extreme personal hardship and in many cases will be unable

to pay their basic living expenses. Such a result obviously would destroy Employee morale and

result in unmanageable Employee turnover, causing immediate and pervasive damage to the

Debtors’ ongoing business operations. Any significant deterioration in Employee morale at this

time will substantially and adversely affect the Debtors and their ability to reorganize, thereby

resulting in immediate and irreparable harm to the Debtors and their estates.

67. Accordingly, by the Wage and Benefit Motion, the Debtors are seeking an order

authorizing them, in their sole discretion, to pay (a) prepetition employee wages, salaries,

CINCINNATI/97646.3 24

25. overtime, vacation pay, incentive compensation, and related items (the “Prepetition Employee

Compensation”); (b) prepetition reimbursable business expenses incurred by employees;

(c) prepetition employee payroll deductions and withholdings; (d) prepetition payroll taxes;

(e) prepetition contributions to, and benefits under, employee benefit plans (the “Employee

Benefits”); (f) all costs and expenses incident to the foregoing; and (g) granting certain related

relief. This relief is essential to maintain employee morale and productivity, thereby preventing

unnecessary and harmful disruption in the operation of the Debtors’ business as they endeavor to

pursue successful reorganization in chapter 11.

68. With one exception, the Debtors do not believe that the amount of Prepetition

Employee Compensation plus Employee Benefits to be paid to or on account of any particular

Employee will exceed the sum of $11,725 allowable as a priority claim under sections 507(a)(4)

or 507(a)(5) of the Bankruptcy Code.12

69. Prior to the Petition Date, in the ordinary course of business, the Debtors’

reimbursed the Employees for certain expenses incurred within the scope of their employment

and on behalf of the Debtors, including auto mileage, travel, lodging, meals or other necessary

and appropriate expenses (the “Prepetition Reimbursable Expenses”). Most of the Prepetition

Reimbursable Expenses are incurred by employees on corporate credit cards issued by American

Express. While the Debtors normally pay any Prepetition Reimbursable Expenses incurred on

the corporate cards directly to American Express, unpaid balances will result in personal liability

for the individual Employees. Because the Debtors filed the Petitions in the middle of an

American Express billing cycle, certain of the Employees have not yet been reimbursed for

12

As discussed in greater detail in the Wage and Benefit Motion, the Debtors have identified one non-executive

management employee who is owed compensation plus benefits of approximately $20,800, which exceeds the

allowed priority claim amount of $11,725 imposed under section 507(a). In connection with the other relief sought

in the Wage and Benefit Motion, the Debtors are seeking authority to pay this employee the full prepetition amount

that he is owed.

CINCINNATI/97646.3 25

26. Prepetition Reimbursable Expenses previously advanced on behalf of the Debtors and no

American Express balances have been paid by the Debtors for the most recent monthly billing

cycle. These expenses were incurred by the Employees in the performance of their duties and

should be reimbursed to them. The Debtors pay, on average, approximately $80,000 in respect

of Prepetition Reimbursable Expenses per month.

70. The Debtors estimate that the amount of untransferred prepetition employee

obligations including Prepetition Employee Compensation (i.e., the gross payroll amount before

deducting withholdings) as of the Petition Date is approximately $425,000. The Debtors seek

authority to pay and transfer this full amount.

71. The Debtors also seek to pay in the ordinary course any outstanding prepetition

amounts that are owed to their payroll processor, Automatic Data Processing, Inc. (“ADP”) in

order to avoid any disruption to the critical payroll function. As of the Petition Date, ADP was

owed less than $3,000 on account of prepetition services.

72. I believe that if the Bankruptcy Court does not approve on an expedited basis any

of the relief sought by the Debtors in connection with the Wage and Benefit Motion, the

Debtors’ and their estates will suffer immediate and irreparable harm.

f. Cash Management System

73. The Debtors have established a series of bank accounts comprising an integrated

and centralized cash management system (the “Cash Management System”) through which the

Debtors’ funds are collected, managed, and disbursed in the ordinary course of business. I

believe that continuance of the Cash Management System without interruption is essential to the

Debtors’ efforts to reorganize in the Cases. Accordingly, the Debtors have filed a motion

seeking authority, on an expedited basis, to continue utilizing the Cash Management System in

the ordinary course of business and seeking related relief (the “Cash Management Motion”).

CINCINNATI/97646.3 26

27. 74. The Cash Management System utilizes fifteen bank accounts (the “Bank

Accounts”), twelve of which are with U.S. Bank, the Debtors’ former13 senior secured lender

(the “U.S. Bank Accounts”). Where U.S. Bank does not maintain branches in close proximity to

the Debtors’ restaurant locations, the Debtors established accounts at other banks. Two such

accounts were established with JPMorgan Chase and one with Bank of America.

75. The cornerstone of the Cash Management System is the Debtors’ concentration

account at U.S. Bank (the “Concentration Account”), through which all of the Debtors’

collective funds flow. Virtually all deposits that are made into the Cash Management System are

daily deposits of cash and credit card revenue generated from each of the Debtors’ various

restaurant locations. Most of a Restaurant’s cash deposits are held in the Restaurant’s safe until

picked up by armored car service, typically weekly. Cash is deposited into the Concentration

Account the day following armored car pick up. Other cash deposits are made into the

JPMorgan and BofA Accounts and then transferred (usually on a weekly basis) by ACH into the

Concentration Account.

76. The Debtors’ credit card revenue deposits are made separately from the cash

deposits into three separate deposit accounts at U.S. Bank. Each of these accounts is a zero

balance account which funds are swept daily into the Concentration Account.

77. Although the Debtors are separate legal entities, their businesses and affairs have

historically been operated and managed as a single business operation through FOC.14 Indeed,

while profit and loss statements are able to be generated for individual store locations, the

Debtors keep a single set of books and records for the business operation as a whole. As such,

13

As indicated above, prior to the Petition Date, U.S. Bank’s note pursuant to the Senior Prepetition Facility was

acquired by HillStreet on January 18, 2013.

14

The Debtors reserve all rights with respect to the potential substantive consolidation of the Debtors’ estates, and

nothing herein is intended to be an admission or waiver of any rights or arguments with respect to the same.

CINCINNATI/97646.3 27

28. the funds received from each restaurant location are deposited into the Concentration Account

without accounting for the particular Debtor entity that generated the funds and without

recording intercompany credits and balances. In the same vein, the Debtors do not record

intercompany loans or transfers.

78. Similarly, most disbursements and expense payments are made by FOC from the

Concentration Account without regard to the particular restaurant for which an expense was

incurred. Such disbursements include loan and lease payments, payroll wires to Automatic Data

Processing (“ADP”) (the Debtors’ third party payroll provider), and various ACH transfers

(including for 401(k) payments and various tax payments).

79. In the ordinary course of its business, the Debtors use certain checks and other

business forms. The alteration of the Debtors’ checks and business forms would be unnecessary

and unduly burdensome. To avoid disruption of the Cash Management System and unnecessary

expense, the Debtors also request that they not be required to include the legend “D.I.P.” and the

corresponding bankruptcy case number on any business forms or checks. Otherwise, the estates

will be required to bear an expense, which the Debtors respectfully submit is unwarranted.

80. I believe that, under the circumstances, the maintenance of the Cash Management

System in substantially the same form as it existed prior to the Petition Date is in the best

interests of the Debtors’ estates and their creditors.

g. Extension of Time to File Statements and Schedules

81. The Debtors were compelled to file these Cases under exigent circumstances and

while under significant liquidity constraints. Leading up to the commencement of the Cases, the

Debtors’ first priority was to ensure a smooth transition into chapter 11 with minimal disruption

to their business operations. To this end, the Debtors dedicated their limited staff and resources

to negotiating with lenders, evaluating restructuring alternatives, developing strategies to

CINCINNATI/97646.3 28

29. maximize value and successfully reorganize its business, and assisting with the preparation of

critical first day motions.

82. Additionally, the Debtors’ operations are complex, encompassing fifteen separate

legal entities. Completing the Schedules and Statements for each Debtor will require the

collection, review and assembly of information from books, records, and documents relating to

myriad claims, assets, and contracts. This information is voluminous and located in numerous

locations. Although the Debtors have sufficient staff on hand to maintain their ordinary business

operations under normal circumstances, they are understaffed for purposes of having their

officers and management divert their attention and efforts away from ordinary business

operations and transitioning into chapter 11 with minimal disruption to focus on compiling their

respective schedules of assets and liabilities and statements of financial affairs (the “Schedules

and Statements”).

83. The Debtors will endeavor to complete the Schedules and Statements as

expeditiously as possible under the circumstances. However, they anticipate that they will not be

able to do so within 14 days of the Petition Date, as required under the Bankruptcy Code.

Accordingly, the Debtors filed a motion asking that they be granted an additional 30 days to do

so (for a total of 44 days from the Petition Date), while reserving their rights to request further

extensions if necessary or appropriate under the circumstances. I believe that the size, scope and

complexity of the Cases and the volume of material that must be compiled and reviewed by the

Debtors’ limited staff to complete the Schedules and Statements for each of the Debtors during

the hectic early days of these Cases provide ample “cause” justifying the requested extension.

CINCINNATI/97646.3 29

30. Vendor Matters

h. PACA Claims

84. The Debtors use a significant amount of fresh produce in the operation of the

Restaurants. The Debtors have examined their vendor records and determined that a certain

portion of the goods the Debtors purchased before the Petition Date, but had not yet paid for may

qualify as “perishable agricultural commodity[ies]” under the Perishable Agricultural

Commodities Act of 1930 (“PACA”). PACA provides various protections to fresh fruit and

vegetable sellers, including establishing a statutory constructive trust consisting of a buyer’s

entire inventory of food or other derivatives of perishable agricultural commodities, the products

derived therefrom and the proceeds related to any sale of the commodities or products. It is my

understanding that any such funds related to a trust created pursuant to PACA are preserved as a

non-segregated floating trust (the “PACA Trust”) that may be commingled with non-trust assets

and that such funds are not property of the Debtors’ estates.

85. The Debtors have identified at least 20 potential parties (the “PACA Claimants”),

who have provided the Debtors with written notice of their intent to preserve the benefits of the

PACA Trust. These PACA Claimants were owed approximately $395,000 in pre-petition claims

potentially subject to PACA (the “PACA Claims”) on account of produce delivered to the

Debtors prior to the Petition Date. As a result, the Debtors believe that certain vendors are likely

to file notices under PACA based on the filing of these Cases.

86. Accordingly, the Debtors have filed a motion (the “PACA Motion”) seeking

authority to: (a) establish procedures for the reconciliation and disposition of PACA Claims and

(b) satisfy valid PACA claims, recognizing that, absent such relief, such claims would be

satisfied in any event through a more costly and contentious process. Because the funds held

pursuant to PACA are not property of the Debtors’ estate until suppliers of goods covered by

CINCINNATI/97646.3 30

31. PACA are paid, payments to the PACA Claimants in respect of the PACA Claims will not

reduce estate assets. I believe that the relief sought in the PACA Motion is necessary to the

Debtors’ efforts to operate their businesses in chapter 11, and that payments made on account of

valid PACA Claims will benefit the Debtors and all parties in interest in the Cases by

(i) allowing the Debtors to continue purchasing and receiving fresh produce and other products

for use in the Restaurants; and (ii) avoiding potential disruption to the Debtors’ business

operations.

i. Adequate Assurance of Utility Payments

87. In the normal course of their business, the Debtors use electricity, gas, water,

sewer, telephone and other utility services for which they pay directly and which is provided by

approximately 50 utility companies. Continued and uninterrupted utility service is essential to

the Debtors’ ability to sustain their food service operations during these Cases, and any

interruption of utility service would severely disrupt the Debtors’ business operations and their

restructuring efforts, and jeopardize the Debtors’ ability to preserve the value of the estates.

88. I believe that the Debtors’ ability to preserve the value of the estates will be

irreparably damaged if the utility companies currently providing services, or that will provide

services during the Cases (collectively, the “Utility Companies”) do not continue to provide

these services.

89. Historically the Debtors have made prompt and complete payments with respect

to the Utility Companies before the Petition Date. Several Utility Companies are holding pre-

petition security deposits.

90. Even though some outstanding arrearages may exist with respect to some of the

Utility Companies, I have been advised that any Utility Company seeking a security deposit (or

an additional security deposit) or seeking to terminate services would be doing so as an

CINCINNATI/97646.3 31

32. automatic reaction to a filing for relief under the Bankruptcy Code. The Debtors have and will

continue to have sufficient funds to make timely payments to the Utility Companies for all post-

petition utility service.

91. Additionally, in order to avoid the irreparable harm to the Debtors’ estates that

would result from Utility Companies discontinuing their services, the Debtors have filed a

motion (the “Utility Motion”) seeking immediate entry of an interim order: (a) prohibiting Utility

Companies from altering, refusing, or discontinuing services to the Debtors on account of the

filing of the Cases, any pre-petition amounts outstanding, or on account of any perceived

inadequacy of the Debtors’ proposed adequate assurance, pending entry of the final order (the

“Final Order”) granting the relief sought in the Utility Motion on a final basis; (b) determining

that the Utility Companies have received adequate assurance of payment for future utility

services on the terms provided in the Utility Motion, under which Utility Companies may request

additional or different adequate assurance; (c) establishing procedures for Utility Companies that

seek to opt out of the Debtors’ proposed adequate assurance procedures; (d) determining that the

Debtors are not required to provide any additional adequate assurance, beyond what is proposed

in the Utility Motion, pending entry of the Final Order; and (e) setting a final hearing regarding

the Utility Motion for the entry of the Final Order.

j. Trust Fund and Other Taxes

92. In the ordinary course of operating their businesses, the Debtors collect and/or

incur income taxes, sales taxes, use taxes, franchise taxes and fees, personal property taxes and

other taxes, assessments, fees and similar charges (collectively, the “Taxes and Fees”). The

Debtors remit the Taxes and Fees to various federal, state and local taxing, licensing and other

governmental authorities (collectively, the “Authorities”). The Debtors pay the Taxes and Fees

CINCINNATI/97646.3 32

33. weekly, monthly, quarterly, annually or biennially to the respective Authorities, in accordance

with any applicable laws and regulations.

93. The Debtors believe that many of the Taxes and Fees collected prepetition are not

property of the Debtors’ estates as they constitute “trust fund” taxes, and must for that reason be

turned over to the Authorities. The failure to pay the Taxes and Fees could also result in

Authorities bringing personal liability actions against directors, officers and other employees or

taking actions that might interfere with the Debtors’ successful reorganization. Any such actions

would certainly distract key personnel from the Debtors’ reorganization efforts at a critical time in

the process and negatively impact these Cases. In any event, even if certain Taxes and Fees are

not actually the property of the Authorities, they may give rise to priority claims.

94. Accordingly, the Debtors have filed a motion for entry of an order authorizing,

but not directing, them to pay certain Taxes and Fees to the Authorities, and authorizing, but not

directing, financial institutions to receive, process, honor, and pay all related checks and

electronic payment requests, to the extent the Debtors have sufficient funds with such financial

institutions.

k. Lease Rejection Motion

95. In an effort to improve profitability and maximize the value of their estates, the

Debtors have undertaken an extensive analysis of their businesses and closed a number of

Restaurants prior to the Petition Date. Accordingly, the Debtors have filed a motion (the “Lease

Rejection Motion”) seeking authority to reject certain of their unexpired real property leases,

effective as of the Petition Date.

96. Using their business judgment, and upon careful evaluation of all of their

Restaurants, the Debtors have determined that none of the leases identified in the Lease

Rejection Motion are necessary or valuable to the Debtors’ estates. I am advised that each of the

CINCINNATI/97646.3 33

34. leases identified in the Lease Rejection Motion is an “unexpired lease” within the meaning of

section 365 of the Bankruptcy Code, capable of being rejected by the Debtors. However, to the

extent that any of these leases already has expired or been terminated, it is included in the Lease

Rejection Motion out of an abundance of caution and the Debtors reserve all of their rights to

object to any rejection damage claims related to such lease on any grounds, including but not

limited to a party’s failure to mitigate damages.

Motions and Applications Relating to Professionals

l. Appointment of Kurtzman Carson Consultants, LLC as Claims, Noticing and

Administrative Agent

97. The Debtors recognize that the large number of creditors and other parties in

interest involved in their chapter 11 cases may impose heavy administrative and other burdens

upon the Court and the Clerk’s Office. To relieve the Court and the Clerk’s Office of these

burdens, and in accordance with the Local Bankruptcy Rules, the Debtors will seek the entry of

separate orders appointing KCC as (a) the Debtors’ claims and noticing agent in the Cases and

(b) the Debtors’ administrative agent in these Cases. KCC may, among other things: (a) prepare

and serve all notices required in the Cases, including notice of the commencement of the Cases

and the initial meeting of creditors under section 341 of the Bankruptcy Code; (b) receive all

claims and maintain the official claims register; (c) assist in preparing, filing, and maintaining

the Debtors’ official Schedules and Statements; (d) assist with the mailing and tabulation of

ballots in connection with any vote to accept or reject any plan or plans proposed in the Cases.

The Debtors obtained and reviewed engagement proposals from three court approved notice and

claims agents, and selected KCC based on their capability and experience and the cost of their

proposal, and have otherwise complied with the Bankruptcy Court’s Protocol for the

Employment of Claims and Noticing Agents under 28 U.S.C. § 156(c). I believe that the

CINCINNATI/97646.3 34

35. appointment of KCC to perform the functions above will facilitate the efficient administration of

the Case.

m. Other Professional Retention Applications

98. The retention of certain chapter 11 professionals is essential to the Debtors’

efforts in the Cases to preserve value for its estate. Accordingly, the Debtors have sought or will

seek to retain various professionals in the Cases. These professionals include: (a) Squire Sanders

(US) LLP (“Squire Sanders”), as their bankruptcy counsel; (b) Getzler Henrich as their financial

advisor and William H. Henrich and Mark Samson from Getzler Henrich as their Co-Chief

Restructuring Officers in the Cases; and (c) J.H. Chapman Group, L.L.C, as their investment

bankers. I believe that (i) the foregoing professionals are well qualified to provide the services

contemplated by their various retention applications, (ii) the services to be provided by the

foregoing professionals are necessary for the success of the Cases, and (iii) the foregoing

professionals will coordinate their services to avoid any duplication of effort. The Debtors may

find it necessary to seek to retain additional professionals as the Cases progress.

INFORMATION REQUIRED BY LOCAL BANKRUPTCY RULE 1007-2

99. I am informed that Local Bankruptcy Rule 1007-2 requires that certain

information about the Debtors be provided in this Affidavit. Various information satisfying this

rule, including Local Bankruptcy Rule-1007-2(a)(1), is set forth in the text above. The

remaining required information is provided in the attached schedules, as follows:

Schedule 1 The holders of the Debtors’ 30 largest unsecured claims, excluding

claims of insiders and information regarding such claims

Schedule 2 The holders of the Debtors’ three largest secured claims

and information regarding such claims

Schedule 3 A summary of the Debtors’ assets and liabilities, in unaudited

consolidated balance sheet format, as of November 28, 2012.

CINCINNATI/97646.3 35

36. Schedule 4 All of the Debtors’ property in the possession or custody of any

custodian, public officer, mortgagee, pledgee, assignee of rents

or secured creditor, or agent for any such entity.

Schedule 5 A list of the premises owned, leased or held under other

arrangement from which the Debtors operate their businesses.

Schedule 6 The location of the Debtors’ substantial assets; the location of their

books and records and the nature, location and value of any assets

held by the Debtors outside the territorial limits of the United States.

Schedule 7 A list of the actions or proceedings that are pending or threatened,

against the Debtors or their property where a judgment against the

Debtors or a seizure of their property is imminent.

Schedule 8 A list of the names of the individuals who comprise the Debtors’

existing senior management team, their tenure with the Debtors and

a brief summary of their relevant responsibilities and experience.

Schedule 9 Additional information required by Local Bankruptcy Rule 1007-

2(b).

CONCLUSION

100. I respectfully request that all of the relief requested in the First-Day Pleadings be

granted along with such other and further relief as is just.

CINCINNATI/97646.3 36

37.

38. Exhibit A

Organization Chart

Flat Out Crazy Restaurant Group

Ownership Structure

The Hillstreet Fund IV, L.P.

Happy Valley Corporation

Stir Crazy Partners, LLC & Series C Investors

Shareholders

5%

26.74%

53.37% 14.89%

Flat Out Crazy, LLC

SCR Operations, LLC

100%

100%

100%

SCR Hospitality, LLC

Stir Crazy Restaurants, LLC 100%

SCR Concessions, LLC

Stir Crazy Café Stir Crazy Café

Oakbrook, LLC 100% 100% Northbrook, LLC

Stir Crazy Café Stir Crazy Café

Woodfield, LLC 100% 100% Great Lakes, LLC

Stir Crazy Café Stir Crazy Café

Boca Raton, LLC 100% 100% West Nyack, LLC

Stir Crazy Café Stir Crazy Café

Creve Coeur, LLC 100% 100% Legacy Village, LLC

Stir Crazy Café

Cantera, LLC 100% 100% Stir Crazy Operations, LLC **

* Percentages vary based on preferences and distribution waterfall as detailed in the Operating Agreement.

** Current and new Stir Crazy stores since Walnut's acquisition of Stir Crazy Partners, LLC

CINCINNATI/97646.3

39. Schedule 1

30 Largest Unsecured Creditors

Pursuant to Local Bankruptcy Rule 1007-2(a)(4), the list below contains information with

respect to each of the holders of the Debtors’ 30 largest unsecured claims, excluding insiders, on

a consolidated basis.

(1) (2) (3) (4) (5)

Name of creditor and complete mailing Name, telephone number and complete Nature of claim (trade Indicate if claim is Amount of claim

address including zip code mailing address, including zip code, of debt, bank loan, contingent, [if secured, also